5 Stocks with Strong Upside Potential

$MSFT - Microsoft Corporation

Microsoft controls one of the most powerful ecosystems in enterprise technology, deeply embedded within global corporate workflows and IT infrastructure. This creates exceptionally high switching costs, strong customer lock-in, and one of the most durable competitive moats in the software industry.

Azure remains one of the global leaders in cloud computing and is rapidly evolving into a comprehensive AI infrastructure platform. By 2026, Azure is expected to account for more than 26% of Microsoft's total revenue.

Total cloud revenue reached approximately $54.5 billion (+29% YoY), while AI-related ARR climbed to approximately $37 billion (+123% YoY).

More than 300 customers are now on track to process over 1 trillion AI tokens annually, and over 10,000 customers are already using multiple AI models within Microsoft's ecosystem.

Microsoft has also become the first large-scale enterprise platform to deeply integrate AI copilots and autonomous agents across its productivity suite. The company now has more than 20 million paid Copilot seats, representing one of the fastest enterprise AI adoption curves in the industry, with seat growth accelerating approximately 250% YoY.

Enterprise adoption continues to strengthen. Accenture alone has surpassed 740,000 Copilot seats, while nearly 90% of Fortune 500 companies are already using Copilot Studio agents. This positions Microsoft at the forefront of the emerging agentic AI enterprise workflow market.

Its data and analytics ecosystem are also expanding rapidly, with Fabric customers reaching 35,000 (+60% YoY) and more than 15,000 customers using both Foundry and Fabric together.

This vertically integrated stack (spanning chips, infrastructure, cloud computing, AI models, data platforms, and enterprise applications), creates a competitive moat that very few companies globally can replicate.

Across Microsoft’s segments, Productivity & Business Processes grew +17%, Intelligent Cloud +30%, Azure +40%, and Dynamics 365 +22%. These businesses continue serving as the company's primary growth engines despite one of the largest investment cycles in Microsoft's history.

Microsoft remains one of the highest-quality compounders in the market, with a credible path toward becoming the operating system of the AI economy, where cloud, data, AI, and enterprise applications increasingly converge into a deeply integrated ecosystem.

Despite stock is down around 20% in the last 6 months, Microsoft remains one of the highest-quality compounders with a credible path toward becoming the operating system of the AI economy, where cloud, data, AI, and enterprise applications increasingly converge into a deeply integrated ecosystem.

If execution remains strong and AI monetization continues accelerating, Microsoft appears exceptionally well positioned to deliver sustained compounding growth over the next decade.

Bill Ackman started his Microsoft position around 21x forward earnings.

Today, the stock trades at 21.4x yet again.

Microsoft is in Ackman's buying zone.

$MSFT

#Risiko: si riscrive la mappa del potere bancario italiano. E la partita è appena cominciata.

Al centro di tutto c'è #Mps, il re, conteso tra Banco BPM e Intesa Sanpaolo. Ma la vera partita, quella più profonda, si gioca sulla regina: #Generali.

Cinque città da tenere d'occhio: Milano, Bologna, Siena, Trieste e Roma. Ognuna con i suoi giocatori, i suoi interessi, le sue mosse ancora da scoprire.

Unicredit è silenziosa, per ora. Il governo non sarà indifferente. E Caltagirone ha già detto no a BPM.

Una giornata da seguire minuto per minuto.

L'editoriale del Direttore Andrea Cabrini

Bill Ackman bought a third of a $20 billion company after it crashed to $100 million

Stock went from 34 cents to $34

"I called the CEO. He didn't return my call. I called again. Six weeks later they spun off the company, the CEO got fired, then he called to thank me for his exit package."

29 minutes

The most contrarian bet in modern Wall Street history explained by the man who made it

Watch the video then read the article

Bill Ackman on markets, the new thing, and high-quality being left behind:

“What’s interesting about markets is people always bring their eye to the new thing… what tends to happen is really high quality things get left behind…”

___

🎙️ All-In Pod | Bill Ackman (06/03/26)

Wall Street keeps saying Big Tech is “too expensive.”

Meanwhile, super investors are buying:

$MSFT 18 buys

$AMZN 15 buys

$META 15 buys

$V 12 buys

$DIS 11 buys

$UBER 8 buys

$BRK.B 8 buys

$ADBE 8 buys

Maybe the best companies rarely look cheap.

Which one are you backing?

🚨 $META cotiza a 18x beneficios futuros. La Big Tech más barata del planeta.

🟢 $AAPL: 32x

🟢 $AMZN: 32x

🟢 $GOOGL: 31x

🟢 $NVDA: 26x

🟢 $MSFT: 22x

🔴 $META: 18x

Una empresa con 3.000 millones de usuarios activos. Margen operativo superior al 40%.

Bitcoin is better money than gold. It has superior monetary properties.

In fact, Bitcoin beats gold on 25 different dimensions.

1. Portability: Move billions across borders with 12 or 24 words. Gold needs guards, vaults, trucks, customs, and prayers.

2. Divisibility: Bitcoin divides into 100 million sats per BTC. Gold is awkward to divide, verify, and spend in small amounts.

3. Verifiability: Anyone can verify Bitcoin supply and ownership with a node. Gold requires assays, trust, and specialists.

4. Scarcity certainty: Bitcoin has a hard cap of 21 million. Gold supply expands with mining, new discoveries, and potentially asteroid mining.

5. Supply auditability: Bitcoin’s total supply is publicly auditable in real time. Nobody knows the exact amount of above-ground gold.

6. Settlement speed: Bitcoin can settle globally in minutes. Gold settlement is slow, expensive, and institution-heavy.

7. Custody sovereignty: Bitcoin can be self-custodied without a vault. Gold self-custody is physically dangerous and logistically annoying.

8. Confiscation resistance: Properly secured Bitcoin can cross borders invisibly. Gold is obvious, heavy, and historically confiscatable.

9. Storage cost: Bitcoin can be stored for near-zero physical cost. Gold requires vaulting, insurance, security, and transportation.

10. Transport cost: Bitcoin travels at the speed of information. Gold travels at the speed of armored logistics.

11. Programmability: Bitcoin can integrate with multisig, time locks, Lightning, smart custody setups, and financial infrastructure. Gold is inert metal.

12. Global liquidity: Bitcoin trades 24/7 globally. Gold markets still rely heavily on traditional financial rails and business-hour settlement layers.

13. Settlement finality: Bitcoin can provide direct bearer settlement without trusted intermediaries. Gold often settles through paper claims.

14. Resistance to counterfeit: Bitcoin units are mathematically validated. Gold can be plated, diluted, faked, or rehypothecated.

15. No trusted issuer: Bitcoin has no central issuer, board, treasury, or refinery bottleneck. Gold custody often depends on institutions.

16. Easier inheritance: Bitcoin can be structured with multisig and recovery planning. Gold inheritance is physical, messy, and theft-prone.

17. Collateral efficiency: Bitcoin is easier to pledge, move, audit, and financialize digitally. Gold collateral is slower and more custodial.

18. Transparency: Bitcoin’s monetary policy and ledger are open. Gold’s market is opaque, with hidden reserves, paper claims, and unclear leverage.

19. Censorship resistance: Bitcoin can be sent peer-to-peer globally. Gold needs physical handoff or trusted transport.

20. Energy-to-scarcity conversion: Bitcoin turns energy into digitally verifiable scarcity. Gold turns energy into heavy rocks guarded by men with sunglasses.

21. Monetary upgradeability: Bitcoin can absorb software improvements at the network edges. Gold cannot become more useful without wrapping it in trust-based systems.

22. Unit consistency: Every bitcoin is perfectly fungible at the protocol level. Gold varies by purity, form, assay, and bar history.

23. Lower friction: Bitcoin is easier to buy, sell, send, receive, verify, split, secure, and integrate into modern finance.

24. Digital-native compatibility: Bitcoin fits an internet economy. Gold belongs to a world of vault receipts, musty central bankers, and men named Klaus guarding basements.

25. Personal sovereignty: Bitcoin lets one person hold immense wealth directly. Gold makes you become your own medieval castle.

All investors should study Fair Isaac FICO $FICO

Yes, long-term debt is a high percentage of total assets, but their interest expense is a low percentage of operating profit (meaning debt is affordable).

And yes, stock-based compensation is a high percentage of operating cash flow, but their FCF per share CAGR is high and their shares outstanding are dropping quickly (meaning there's still great capital allocation).

Peter Lynch said: "There is 100% correlation between a company's earnings and what happens to the stock.”

If stock price follows EPS, here are 6 stocks that look like opportunity.

1. $MSFT - Microsoft

🚨 Bill Ackman concentra el 82% de su cartera en solo 7 acciones.

🟢 Brookfield ($BN): 18,15% (subió posición un +49,69%)

🟢 Uber ($UBER): 15,90%

🟢 Amazon ($AMZN): 14,28% (subió posición un +64,99%)

🟢 Google ($GOOG): 12,46%

🟢 Meta ($META): 11,37% (nueva posición)

“Price is what you pay, value is what you get.”

– Warren Buffett

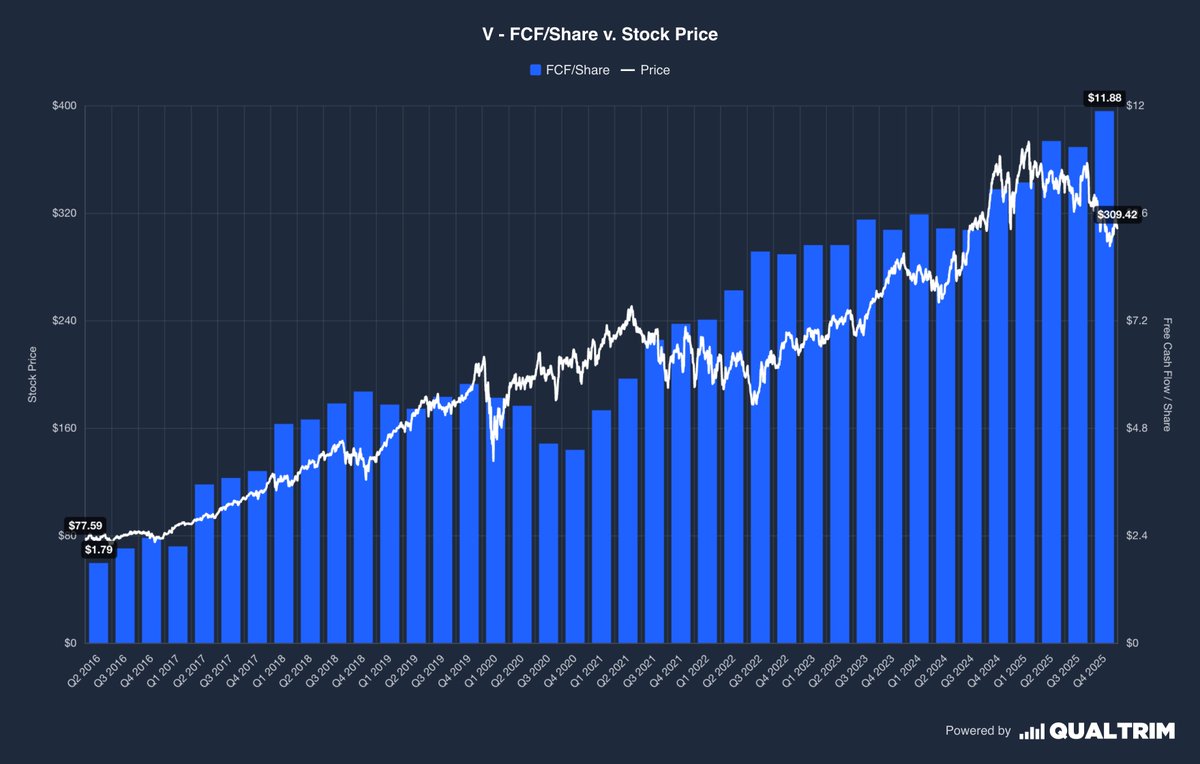

Visa and Mastercard are quietly compounding FCF/share. Yet, price hasn’t caught up.

It usually does.

$V $MA

Everyone uses "moat" and "competitive advantage" interchangeably. They're not the same thing.

One lasts 5 years. The other lasts 20. That difference explains this entire tier list.

$DUOL doesn't have a moat. And you can prove it in one sentence.

When they stopped posting unhinged memes on TikTok, downloads dropped immediately.

If your users leave because you stopped posting on social media, you don't have a moat. 91% of active users don't pay. I like the founder a lot. But the business? No.

$CPRT owns every junkyard in America. Still B-tier.

Daniel's framework here changed how I think about this. Competitive advantages last 5-6 years. A moat lasts 20+. Even if AVs are 20 years away, the market starts discounting that now. Zero debt. Land on the books at prices from the '90s. Still not enough if the business has an expiration date.

$BRK.B is A-tier, not S. And it's not because Buffett left.

The moat is untouchable. Insurance float, BNSF, energy. Nobody's replicating that. The problem? $300B in cash Abel can't deploy and 40% of the equity book sitting in $AAPL. Buffett himself said he was looking for opportunities and couldn't find them.

$CSU belongs above $BRK.B right now.

AI is compressing public software multiples faster than private ones.

So for the first time, buying listed VMS is actually cheaper than private acquisitions. That's why CSU's move into public markets works.

Leonard built the decentralization playbook from day one. Less key man risk. More runway. Berkshire was always one guy making the calls. CSU was designed to not need that.

$MELI would be S-tier if it were American.

Venezuela used to be one of their biggest markets. Then it was gone overnight.

That's the risk with the best flywheel in South America.

E-commerce, fintech, logistics. Each one feeds the others. They lend to merchants and just take repayment out of their sales. But the currency risk is real and they haven't been through a real recession yet. That keeps it at A.

$RMS is S-tier for a reason nobody talks about.

Executives must spend a decade in actual production. Making the bags. Before they can enter leadership. Six generations of leadership transitions.

$LVMH?

Arnault has 4-5 heirs and no clear successor. The ultra wealthy are spending more every year. The people buying luxury to look rich? Barely growing.

$UBER's strongest bull case is a parking problem.

When an NFL game ends, you need 20,000 cars. Uber doesn't care. Drivers go home. If Waymo owns the fleet, where do 20,000 cars sit at 2am on a Tuesday?

Where did we get it wrong?