Market somehow just realized that even if King 👑 Jetsen invests $2 B in the $IREN it still can’t make them profitable any time soon or ever so suddenly thunderous decline in AH 🤷🏻♂️

$IREN below daily highs after going up 25% in AH

$IREN Revenue Q3 FY26: $144.8 M

Bitcoin Mining Revenue declined by -33% from $167.4 to $111.2 M

While AI cloud services revenue increased by 94% from $17.3 to $33.6 M but its just 23% of the their total revenues 🤷🏻♂️

Depreciation and amortization: -$121.2 M (83.7% of the revenue…lol 🤣)

Net Income: -$247.8 M - this is nothing but the big sad joke 😂

I still am bearish on $IREN.

Algorithms/retail probably read $NVDA + $IREN partnership and bought it up.

However, if you look at the realtity, it's just looks like brand agreement giving $NVDA risk-free convertible notes.

So $IREN can continue selling their $6,000,000,000 ATM into retail investors.

It's the equivalent of a startup using AWS and saying they have an Amazon partnership so give them $6B.

This wasn't Nvidia directly funding $IREN yet, just a risk free option to.

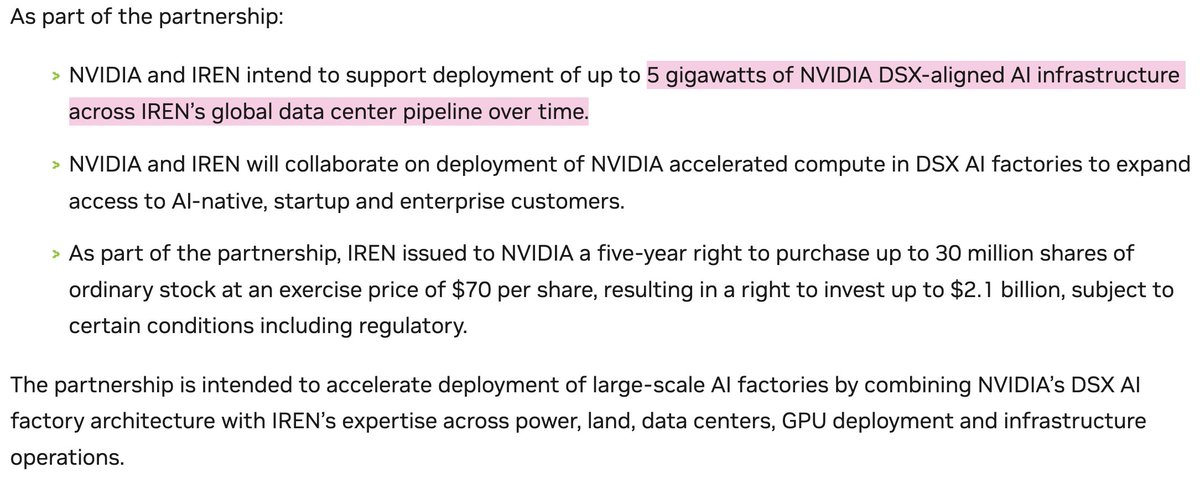

There's a "5 GW deployment" but I'd rather not be the one buying into the dilution to fund it.

PayPal $PYPL : The Market Is Missing The Setup

PayPal Holdings, Inc $PYPL . has quietly turned into one of those stocks the market no longer wants to think about. And in my experience, that’s usually where things start to get interesting.

This is still a company operating across 200+ markets, with roughly 450 million active accounts and nearly $2 trillion in annual payment volume. Those are not the metrics of a broken business. Yet the stock trades like one.

So the real question isn’t what PayPal is, but why the market has decided it no longer matters.

I think that’s where the opportunity lies.

A Business The Market Has Already Written Off

Let’s call it what it is: sentiment around PayPal has collapsed.

Since its separation from eBay, the company went from being a high-multiple fintech compounder to what the market now treats as a low-growth, commoditized payments platform. Competition intensified, growth slowed, and the narrative shifted from “category leader” to “just another wallet.”

But here’s what doesn’t add up to me.

Despite all the negativity, PayPal is still growing. Not hyper-growth, but stable, mid-single to low-double-digit growth across key metrics. And more importantly, it’s still generating significant cash flow with a massive installed user base.

Markets don’t usually price businesses like this at under 9x forward earnings unless they believe something structurally broken is happening.

I don’t see that here.

The Quarter Everyone Is Complaining About… Was Actually Solid

Let’s go straight to the numbers, because that’s where the disconnect becomes obvious.

PayPal reported Q1 2026 results that beat expectations on both the top and bottom line:

🔹Revenue came in at $8.4 billion, up 7% YoY

🔹Adjusted EPS was $1.34, ahead of the $1.27 consensus

🔹Total Payment Volume (TPV) grew 11% YoY to $460+ billion

Now step back for a second.

This is a company the market is treating like it’s stagnating, yet it’s still growing double digits on volume and mid-single digits on revenue at massive scale.

That’s not a decline story. That’s a mature platform with operating leverage.

And yet, the stock sold off.

Why?

Guidance, Not Fundamentals, Is Driving The Reaction

The real issue wasn’t the quarter. It was the forward outlook.

Management guided for a mid-single-digit EPS decline in Q2 and, more importantly, did not raise full-year guidance despite the Q1 beat.

That’s what the Street didn’t like.

But here’s how I interpret it: this looks more like conservative positioning than fundamental deterioration.

Companies that are undergoing internal restructuring and cost realignment tend to guide cautiously. PayPal is doing both right now.

So instead of asking, “Why didn’t they raise guidance?”, I think the better question is:

What happens if they eventually do?

The Quiet Transformation Underway

One of the more underappreciated developments here is the internal restructuring.

PayPal is reorganizing into three core segments:

🔹Checkout Solutions & Core PayPal

🔹Consumer Financial Services & Venmo

🔹Payment Services & Crypto

At first glance, this looks like corporate reshuffling. But structurally, it matters.

This kind of segmentation typically does two things:

🔹Improves accountability and capital allocation

🔹Makes individual business units easier to evaluate (and potentially monetize)

And yes, that includes the possibility of spinning off or selling assets like Venmo.

The market isn’t pricing in any of that optionality right now.

Cost Discipline + AI = Margin Expansion Story

Another piece that’s getting overlooked is the cost side.

Management is targeting ~$1.5 billion in run-rate savings over the next 2–3 years, driven by operational efficiencies and AI integration.

That’s not trivial.

For a company already generating billions in operating income, even modest margin expansion can materially impact earnings.

This is how mature platforms re-accelerate EPS growth without needing explosive revenue growth.

It’s not flashy but it works.

The Growth Drivers Are Still There (Just Not Hyped)

If you strip away the noise, some key growth engines are still performing:

🔹Branded checkout remains resilient

🔹Venmo monetization is improving

🔹Buy Now, Pay Later (BNPL) volume surged ~20%

These are not legacy segments in decline. These are still scaling businesses.

The issue is that none of them individually feel like a “breakout narrative” right now.

And markets tend to ignore companies that don’t have a clean, compelling story.

$PYPL good chance they end up spinning off Venmo to shareholders in a tax-free distribution. Buyers may be circling, but best bet for shareholders is the opportunity to hold onto $VNMO shares! This likelihood will continue to get priced in as we get more segment information. Same for Braintree. $PYPL Narrative has totally shifted, which is a good thing.

https://t.co/vzRStMMHq1

1850s

- no phone to call your parents (1876)

- life expectancy ~40 at birth

- kids pulling 11–12 hour shifts

2026

- you’re stressed because the app sent a notification

we are blessed and cursed