My friend makes $1.2 million a year as an Anthropic engineer.

I asked him how he learned prompting so well.

He sent me a video that was never supposed to get out. Their core team's prompting playbook.

You won’t find anything better about prompting than this video.

I watched it last night.

Halfway through, I realized I've been using Claude completely wrong for two years.

Watch it, then read the article below.

I'm a cardiologist. If I could only recommend two supplements for the rest of my career, it would be these:

Magnesium glycinate.

Vitamin D3 with K2.

I take both every day. I prescribe both constantly. And the number of patients whose lives visibly change within weeks of starting them still surprises me after twenty years.

Up to 75% of Americans are low in magnesium. Most have no idea. If you're stressed, sleeping poorly, cramping at night, your blood pressure runs high, or you feel wired but exhausted — this is probably why.

Magnesium calms the nervous system, relaxes blood vessels, supports healthy heart rhythms, and improves sleep quality. The glycinate form is highly absorbable and gentle on the stomach. 300-400mg before bed. It's the supplement patients thank me for most — because they finally wake up feeling calm instead of wrecked.

Most Americans are also deficient in vitamin D. Low D3 quietly ruins your mood, weakens your immunity, increases inflammation, and raises cardiovascular risk. I see suboptimal levels constantly in my heart patients. Target blood levels of 50-80 ng/mL — not the bare minimum of 30 most doctors accept.

Here's what almost nobody knows: low D3 actively depletes magnesium. Your body uses magnesium to convert D3 into its active form. If you supplement D3 without magnesium, you can actually worsen a magnesium deficiency — and wonder why you still feel terrible.

You need both. They work as a system.

And always take D3 with K2. Without K2, calcium from D3 can deposit in your arteries instead of your bones. Together, they keep bones dense and arteries clean.

D3 with K2 in the morning with a meal containing fat — they're fat-soluble.

Magnesium glycinate at night before bed.

Cheap. Available everywhere. Backed by extensive evidence. And the combination addresses two of the most common deficiencies driving the fatigue, poor sleep, anxiety, muscle cramps, and low mood that millions of people are medicating with far more expensive and dangerous interventions.

Your future self will thank you. Probably within two weeks.

Back of the envelope $SPGI

$SPGI trades for $120.82B market cap.

Apply $MCO current 26.31x NTM multiple to $SPGI 𝐑𝐚𝐭𝐢𝐧𝐠𝐬 business ($3.14B LTM operating profit) → $82.61B

Apply $MSCI 27.20x NTM multiple to $SPGI 𝐈𝐧𝐝𝐢𝐜𝐞𝐬 business ($1.33B LTM operating profit) → $36.17B

𝐑𝐚𝐭𝐢𝐧𝐠𝐬 + 𝐈𝐧𝐝𝐢𝐜𝐞𝐬 = $118.78B

$SPGI entire market cap is $120.82B

___

You’re basically getting Energy (Platts), Market Intelligence, and the Mobility spin-off for free

And here’s the value to those:

𝐄𝐧𝐞𝐫𝐠𝐲 (Platts): $975M LTM operating income (14.72% CAGR from 2021–LTM) — Conservative 15x multiple → $14.63B

𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐭𝐞𝐥𝐥𝐢𝐠𝐞𝐧𝐜𝐞: $1.21B LTM operating income assuming 8.5x multiple (IYKYK) since according to Mr Market it’s never going to grow → $9.68B

𝐌𝐨𝐛𝐢𝐥𝐢𝐭𝐲 (spin-off): low-end $7B

All together = $31.31B

___

𝐈𝐦𝐩𝐥𝐢𝐞𝐝 𝐭𝐨𝐭𝐚𝐥 𝐯𝐚𝐥𝐮𝐞: ~$150B, or ~25% higher than today’s market cap (~$510 share price) — $118.78B + $31.31B = $150B

All while margins keep expanding and >80% of FCF is returned to shareholders

At some point, Mr Market will take notice

For now, let the accretive buybacks continue

___

Post inspired by @moats_multiples who shared an excellent piece titled “Inside TCI’s Conference: The Anti-AI portfolio” — link below 👇🏽

https://t.co/9oBU83y6sU

🚨 SHOCKING: Claude can now analyze entire books like a $300/hour research consultant.

Most people read books and forget 90% within a month.

Here are 6 insane Claude prompts that extract every insight from any book, PDF, document in minutes.

(Save before you read another book)

“Mozart was the greatest musical talent maybe that ever lived... so what was his life like?

Well, he was bitterly unhappy and he died young... What the hell did Mozart do to screw it up?"

— Charlie Munger

John D. Rickefeller was the world's first billionaire.

Here are the 38 letters he wrote to his son in 15 sentences:

- Share this with someone who needs it.

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

I am getting a lot of messages from folks that are confused about $MELI's strategy still so I will try to explain further why the bad debt that is dragging their earnings is not as scary as what meets the eye.

Let me make it crystal clear if you aren't familiar with the mechanics here. That 3.9 ppts margin drop “bad debt” is the cost of upfront accounting. Under IFRS 9 standards, they are required to provision for expected bad debt the exact moment new loans are originated. No actual cash has been lost at that point in time. It is strictly a non-cash estimate of future risk. To be clear this is something to keep in mind. It should be somewhat representative of what is to come but they are also showcasing with their NIMAL it has been very effective so far.

The reason the hit looks so massive comes down to a couple of factors. First, the credit portfolio is growing at a rapid clip, which automatically triggers higher day 1 provision expenses. Second, they extended the duration of the loans. Longer terms carry a higher lifetime probability of default, meaning accounting rules force them to provision even more upfront compared to their shorter-term loans.

But this isn't a red flag. This is a deliberate strategy. Yes, there is inherent credit risk involved, but MELI is aggressively expanding their credit book downmarket. They are directly targeting the exact consumer demographic that shops on Shopee and other low-end consumers. MELI is playing the disruptor here. They are executing a strategic land grab against their downmarket competition, and it's kind of brilliant. Obviously, these cohorts are riskier with higher historical default probabilities, but the long-term payoff is massive. They are effectively neutralizing any upmarket move from Shopee by capturing and controlling those customers' purchasing power through Pago.

Then there is the bottom-line reality that gets ignored. Despite this aggressive expansion, their NIMAL (this stands for Net Interest Margin After Losses) remains extremely robust, tracking above 17%. Even after absorbing these massive, upfront non-cash provisioning hits, the credit business is still highly profitable. They aren't losing money at all. They are making the conscious choice to reinvest that credit profit directly back into the business to acquire market share. It’s exactly that. Reinvesting internally to own the market.

One other crucial aspect to understand: the margin drag from these longer-duration loans is largely an accounting hit. Because of IFRS rules, they have to book massive provisions upfront based on conservative lifetime risk models. But the reality? The actual repayment data shows these cohorts are outperforming those models. So, while they take a short-term margin hit on paper to fund these provisions, they are successfully capturing a customer base that is fundamentally less risky than the upfront accounting suggests. You heard that right, part or the drag is that they provisioned are larger amount and some folks paid off their loan faster. So they earner less interest on the loan. They are taking a paper penalty today to lock in high-quality, sticky users for tomorrow. 🍻

El cortisol no es solo la hormona del estrés.

Alimenta la grasa abdominal persistente, reduce la testosterona y altera el sueño.

Aquí tienes 8 maneras naturales de reducir el cortisol a partir de hoy

1. Exposición al frío.

Lisa Su, CEO of AMD said something that every investor needs to hear.

"We're probably on a massive 10-year cycle in terms of AI technology and AI buildout. And we're probably two years into it."

Most people look at AMD's all-time high stock price and think the trade is over.

They have it completely backwards.

AMD's server CPU market share has gone from 20% in 2022 to nearly 37% today and it's still accelerating.

Data center GPU revenue is projected to hit $15 billion in 2026, up 114% year-over-year.

The stock isn't expensive because the run is over but rather expensive because the market is finally believing the numbers.

Here's the part most people don't understand.

Nvidia controls roughly 80% of the AI accelerator market but inference serving AI responses to real users in real time, is increasingly price-sensitive, memory-intensive, and less dependent on CUDA.

AMD's MI series holds a decisive advantage in memory capacity, and Lisa Su just locked in a 6-gigawatt GPU commitment from OpenAI and multi-year deals with Meta and Oracle.

AMD is winning the customers who care about cost-per-token, not just raw training throughput.

And the MI400 hasn't even shipped yet and it's built on TSMC's 2nm process with HBM4 memory, it launches in the second half of 2026, directly targeting Nvidia's next-generation Rubin platform.

AMD projects data center operating income alone will reach $9.4 billion this year, up from $3.6 billion last year.

The biggest orders and the biggest returns are still ahead.

Milk Road is extremely bullish on AMD.

19. Avoid high quantities of raw vegetables

20. Consume butyrate-producing foods like ghee, butter, and cheese

21. Limit heavy metal intake from crappy cookware, tap water, and poor-quality fish

22. Eat polyphenol-rich food like berries, organic coffee, and dark chocolate.

Each of these prompts replaces work that costs:

- Junior Analyst: $100K/year

- Associate: $150K/year

- VP: $250K/year

Wall Street models in 10 minutes instead of 10 hours.

Copy any prompt. Replace the brackets. Get Goldman-quality financial analysis.

No finance degree needed

🚨 Anthropic's own team just showed how to actually prompt Claude.

24 minutes. free. from the people who built it.

watch the workshop. bookmark it.

worth more than every $300 course you almost bought.

you've been using Claude without knowing 40 of its prompts.

Then read the guide below.

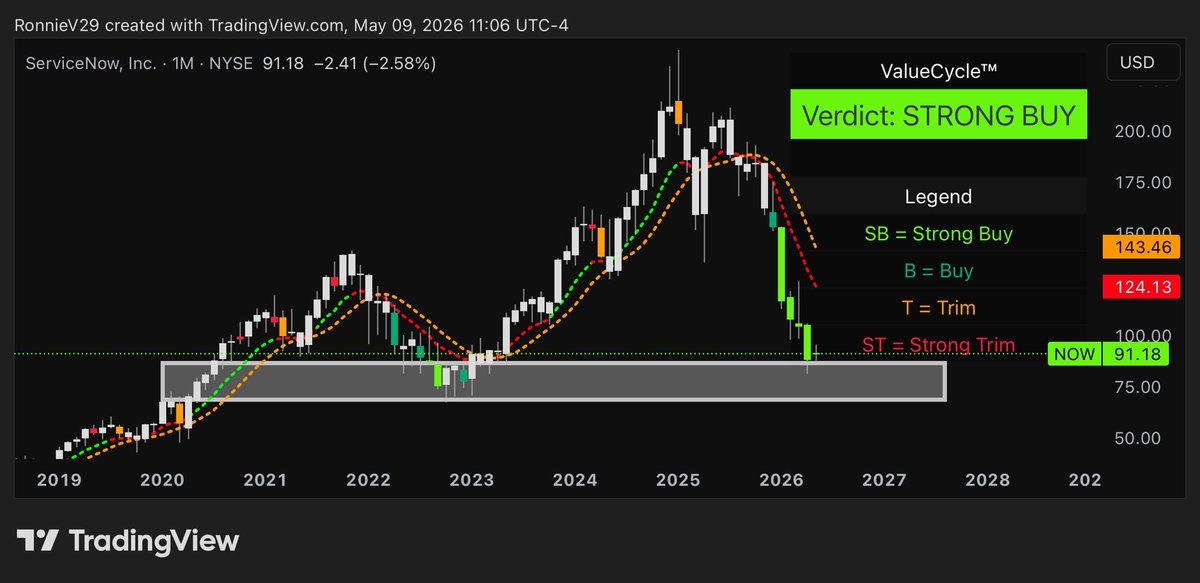

$NOW ULTRA DEEP DIVE:

AI is not replacing $NOW.

It may actually make ServiceNow even harder to leave.

That is the part I think most investors are missing.

Everyone keeps asking:

“Will AI replace SaaS?”

But with ServiceNow, I think the better question is:

“What happens when AI needs workflows to actually get work done?”

$NOW is not just another software company.

It is deeply embedded inside enterprise operations:

IT workflows

HR workflows

Customer service workflows

Security workflows

Finance workflows

Procurement workflows

Developer workflows

AI can answer questions.

But ServiceNow helps route, automate, approve, escalate, resolve, and connect work across the enterprise.

That is a much deeper moat than just “software.”

In Q1 2026, ServiceNow reported a 97% renewal rate, including Moveworks.

That tells me customers are not exactly rushing to leave the platform because of AI.

If AI was already hurting ServiceNow’s value, I would expect retention to weaken.

So far, that is not showing up.

The backlog is still strong too.

ServiceNow ended Q1 with $12.64B in cRPO, up 21% YoY in constant currency.

Total RPO reached roughly $27.7B, up 23.5% YoY in constant currency.

That matters because RPO is basically future contracted revenue.

If customers were pulling back because AI was replacing the need for ServiceNow, I would not expect to see that kind of growth in future commitments.

Large customers are also spending more.

ServiceNow now has 630 customers doing over $5M in ACV.

The company also had 16 deals over $5M in net new ACV, including 5 deals over $10M.

That is one of the most important pieces of the thesis.

The biggest enterprises are not just using ServiceNow.

They are expanding with it.

And once a company has ServiceNow embedded across multiple workflows, ripping it out becomes extremely difficult.

This is where the AI argument gets interesting.

AI may actually increase the need for ServiceNow.

Why?

Because enterprises do not just need AI answers.

They need AI to take action inside real business processes.

Create a ticket.

Route an approval.

Escalate an issue.

Trigger a workflow.

Resolve an IT request.

Connect data across departments.

Follow compliance rules.

That is where ServiceNow becomes valuable.

It is not just the AI layer.

It is the system that connects AI to actual enterprise work.

Now Assist is already showing traction too.

Customers spending over $1M in ACV on Now Assist grew over 130% YoY in Q1.

That is the opposite of the “AI is killing ServiceNow” argument.

At least right now, AI is becoming an upsell opportunity.

Not a replacement.

Multi-product adoption is another piece most people miss.

In Q1, 17 of ServiceNow’s top 20 deals included 7 or more products.

That tells me customers are not buying one small tool and calling it a day.

They are going deeper into the platform.

And the deeper they go, the more valuable ServiceNow becomes.

This is the key point:

The more workflows ServiceNow owns, the more valuable its AI becomes.

And the more AI gets embedded into those workflows, the harder the platform becomes to replace.

That is why I think the “AI will replace SaaS” argument is too simplistic.

AI might replace some basic software tools.

But platforms sitting at the center of enterprise operations could become even more important.

That is why I’m bullish on $NOW long term.

The moat is not just software.

The moat is workflow depth.

The moat is enterprise adoption.

The moat is switching costs.

The moat is being embedded inside the daily operations of massive companies.

AI is not replacing that overnight.

In my opinion, AI may actually make $NOW more important over time.