@UpslopeCapital This recent change feels like a hail mary attempt. I think he was faced with two choices:

1) Wind down the fund today and return capital back to LPs or,

2) Give it a last ditch effort to make a drastic change and hope it sticks.

After years of "buy good businesses, don't overpay, do nothing," Terry Smith just did… a lot. 12 buys, 13 sells, and a new appetite for activity.

Has one of quality investing's greats lost his nerve? My take on it below:

https://t.co/OABXWkd9yE

750m+ users. Two decades of listening data. 33% of global streaming and climbing. The moat some people call narrow keeps getting wider.

My Spotify thesis below:

https://t.co/hXNe11zC7D

SHOCKING: Many neocloud executives we spoke with feel that if they have non-NVIDIA networking gear on their cluster, or if their cloud has an AMD GPU or TPU offering, NVIDIA will retaliate. They feel that retaliation includes not giving early allocation or no longer supporting a potential IPO/VC raise.(1/3)🧵

Back of the envelope $SPGI

$SPGI trades for $120.82B market cap.

Apply $MCO current 26.31x NTM multiple to $SPGI 𝐑𝐚𝐭𝐢𝐧𝐠𝐬 business ($3.14B LTM operating profit) → $82.61B

Apply $MSCI 27.20x NTM multiple to $SPGI 𝐈𝐧𝐝𝐢𝐜𝐞𝐬 business ($1.33B LTM operating profit) → $36.17B

𝐑𝐚𝐭𝐢𝐧𝐠𝐬 + 𝐈𝐧𝐝𝐢𝐜𝐞𝐬 = $118.78B

$SPGI entire market cap is $120.82B

___

You’re basically getting Energy (Platts), Market Intelligence, and the Mobility spin-off for free

And here’s the value to those:

𝐄𝐧𝐞𝐫𝐠𝐲 (Platts): $975M LTM operating income (14.72% CAGR from 2021–LTM) — Conservative 15x multiple → $14.63B

𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐭𝐞𝐥𝐥𝐢𝐠𝐞𝐧𝐜𝐞: $1.21B LTM operating income assuming 8.5x multiple (IYKYK) since according to Mr Market it’s never going to grow → $9.68B

𝐌𝐨𝐛𝐢𝐥𝐢𝐭𝐲 (spin-off): low-end $7B

All together = $31.31B

___

𝐈𝐦𝐩𝐥𝐢𝐞𝐝 𝐭𝐨𝐭𝐚𝐥 𝐯𝐚𝐥𝐮𝐞: ~$150B, or ~25% higher than today’s market cap (~$510 share price) — $118.78B + $31.31B = $150B

All while margins keep expanding and >80% of FCF is returned to shareholders

At some point, Mr Market will take notice

For now, let the accretive buybacks continue

___

Post inspired by @moats_multiples who shared an excellent piece titled “Inside TCI’s Conference: The Anti-AI portfolio” — link below 👇🏽

https://t.co/9oBU83y6sU

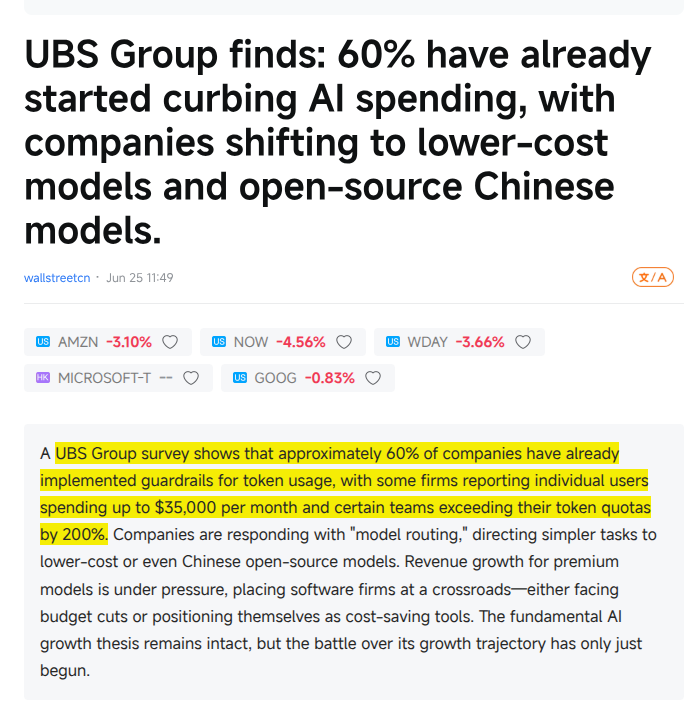

Don't find this surprising at all. Spoke to two friends recently who echoed this sentiment. One is an engineer at CVC and another at Adyen. Unless cost per token drops dramatically or ROI on token spend increases, I see this as bad news for the LLM companies.

UBS says 60% of companies now watching AI budgets are moving to cheaper models and open-source Chinese models

The pressure is coming from extreme bills, including users spending up to $35K/month, teams exceeding quotas by 200%, and companies cutting internal AI tools from 5 to 2.

Companies are not abandoning AI, they are using model routing, which sends easy tasks to cheaper models and saves premium models for hard reasoning, code, and long-context work.

Chinese open-source models such as Qwen, DeepSeek, MiniMax, GLM, and Kimi now fit the enterprise cost curve because they can be run locally or used through cloud catalogs.

---

news .futunn.com/en/post/75068082/ubs-group-finds-60-have-already-started-curbing-ai-spending?level=2&data_ticket=1780870170397383

Nick Sleep didn't hire researchers, count cars, or call suppliers before buying Costco.

He just saw what everyone else overcomplicated — and made 4x.

A piece on why judgement and patience beat information in modern markets:

https://t.co/LdfU9BYnoY

@filippogarba@SouthernValue95 His view was that Microsoft's core business franchises are more prone to AI disruption vs. Google which is likely to reinforce its competitive advantages because of it. Personally, I'm not convinced that Office gets it lunch eaten by the LLMs.

@cloneinvestor Hey! Thanks for sharing my post. Learnt a lot from the conference and it was great to hear Chris and the investment team present their views.

TCI's Chris Hohn on $GOOG and financial infrastructure ($V $MA $MCO $SPGI $DB1

"Within the technology sphere, TCI maintains positions in Google and SAP. Whilst they didn’t really discuss SAP, they seemed quite bullish on Google and its prospects in AI. Notably, they pointed out that unlike its peers, Google has a strong presence across every layer of the AI stack and that AI was a self-reinforcing competitive advantage in its other businesses e.g., AI has made the search business even better for users and customers. TCI project Google Cloud to grow at a 45% p.a. rate to 2030 and see it as one of the big winners in AI."

"There was quite a bit of discussion around businesses in what TCI labels financial markets infrastructure – Visa, S&P Global, Moody’s, Deutsche Borse. The common seam through these discussions was the standards/protocol nature of these businesses which makes them near impossible to disrupt. All the while, most of these companies seem to be trading at decades low valuations on the fear of AI disruption from the market. TCI’s conviction here was evidenced by the increased allocation of capital to these businesses which the firm hopes will generate a high-teens net IRR over the next five years."

https://t.co/KpfPGSItvX

Chris Hohn just told a room of allocators he's "scared" of this market.

Then he showed us the portfolio he's hiding in and why he dumped Microsoft.

My notes from TCI's investor conference below:

https://t.co/7VgBN9FmuR

Like a moth drawn to a flame, I couldn't help myself and had to get a word in about IPOs.

Read my latest article on Substack for free!

https://t.co/c0M46rMhQx

I've increasingly become more bearish on my position in Microsoft.

Check out my free Substack article where I go into depth about this.

https://t.co/Fl4XiaVeTR