Inference will never be the same: Etched invented two new ways to massively improve compute cost, speed, and per watt efficiency: low voltage inference (more FLOPs) and cluster scale memory (memory/bandwidth)

The combination runs trillion-parameter models at over 80% MFU, where today's GPUs deliver 20 to 50%.

"Everyone said you can't run at voltages lower than GPUs. That was dissatisfying, because plenty of other chips already do.

Bitcoin miners run at under a quarter of the voltage of GPUs. We found a new mechanism to run at much lower voltages, and we think all AI chips in the future will be low voltage chips.

People ask how much memory bandwidth is on your chip. You should be asking how much is on your full scale-up cluster.

We added far more bandwidth at much lower latency from chip to chip."

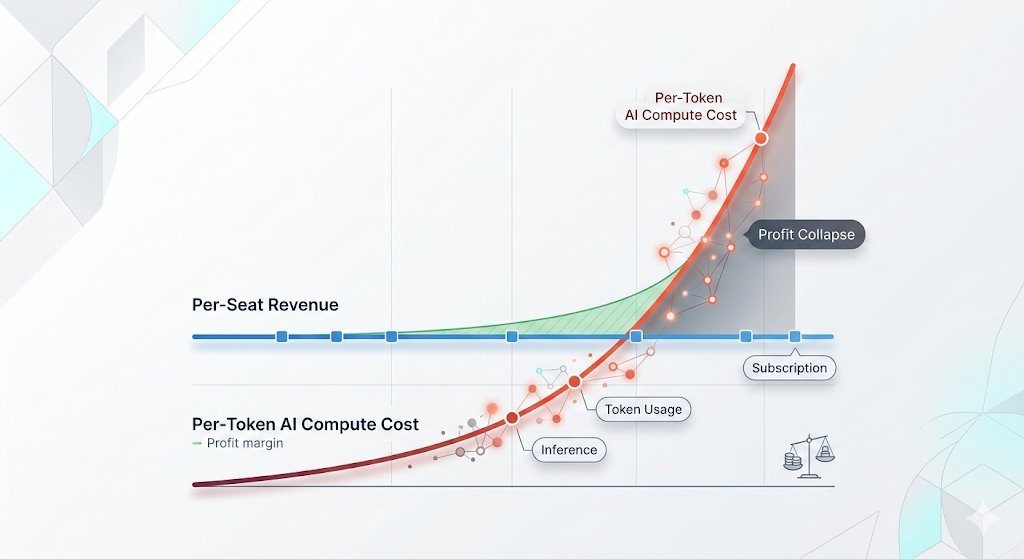

How to keep AI spend flat while token usage grows exponentially: Not with friction and spend alerts. With better defaults, routing, and caching.

Better Defaults (not Usage Caps) – Engineers can choose any model they want, but defaults matter. We’re experimenting with defaulting to open weight models like GLM 5.2 and Kimi 2.7 through our LLM gateway, while still encouraging engineers to choose the right model for the task. 91% of our employees were never hitting their usage caps, so instead of lowering caps and driving up alerts, we're moving to cheaper defaults. Note that code reviews use a diversity of models, so they can check each other's work.

Better Routing – In our custom harnesses, we preprocess prompts and route to the best model for the job, considering cache hits and model pricing. For instance, you may want a frontier model for planning, but not for execution where they can be overkill. Ultimately, humans shouldn't be choosing models - AI can automate this task.

Better Caching – Cache misses are the easiest way to drive your cost up. All of our requests are cache aware, so we’re reusing a warm cache wherever possible. For example, our cache hit rate went from 5% → 60% in LibreChat once properly implemented.

Keep Context Lean – Start fresh sessions when switching tasks. Scope file context narrowly. Disconnect unused tools. Don't just compact. The goal isn't fewer tokens used, it's fewer tokens wasted.

Better Visibility – Our engineers can use as many tokens as they want, from whatever model they want, but we’ve made usage visible – and the more you spend on AI, the more impact we expect.

The goal isn't to suppress usage. It's to build the infrastructure that makes exponential growth sustainable.

Putting this into practice has cut our AI spend nearly in half, while our token usage continues to grow.

CONTRACT MANUFACTURING AND US AI HARDWARE PRODUCTION

FLEX AND SANMINA RECEIVE A DIRECT AI SYSTEM MANUFACTURING READ-THROUGH (READ-THROUGH 11)

Affected companies: Flex Ltd. (FLEX: US), Sanmina Corporation (SANM: US)

Directional impact and magnitude: Positive, medium for Sanmina due to new supplier addition; positive, low-to-medium for Flex due to existing scale and broader revenue base.

Near-term trading catalyst versus longer-duration fundamental shift: Near-term catalyst is positive for AI manufacturing order visibility and customer validation. Longer-duration fundamental shift is positive if Cerebras scales CS-3 deployments materially and maintains US-based system manufacturing.

Supporting call evidence: Management said Cerebras manufactures CS-3 systems in the US and, “to the best of my knowledge, we are the only accelerator maker to manufacture exclusively in the US.” Feldman added, “We have added hundreds of thousands of square feet of manufacturing and clean room space to support our growth. We’ve expanded our partnership with Flextronix and are proud to have added Sanmina as our second major contract manufacturer.”

Transmission mechanism: Cerebras’s growth translates into system-level manufacturing demand for contract manufacturers with capability in complex electronics, clean room assembly, supply chain management, and US-based production. Flex benefits from an expanded relationship, while Sanmina benefits from becoming a 2nd major contract manufacturer. The addition of Sanmina also indicates that Cerebras is scaling beyond a single-manufacturer model, which supports a larger production plan and reduces operational risk.

The read-through is direct and high quality because the supplier names were explicitly disclosed. The impact is still moderated by customer concentration and the need for Cerebras to convert backlog into deployed systems, but the manufacturing signal is clearly positive.

TELECOM AND GEOGRAPHIC INFRASTRUCTURE

BELL CANADA VALIDATES TELCO-OWNED POWER, FIBER, AND REAL ESTATE AS AI INFRASTRUCTURE ASSETS (READ-THROUGH 12)

Affected company: BCE Inc. (BCE: Canada)

Directional impact and magnitude: Positive, low-to-medium for BCE at the consolidated level; potentially positive, medium for the strategic value of telco infrastructure assets.

Near-term trading catalyst versus longer-duration fundamental shift: Near-term catalyst is modest because financial contribution is not quantified. Longer-duration fundamental shift is positive because telcos with power access, fiber, land, and enterprise relationships may monetize infrastructure through AI hosting partnerships.

Supporting call evidence: Feldman referenced “a 120 megawatt deal with Bell Canada” and said the facility “does have room to expand.” Management also highlighted Canada as one of the regions where Cerebras has added data center capacity.

Transmission mechanism: AI data centers require power, land, fiber, and operational reliability. Telcos often own or control strategic fiber routes, real estate, and enterprise connectivity relationships. The Bell Canada reference indicates that telecom infrastructure can become a monetizable AI hosting asset rather than a declining legacy connectivity business. For BCE, the direct financial impact may be limited relative to the company’s total revenue base, but the strategic implication is meaningful: underappreciated telco infrastructure can be repurposed into AI data center capacity.

The geographic signal is also important. Canada, the Nordics, and other power-rich/cooling-advantaged regions may become more valuable as AI inference capacity expands globally. This supports a broader portfolio screen for telecoms, utilities, and infrastructure owners with stranded or under-monetized powered real estate.

ENTERPRISE SOFTWARE, AI APPLICATIONS, AND AGENTIC WORKFLOWS

FASTER INFERENCE IS A POSITIVE FUNDAMENTAL INPUT FOR ENTERPRISE AI APPLICATION ADOPTION (READ-THROUGH 13)

Affected companies: ServiceNow (NOW: US), Salesforce (CRM: US), Microsoft (MSFT: US), Adobe (ADBE: US), Intuit (INTU: US)

Directional impact and magnitude: Positive, low near term; positive, medium longer term for enterprise software companies with agentic workflows, copilots, customer-service automation, creative AI, and workflow automation.

Near-term trading catalyst versus longer-duration fundamental shift: Near-term catalyst is limited because the call does not provide direct software vendor customer wins. Longer-duration fundamental shift is positive because lower latency and better guardrail performance can increase AI feature usage, task completion, and enterprise willingness to deploy agents in production.

Supporting call evidence: Feldman said, “Speed enables agents to complete tasks faster.” He also argued that speed makes frontier models interactive and increases productivity. On safety, he said guardrails add compute and traditionally force a trade-off between safety and user experience, but “Cerebras eliminates this trade-off” because fast inference allows guardrails to work “without inserting crippling delays.”

Transmission mechanism: Enterprise AI adoption is constrained not only by model accuracy and cost but also by latency, user experience, and the operational burden of safety guardrails. If inference becomes materially faster, enterprise applications can run more complex agentic workflows without making users wait or disabling necessary safety layers. That supports higher AI usage, deeper workflow integration, and stronger monetization for software vendors that can turn lower-latency inference into differentiated product experiences.

The read-through is positive but longer duration. It does not create an immediate estimate revision for ServiceNow, Salesforce, Microsoft, Adobe, or Intuit. It does, however, support the broader thesis that faster inference can expand the practical scope of enterprise AI beyond chat interfaces into real-time workflow execution.

AI SAFETY AND GOVERNANCE

LOWER GUARDRAIL LATENCY IS POSITIVE FOR ENTERPRISE AI DEPLOYMENT, BUT NEGATIVE FOR VENDORS RELYING ON SLOW, COMMODITIZED INFERENCE (READ-THROUGH 14)

Affected companies: Microsoft (MSFT: US), Alphabet (GOOGL: US), ServiceNow (NOW: US), Salesforce (CRM: US), Palantir Technologies (PLTR: US)

Directional impact and magnitude: Positive, low-to-medium for AI platforms with enterprise governance layers; negative, low for commodity AI service providers that cannot match latency while maintaining safety.

Near-term trading catalyst versus longer-duration fundamental shift: Near-term catalyst is low because this is a product-quality and adoption read-through, not an immediate financial datapoint. Longer-duration fundamental shift is positive for enterprise AI platforms that can combine fast inference with auditable guardrails, permissioning, and workflow controls.

Supporting call evidence: Feldman stated that guardrails “add a layer of compute on top of the AI to create a safer experience,” and that this compute “takes time.” He said traditional guardrails create a trade-off “between safety and user experience,” but argued Cerebras can allow AI to be “safer and more productive” when it is “blisteringly fast.”

Transmission mechanism: Enterprise customers often require security, governance, auditability, policy enforcement, and domain restrictions before deploying AI into production workflows. These controls add latency and can reduce usability. Faster inference lowers the adoption penalty from governance. That benefits enterprise AI platforms and software vendors that can bundle governance with high-value AI workflows. Conversely, commodity inference platforms that compete only on access or price may become less competitive if they cannot deliver both low latency and safe execution.

The read-through reinforces a broader market point: the winning enterprise AI stack is unlikely to be only the cheapest token. It will likely be the fastest safe token integrated into workflow, identity, data, and governance systems.

AI INFRASTRUCTURE ECONOMICS AND CAPACITY OWNERSHIP

RENTED CAPACITY ECONOMICS CONFIRM THAT AI INFRASTRUCTURE SCARCITY IS TRANSFERRING MARGIN FROM CLOUD OPERATORS TO CAPACITY OWNERS (READ-THROUGH 15)

Affected companies: Digital Realty Trust (DLR: US), Equinix (EQIX: US), Iron Mountain (IRM: US), CoreWeave (CRWV: US), Nebius Group (NBIS: Netherlands), Oracle Corporation (ORCL: US)

Directional impact and magnitude: Positive, medium for owners of scarce data center capacity; negative, medium for AI infrastructure operators that must rent capacity to meet customer commitments.

Near-term trading catalyst versus longer-duration fundamental shift: Near-term catalyst is negative for AI cloud margin expectations and positive for data center leasing economics. Longer-duration fundamental shift depends on whether AI infrastructure platforms can transition from expensive rented capacity to owned or contracted lower-cost capacity quickly enough to preserve margins.

Supporting call evidence: Bob Komin said Cerebras is “temporarily renting our own systems back from an existing customer” to accelerate service availability. He stated that the additional cost of renting third-party capacity will depress cloud and services margin by “10 to 15 margin points” before margins begin ramping back toward the 60%+ target. He also confirmed that these rental costs are baked into 2Q26 and full-year guidance.

Transmission mechanism: When AI infrastructure companies cannot deploy owned capacity fast enough, they must rent scarce capacity at unfavorable economics. That transfers margin to capacity owners and validates pricing power for data center landlords, hosting providers, and customers with deployable systems. For GPU cloud companies and AI infrastructure operators, the risk is that headline demand growth does not translate into expected gross margin if capacity must be rented or if deployment delays persist.

This read-through is highly actionable because it connects demand strength to margin pressure. The market should not treat AI infrastructure revenue growth as automatically high margin. In a capacity-constrained environment, the owner of power and deployment capacity can capture a disproportionate share of economics.

OVERALL CROSS-PORTFOLIO CONCLUSION

The highest-conviction positive read-throughs are for powered data center capacity, electrical and thermal equipment, TSMC’s role as a broad AI foundry partner, AWS’s 2027 enterprise inference positioning, and direct contract manufacturers Flex and Sanmina. The highest-conviction negative read-throughs are for the uncontested-GPU inference narrative, AMD’s AI GPU catch-up thesis in latency-sensitive inference, GPU-only AI cloud platforms, and the assumption that HBM remains a universal gating factor across all AI compute architectures.

The most important market implication is that AI infrastructure is becoming more heterogeneous, not less. Training, prefill, decode, cloud distribution, data center ownership, and power availability are separating into distinct profit pools. Cerebras’s call suggests that the next phase of AI infrastructure investing should distinguish between companies that own scarce physical capacity, companies that enable deployment, companies that control enterprise cloud demand, and companies whose accelerator economics depend on maintaining architectural dominance.

Met a guy making $1.6 million a year.

Three days ago he was at a Meta conference. Told me he saw the best AI talk of his life.

Boris Cherny was on stage. Showed how the Anthropic team actually uses Claude day to day.

Boris deleted his IDE eight months ago. Now he codes from his phone.

I watched it last night. Had to pause it twice.

Not because it was hard. Because I realized I've been using Claude like a toy.

He sent me the recording. It was never published.

Posting it below.

Karpathy just said the people who don't use LLMs are already losing

he spent 4 minutes explaining why smart people are still going to fall behind

not only the people who refuse AI, but also those who think signing up for Claude counts as using it

typing a prompt and reading what comes back isn't the skill, anyone can do that

the real shift is going from asking AI things to building something that runs without you

that's exactly why I wrote an article on Claude features most people don't even know exist

read the article below and you'll already be ahead of 99% of people

So DCs are a national interest but at the level of local gov they’re likely to encounter opposition. AFAIK DCs don’t lead to massive local wealth creation, and taxing them on top of expensive energy would meaningfully impact cycle value.

So if national governments want sovereign AI, will they need to throw money at provinces that have/can rapidly build power infra?

NVIDIA QUIETLY DROPPED A $249 BOX THAT REPLACES YOUR $200/MONTH OPENAI SUBSCRIPTION WITH $2 IN ELECTRICITY

it's called the jetson orin nano super. smaller than a wallet, runs at 25 watts, does 70 trillion ai operations per second. runs llama 3, mistral, gemma and deepseek locally with no api fees and no data leaving your house

a developer running automations and coding assistants pays $200 a month to openai. the same workload on this box costs $2 a month in electricity and breaks even in 10 weeks

install ollama with one command. change one line in your code. point it at localhost instead of openai. everything else works identically

7 billion parameter models handle 80% of what people use chatgpt for. summarization, drafting, coding, document q&a, automation pipelines. total monthly cost drops from $200 to $22

cloud subscriptions keep getting more expensive and rate limits keep getting tighter. the people who set this up in 2025 are going to look very smart in 2027

bookmark this and read the article below

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

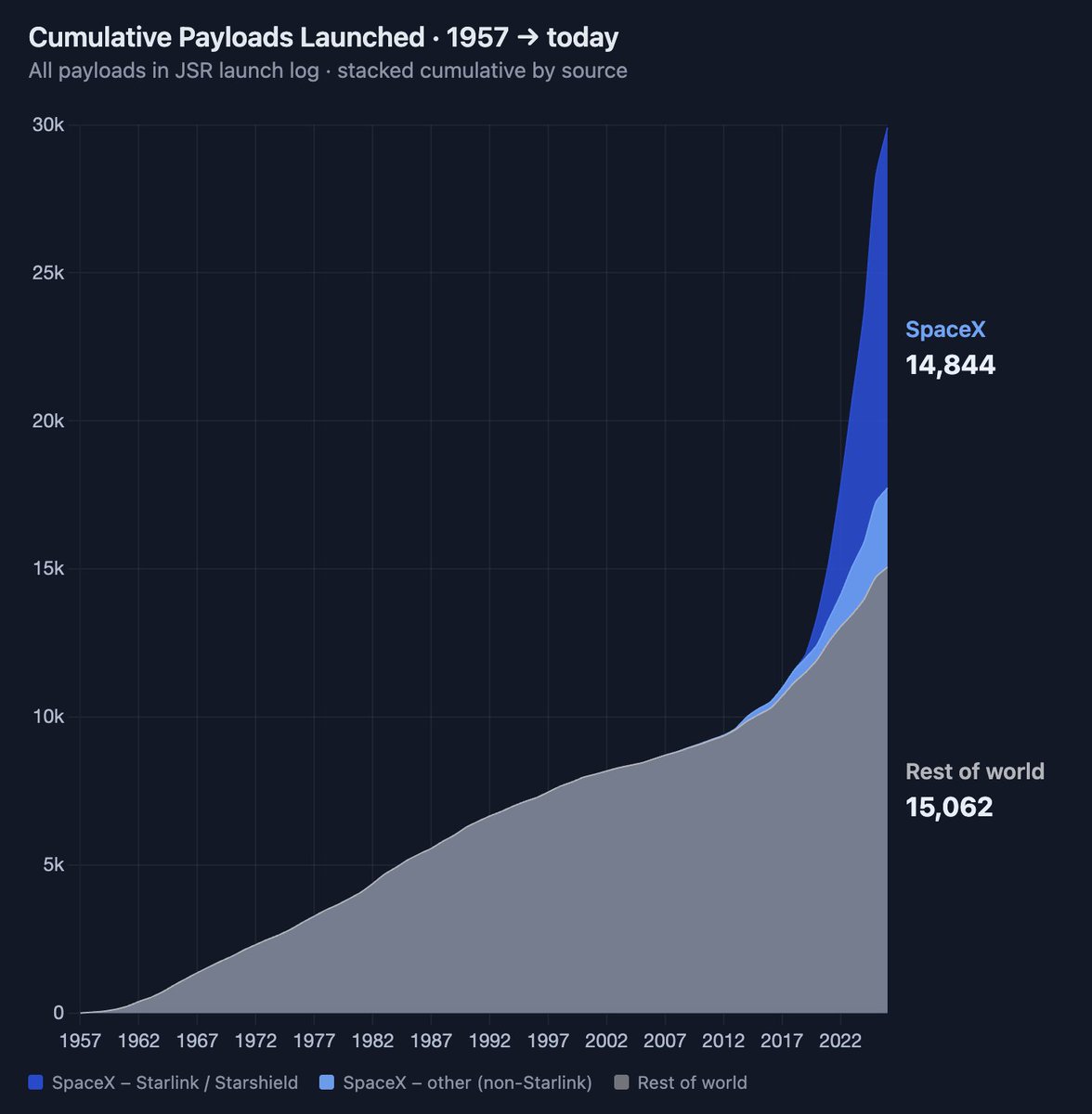

SpaceX is only ~200 satellites away from having launched as many satellites as the rest of the world combined

(despite giving the rest of the world a 61-year head start)

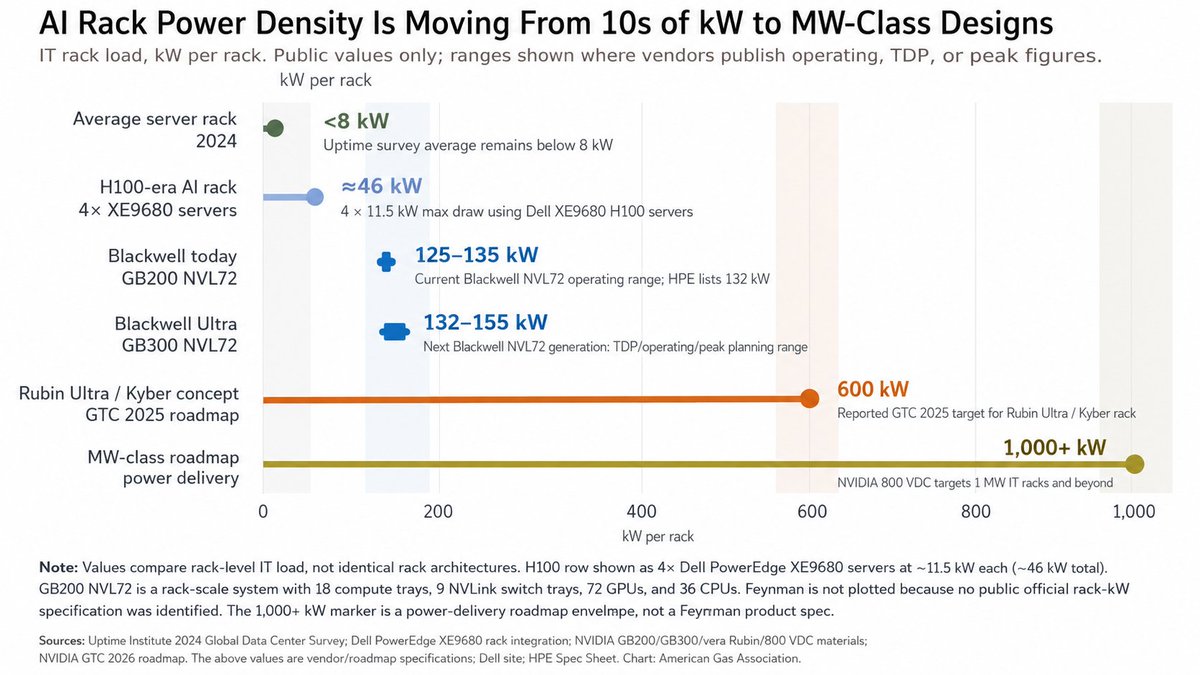

Data center compute racks used to need single-digit kilowatts of power.

Today, the top-of-the-line AI GPU racks require 100+ kW.

Very soon, a single rack of next-gen GPUs will consume about 600 kW of power.

Then megawatt-scale is coming.

For decades, data center racks have been powered by three-phase AC, the same kind of power that runs industrial machinery. NVIDIA's next AI rack uses 800-volt DC instead, the same standard NVIDIA itself credits to the electric vehicle and solar industries.

The change re-architects how electricity moves from the grid to the GPU, and three things at the silicon level had to happen first.

1️⃣ Doubling the voltage halves the current for the same power delivered, which cuts resistive losses in copper by roughly 75 percent. NVIDIA's design partners estimate copper thickness can drop by up to 45 percent across the rack. A 1MW rack needs up to 200kg of copper busbars at the legacy 54-volt distribution standard. A single 1GW data center built that way would need up to 200,000kg of copper for rack busbars alone, per NVIDIA's own technical blog.

2️⃣ The power semiconductors needed to convert 800 VDC efficiently at the rack level matured only in the last few years. Silicon carbide handles the high-voltage front-end conversion from medium-voltage utility AC down to 800 VDC. Gallium nitride handles the high-frequency stepdown from 800V to intermediate buses (50V, 12V, or 6V) feeding the GPU. Both are wide-bandgap technologies. SiC scaled because of the EV industry, where Porsche, Hyundai, Kia, and BYD have built the 800V powertrain supply chain over the last five years. GaN scaled on the back of consumer fast-charging and is now being adapted for AI infrastructure.

3️⃣ AC-to-DC conversion moves out of the IT rack entirely. In a current GB200 NVL72 or GB300 NVL72, up to eight power shelves sit inside the rack converting AC to DC. At MW scale on the same standard, those shelves would consume up to 64U of rack space, leaving no room for compute. In the 800 VDC architecture, conversion happens once at a dedicated power shelf upstream, and the IT rack receives DC directly. NVIDIA estimates this delivers up to 5 percent end-to-end efficiency improvement and up to 70 percent reduction in PSU-related maintenance costs.

Power semiconductor content per rack grows substantially across this transition. SiC and GaN suppliers, high-voltage busbar and connector vendors, and rack-level DC-DC converter makers gain share. The legacy low-voltage and multi-stage AC conversion stack loses share.

Most colocation facilities today operate at 10 to 30 kW per rack. The 600kW Rubin Ultra rack is more than an order of magnitude above that. The math operators are working on for 2027 deployments is whether their existing PDUs, busways, and rack power shelves are even compatible with the new spec.

🚗 Top 20 Best-Selling Electric Vehicles in the World

March 2026

1. 🇺🇸 Tesla Model Y – 118,531 units

2. 🇺🇸 Tesla Model 3 – 53,158 units

3. 🇨🇳 Geely Xingyuan / EX2 – 34,146 units

4. 🇨🇳 BYD Song / Seal U – 34,011 units

5. 🇨🇳 BYD Yuan Up / Atto 2 – 33,934 units

6. 🇨🇳 BYD Seagull / Dolphin Mini – 31,076 units

7. 🇨🇳 Li Auto L6 – 24,198 units

8. 🇨🇳 BYD Dolphin – 23,529 units

9. 🇨🇳 BYD Seal 06 – 20,635 units

10. 🇨🇳 BYD Sealion 06 – 19,662 units

11. 🇬🇧 MG 4 – 17,409 units

12. 🇨🇳 Wuling Mini EV – 16,815 units

13. 🇨🇳 Deepal S05 – 16,395 units

14. 🇨🇳 NIO ES8 / EL8 – 16,272 units

15. 🇨🇳 BYD Qin Plus – 15,973 units

16. 🇯🇵 Toyota bZ4X – 15,683 units

17. 🇨🇳 BYD Yuan Plus / Atto 3 – 15,014 units

18. 🇨🇳 Fang Cheng Bao Tai 7 – 14,197 units

19. 🇨🇳 Leapmotor C10 – 13,879 units

20. 🇨🇳 Xiaomi YU7 – 13,561 units

(Source: CleanTechnica, March 2026 data)

The S&P is 45% AI and 4% energy.

The market is massively long the output.

Massively short the input.

AI runs on power.

Every dollar flowing into Nvidia eventually flows into a gas turbine, a transformer, or a transmission line.

The market has built a portfolio that ignores its own supply chain.

I wrote about it, in my latest article, link in replies 👇

One of the most substantive and eye-opening MS&E 435 classes yet. Thanks @ChaseLochmiller for walking us through the economics of AI datacenters from Abilene to Claude, TX. From Everest to the Hewlett 201 desk, the man keeps finding new summits 🏔️