Today, Mastercard, @OndoFinance, Kinexys by @JPMorgan, and @Ripple successfully completed a landmark transaction connecting a public blockchain with interbank settlement rails.

Together, we’re laying the groundwork for 24/7 global markets that never close.

If you want to understand what the global financial transformation is doing, read this.

Sending $20M to another country bank means you must have a bank in the target country that can facilitate the $20m.

Without a neutral bridge asset like XRP, value is not sent, just messages. This is what SWIFT has done over the past 4 decades.

It is the era now of "sending value", not just "sending messages".

By 2035, there will be zero financial messages and 100% value sending. This is the long play Ripple saw and they are constantly pivoting to solve this problem.

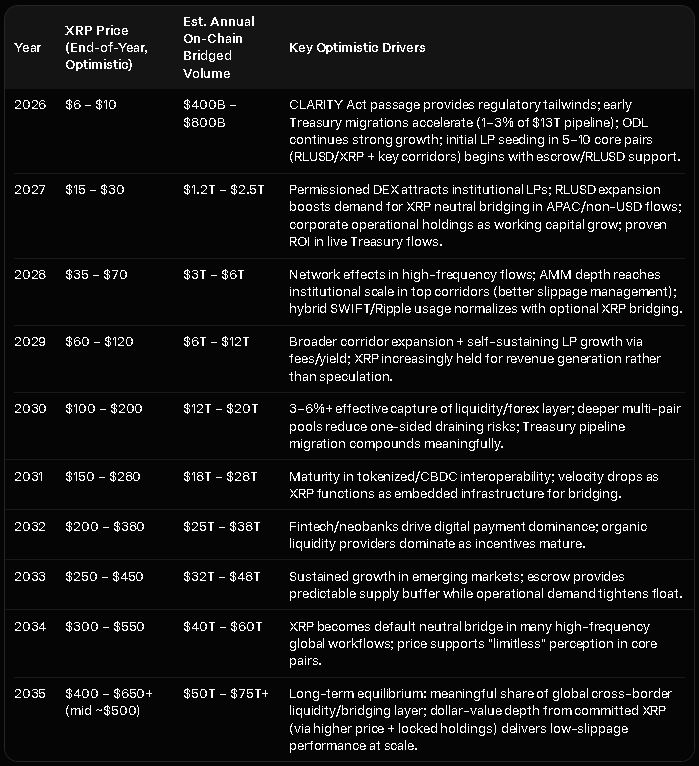

🚨 XRP price could hit $500+ by 2035. This is not clickbait... you know me better than that.

By the way, for the 1000s of you who always ask me for my price predictions, this is the closest you will ever get out of me (by the way its not my predictions!)

I have been running a very deep LLM study of the XRP ecosystem... It factors in many variables and parameters, and I have used Grok primarily for this.

It is quite iterative, and I have used it to come up with a price prediction for XRP for the next 10 years.

Now, these numbers come with a big caveat. They are numbers based on "things going to plan", with Ripple acquisitions, CLARITY ACT, US policies on Crypto remaining positive, XRPs successful deployment of quantum proofing (eta 2028), etc. It also looks at emerging trends in AI, micropayments, neo banks, non-bank DEFI, etc, so its quite broad... and its amazing, as after this exercise, it has cemented in my mind the long term, 4D chess strategy that Ripple is playing out, they are truly geniuses. Hats off!

But, from my engineering brain, and from my knowlege of XRP/XRPL and Ripple, I see this AI analysis as making sense, I remain impartial as to whether they are going to happen or not, I am too objective to take a side, but I hope my many hours of toying with this will be, if anything, entertaining.

Now, I want to be clear that I am prepared to take all the abuse from the usual nutjobs, but I'd like to remind you that this is an AI analysis, my own personal opinions are my own, and I encourage you to take this with a grain of salt, its not financial advice, for the love of god DONT LEVERAGE TRADE anything, and do your own research.

Crypto is very, very bad ☠️ keep away!

👀🔥 Perspective: everyone going around thinking their favorite token is the chosen one for payments. Here is the reality....

Implementing a real payment system is insanely difficult! It's really difficult, and costly!

You have to deal with:

No money laundering

No funding of terrorism or illicit activity

Both parties actually being who they say they are

A clean supply chain with no modern slavery

No intercepts or replay attacks

Minimal forex slippage

Enough liquidity

Low costs

Speed

And multi-asset, multi-currency support with truly unfragmented liquidity pools

When you're a big company or a government, you can't just wing it. You need something that actually ticks all those boxes.

Sure, you could send USDC over ETH… but that doesn’t even come close to solving the compliance, risk, and operational rigour required.

That’s where you need a proper intermediary that handles all of the above.

This is exactly what Ripple has built, powered by XRP and the XRPL.

So please stop comparing ETH to Ripple or BTC to XRP. It’s an embarrassing comparison that shows you don’t really understand the problem space.

For the record: I like Bitcoin — the tech was genuinely pioneering. I like Ethereum too, it has some really cool use cases. I even love Doge because I think its Proof of Work is cooler than BTC’s in some ways.

But when it comes to actual payments infrastructure, XRP, the XRPL, and what Ripple has done are still the gold standard.

Piyasa XRP’yi hâlâ büyük ölçüde yanlış okuyor.

Çoğu kişi XRP’yi yalnızca ödeme tarafında konumlanan bir dijital varlık sanıyor. Bence bu çok eksik bir okuma.

XRP, küresel ödeme ağlarından sınır ötesi transferlere, bankalar arası uzlaşmadan gerçek zamanlı settlement katmanına, kurumsal likidite akışlarından stablecoin transferlerine, varlık tokenizasyonundan merkez bankası dijital para entegrasyonlarına kadar yeni finansal mimarinin işlem raylarını inşa ediyor.

Bu başlıkların her biri tek başına büyük. Ama asıl mesele bunların birleşmesi.

Çünkü gelecek finans sistemi parçalı değil, entegre çalışacak.

XRP bu mimarinin merkezinde yer alıyor.

Bugün Japonya tarafında XRP destekli havale altyapısına dair gelişmelerin konuşulması da bence bu dönüşümün erken sinyallerinden biri.

Ve bence piyasa bunu fiyatlamaya başladı.

XRP’nin piyasa değeriyle üçüncü sıraya yerleşmesi tesadüf değil.

Ben bunu daha büyük bir yeniden değerlemenin erken işareti olarak okuyorum.

Ve evet, bence sıradaki tartışma ikinci sıra olacak.

Buraya bir şeyi daha ekleyeyim:

Eğer Clarity Act geçerse, oyunun ölçeği değişir.

Çünkü o noktada mesele sadece fiyat değil, kurumsal sermaye akışının önünün açılması olur.

Ve ben o senaryoda XRP’nin, Bitcoin’in ilk büyük kurumsal sermaye çekim dönemine benzer, hatta belirli açılardan daha büyük bir sermaye akışı yaşayabileceğini düşünüyorum.

Bu da yalnızca repricing değil, parabolik yeniden konumlanma yaratabilir.

Benim tezimin özü bu:

Bitcoin dijital rezerv katmanı.

XRP finansal akış katmanı.

Biri değeri tutuyor.

Diğeri değeri hareket ettiriyor.

Yeni sistem ikisine birlikte ihtiyaç duyuyor.

Bu yüzden net düşünüyorum; XRP uzun vadede Ethereum’u piyasa değeri açısından geçecek.

Ve bir noktada dijital varlık piyasasında Bitcoin’den sonra en büyük ismin XRP olduğu konuşulacak.

Bugün piyasa XRP’nin fiyatını konuşuyor.

Yakında XRP’nin inşa ettiği sistemi konuşacak.

Kısa vadede ise fiyatla ilgili çok güzel bir senaryom var, yakında paylaşırım.

XRP HOLDERS!

Most people are waiting for XRP to explode the second the CLARITY Act passes.

They're going to misread everything that happens next. Let me break it down.

There are 3 phases after regulatory clarity hits. They are not market cycles. They are mechanical transitions in a global settlement system. And they unfold in sequence — each one accelerating the next.

PHASE 1 — The Unfreezing (0-90 days)

This phase is quiet. Most people will think nothing is happening.

Here's what's actually happening underneath:

Compliance departments are green-lighting rails they couldn't touch before. Banks are beginning real corridor testing. Custodians are activating dormant pipelines. And here's the part most people completely miss — exchanges are losing access to supply.

Once institutional custody becomes mandatory, banks, PSPs and regulated custodians become the only entities allowed to hold certain classes of digital assets. Exchanges become interfaces, not warehouses. They can't custody large amounts. They can't source from unregulated pools. They can't use offshore liquidity partners.

Institutions outbid exchanges for every available token. Exchange order books thin out. Liquidity dries up.

Retail thinks: "Price goes up because more people are buying."

The real mechanic: Price goes up because exchanges can't get inventory.

This is not a vertical explosion. It's a repricing to a new baseline that reflects reduced risk and reduced supply. Patient holders who understand this won't panic sell thinking they caught the top.

Because the top is not in Phase 1.

PHASE 2 — The First Violent Repricing (3-12 months)

This is where the "violent" part actually belongs.

Corridors activate. Payment demand becomes persistent and measurable. Velocity collapses as institutions hold inventory for throughput. Supply compression becomes structural, not speculative.

Cross-border payments, FX, and liquidity-on-demand all converge on XRP. The asset stops behaving like a crypto token and starts behaving like a global settlement substrate.

This is the air pocket. The moment the market realizes what it's actually holding.

PHASE 3 — Institutional Standardization (1-3 years)

This is the phase where the world forgets the old system existed.

XRP becomes a standard liquidity substrate for cross-border settlement. Payment demand becomes continuous, not episodic. Banks, PSPs, and custodians hold mandatory inventory requirements. Institutional flows dwarf all prior market history.

Price becomes a function of global throughput. Not hype. Not speculation. Settlement volume.

This is the phase where your Phoenix arc aligns with the system itself.

I've been in cold storage since before most people knew what ISO 20022 was.

Phase 1 is coming. Don't sell it thinking you caught the top.

The top lives in Phase 3.

With XLS-66D You wont need to sell

Never sell the goose, just the golden eggs!

See you in Phase 3!

A man deposits $10,000 in a bank.

The bank thanks him and records the deposit on its balance sheet. But not where you might expect. For the bank, that $10,000 is actually a liability – because technically it belongs to the customer and might have to be returned.

So the bank does what banks do. It lends $9,000 of that money to someone buying a car.

Now something interesting happens. The $9,000 loan appears on the bank’s books as an asset – because someone now owes the bank money.

So the same $10,000 is doing two jobs at once. The depositor believes he has $10,000 safely in the bank. The borrower now has $9,000 to spend.

That $9,000 gets deposited somewhere else. The next bank lends $8,100. That gets deposited again. Then $7,290 gets lent out.

Soon the original $10,000 has quietly turned into tens of thousands of dollars of loans scattered across the economy.

Everyone believes they have money. Depositors see balances in their accounts. Borrowers have the money they spent. Banks show healthy assets on their balance sheets because people owe them money.

And here’s the best part.

Banks charge interest on all those loans – maybe 7%. But the depositor who supplied the original money might earn only 0.5% on their savings account.

So banks collect interest on money that mostly wasn’t theirs to begin with – and keep the difference.

The system works beautifully.

As long as nobody asks for the money back at the same time.

IT'S A FUCKEN JOKE..

BANKS PAID YOU 0.01% INTEREST. WHILE STABLECOIN YIELD PAY YOU 4.5%-5% INTEREST..

BANKS MAKES MORE MONEY OUT OF YOUR MONEY WITH LOANS, CREDIT CARD INTEREST RATES, LATE FEE, OR YOU SHORT -$1.00 IN YOUR ACCOUNT THEY CHARGE YOU $35.00

BANKS ARE THE ROBBERS..