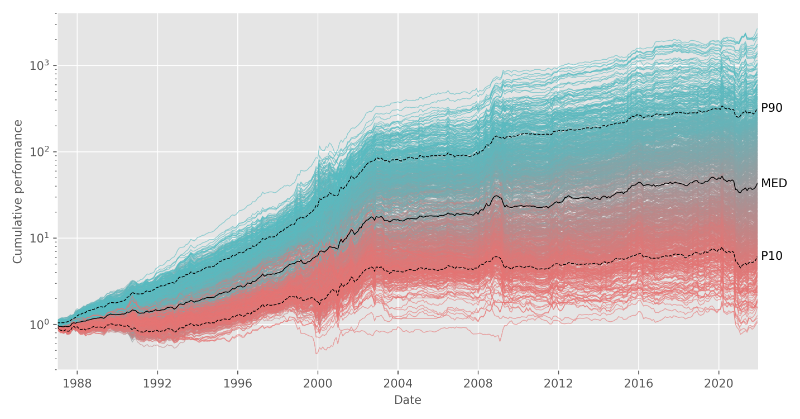

📢 NEW PAPER OUT! 🚀

We analyze 1,056 #ML models to uncover how key design choices—algorithm, target, feature, & training—affect strategy returns.

Key takeaways:

📈 Returns vary widely; see graph below!

🔍 NSE exceed SE by 59%

💡Check out which ML design choices really work 👇

The Illusion of the Carbon Premium

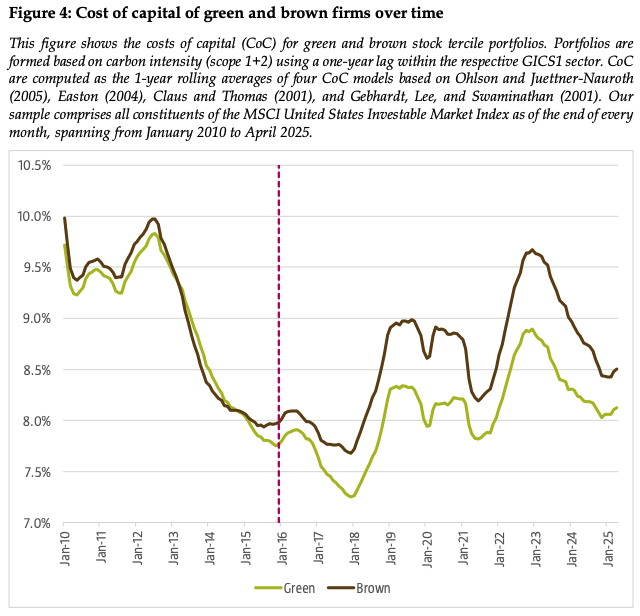

Carbon that has not yet been emitted should not be used to predict stock returns. While this sounds obvious, prior research papers has done exactly that. This critical observation forms the basis for the Robeco Institutional Asset Management research team's re-examination of the relationship between climate risk and asset pricing. Investors and academics alike have sought to understand how environmental factors influence stock returns, often assuming that higher emitters command a risk premium. However, the timing of data availability is crucial in quantitative strategy formation, and misalignments here can lead to spurious conclusions about the pricing of carbon emissions.

https://t.co/2Fkt8P21Qj

#esg #carbon #StockPicks

@systvest@Greenbackd How do you define ROIC? If you ask five different analysts, portfolio managers, or investors how to calculate ROIC exactly, you’ll likely get six different definitions! 😉

@systvest@Greenbackd Gross margin is indeed rather weak. Gross profitability (gross margin * asset turnover) is stronger. In my research, I typically find the best results for profitability measured between top and bottom line and rather in cash than in accounting terms.

The RenAIssance of the tangible economy

The Mag7 now spend more on CAPEX than on R&D.

This may create both risks and opportunities:

📉 Costly overinvestment could lower future returns

🏰 But AI CAPEX could reinforce competitive moats

https://t.co/1YCfYTRmtE

#MarketingCommunication #CapitalAtRisk

New paper: The Illusion of the Carbon Premium

Carbon that has not yet been emitted should not be used to predict stock returns. While this sounds obvious, prominent prior research has done exactly that.

What happens when using only emissions data available to investors at the time of portfolio formation?

Read the full paper on @SSRN :

https://t.co/OM1W0pte0N

The RenAIssance of the tangible economy

The Mag7 now spend more on CAPEX than on R&D.

This may create both risks and opportunities:

📉 Costly overinvestment could lower future returns

🏰 But AI CAPEX could reinforce competitive moats

https://t.co/1YCfYTRmtE

#MarketingCommunication #CapitalAtRisk

The RenAIssance of the tangible economy

The Mag7 now spend more on CAPEX than on R&D.

This may create both risks and opportunities:

📉 Costly overinvestment could lower future returns

🏰 But AI CAPEX could reinforce competitive moats

https://t.co/1YCfYTRmtE

#MarketingCommunication #CapitalAtRisk

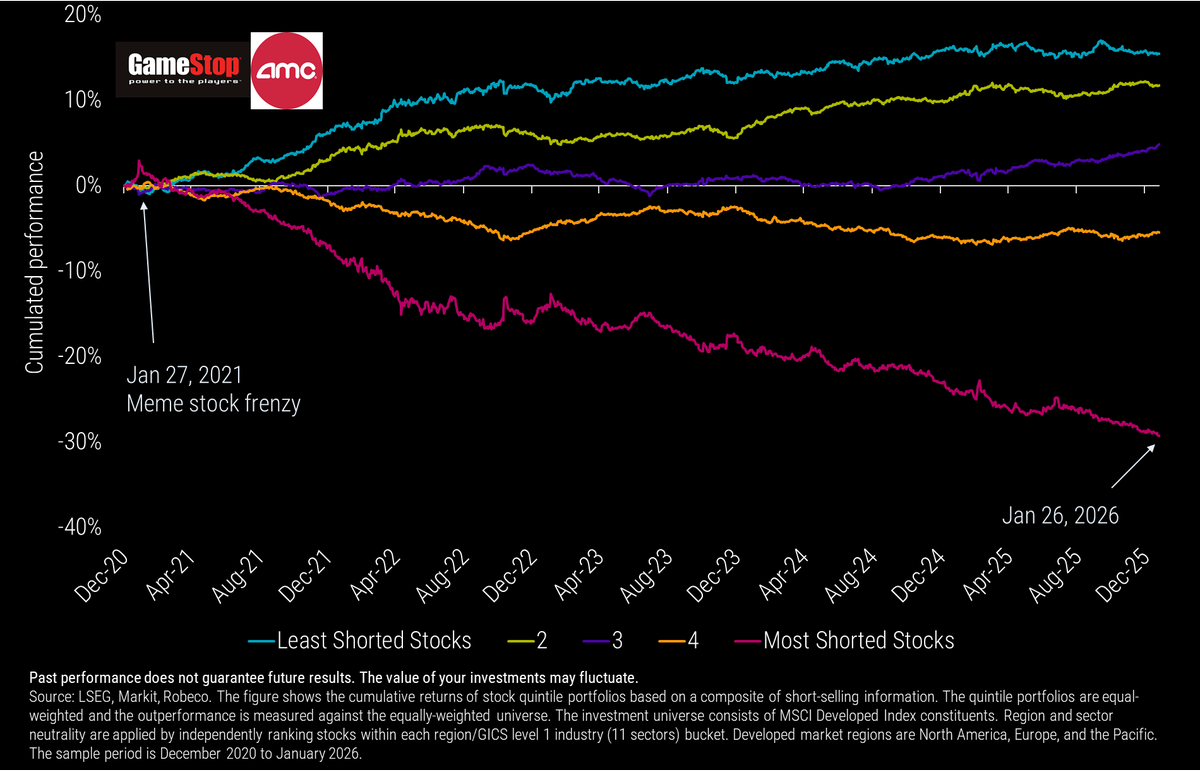

Five years ago, the #MemeStock frenzy drove markets crazy.

Five years on, the most heavily shorted stocks have underperformed, making 2021 look like a short-lived blip.

Or is the #MOASS still coming?

#MarketingCommunication#CapitalAtRisk

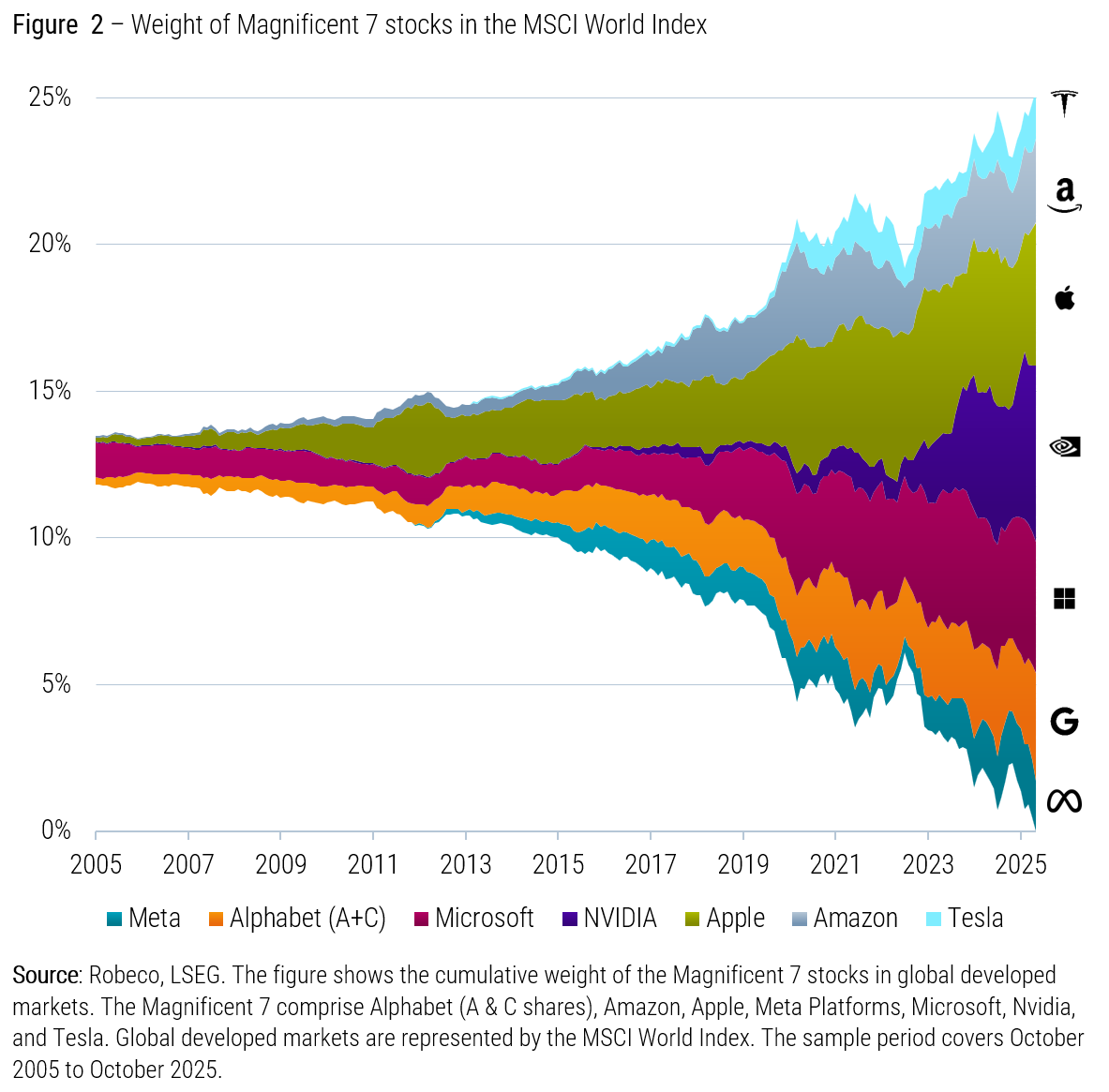

The Mag7 make up ~25% of MSCI World. Not the first time a handful of names dominate (remember Cisco, Nokia, Lucent?).

They shape the benchmark, but they don’t have to shape your alpha. Our systematic, benchmark-aware process taps the long tail instead.

https://t.co/sfCu9rKSZ9

@QCompounding For those interested in the performance of the “Magic Formula” but also other popular investing formulas, please check out our paper “Formula Investing”.

🔗 https://t.co/74lojDQmhd

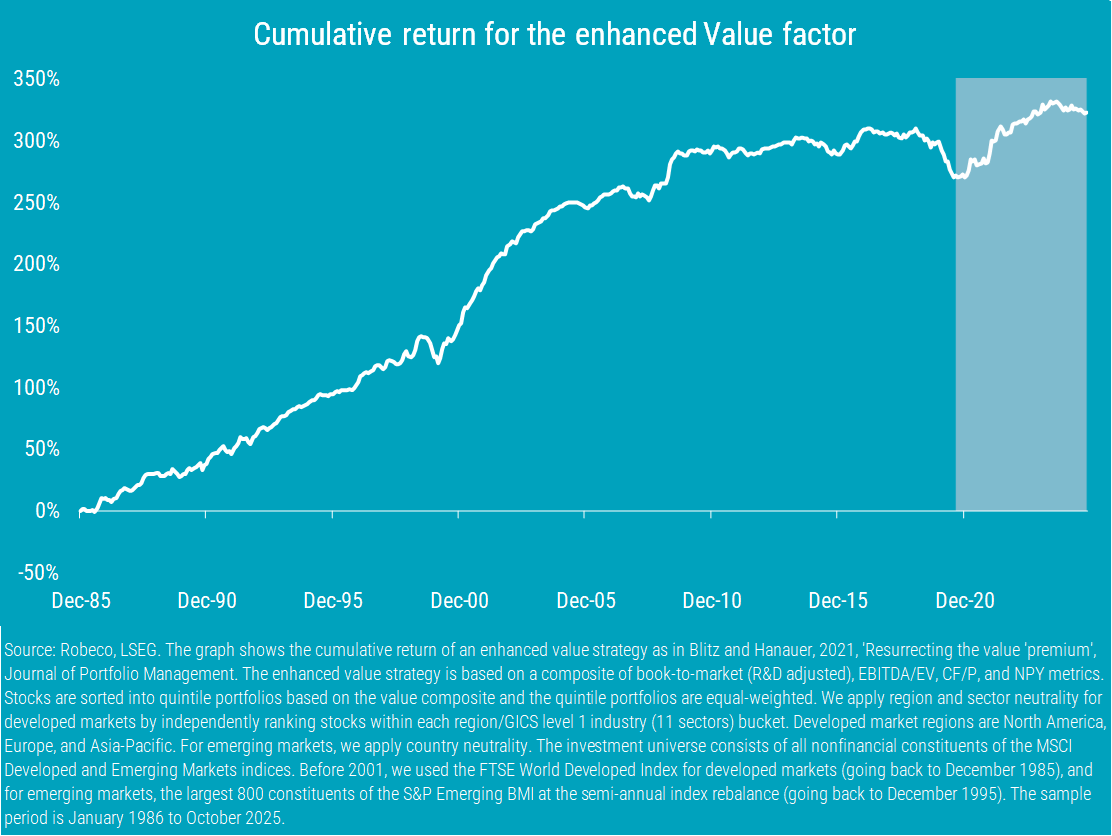

Value is not dead, but quant is more than value!

To the day five years ago, the announcement of the successful Pfizer-BioNTech COVID-19 vaccine candidate results triggered a major market rotation.

Since then, the average #value stock has outperformed the average growth stock. Below, I share four graphs showing how value has evolved since the “vaccine day.”

1️⃣ Long-term performance

The enhanced value strategy in global equity markets, as defined in my paper with David Blitz (Resurrecting the Value Premium), has delivered solid long-term returns despite the challenging 2018–2020 period. The Pfizer-BioNTech news on 9 November 2020 marked the turning point. The shaded area presents out-of-sample data after posting the value paper on SSRN in October 2020 (https://t.co/EDmHhovI9C).

In contrast, benchmark-aware approaches that take many diversified bets based on a strong quantitative model, where value is just one of many elements, have benefited from value exposure while maintaining balanced overall risk.

Taken together, these charts show that value is not dead. But they also remind us that quant investing is much more than value alone. It is about combining robust signals, continuous innovation, and adapting to new market situations.