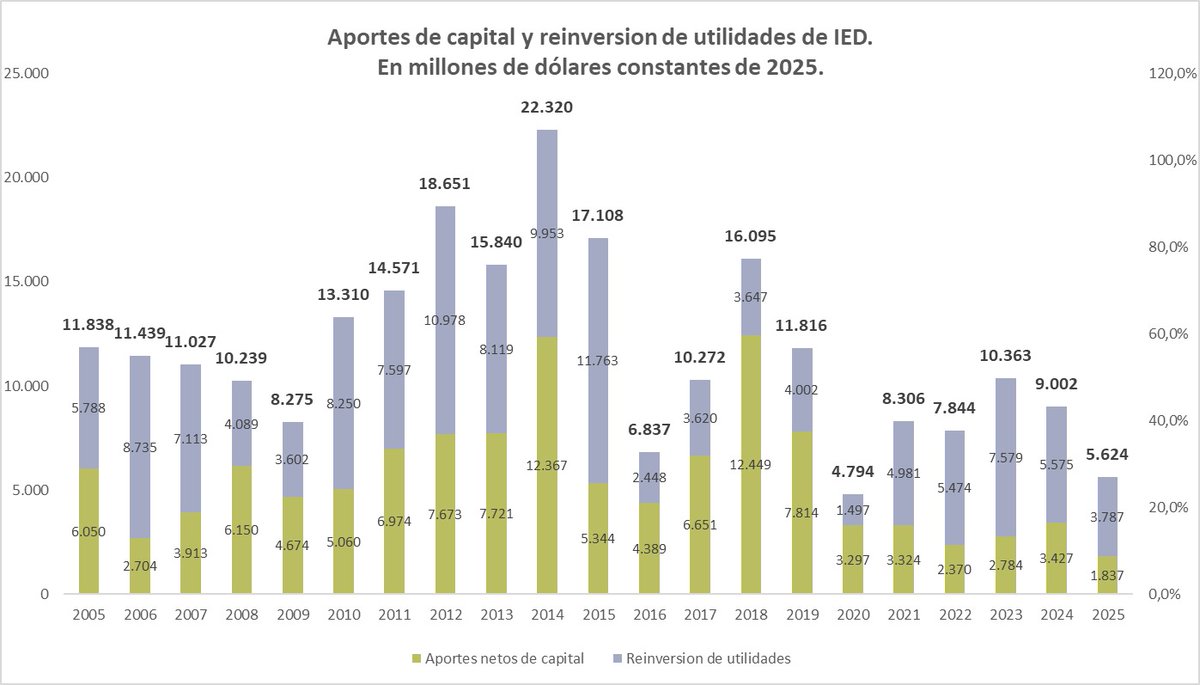

Recién sacada del horno: en esta nota trato de ilustrar la compleja situación que atraviesa de centenaria Cuenca del Golfo San Jorge tras la abrupta retirada de YPF. Desde ya, gracias a la generosidad y apoyo de @revistaanfibia! https://t.co/viYDUI7C5J

🇨🇴 67 leading international economists, scholars, and public policy figures have signed an open letter backing Colombia’s economic transformation under President Gustavo Petro, saying the country is demonstrating that “another economic path is possible” by breaking from decades of neoliberal orthodoxy.

The signatories include Thomas Piketty, Yanis Varoufakis, Jayati Ghosh, Ha-Joon Chang, James K. Galbraith, Isabella Weber, Jason Hickel, Ann Pettifor, and former Ecuadorian President Rafael Correa.

Published ahead of Colombia’s June 21 presidential runoff, the letter cites falling poverty, record-low unemployment, a rising share of national income going to workers, advances in land reform, growth in non-extractive exports, and a major expansion of renewable energy.

The vote will decide whether Petro’s project continues under his leftist ally Iván Cepeda or is reversed by far-right outsider Abelardo de la Espriella, who narrowly led the first round and has pledged a sharp turn back toward market orthodoxy.

The authors acknowledge ongoing challenges including debt, inflation, fiscal pressures, and weak private investment, but reject calls for austerity, wage suppression, indiscriminate liberalization, and deeper dependence on extractive industries.

They said Colombia’s experience carries significance beyond its borders for countries seeking development strategies rooted in redistribution, productive transformation, economic democracy, and climate justice.

Letter ⬇️

🚨 Anthropic just showed a 27-minute workshop on how to actually do prompts for Claude.

Taught by the people who built it.

Free. No registration. No paywall.

I've seen $300 courses that don't cover what they teach in the first 8 minutes.

Watch it and bookmark it now.

🚨 THE ENTIRE AI BOOM MIGHT BE BUILT ON FAKE REVENUE.

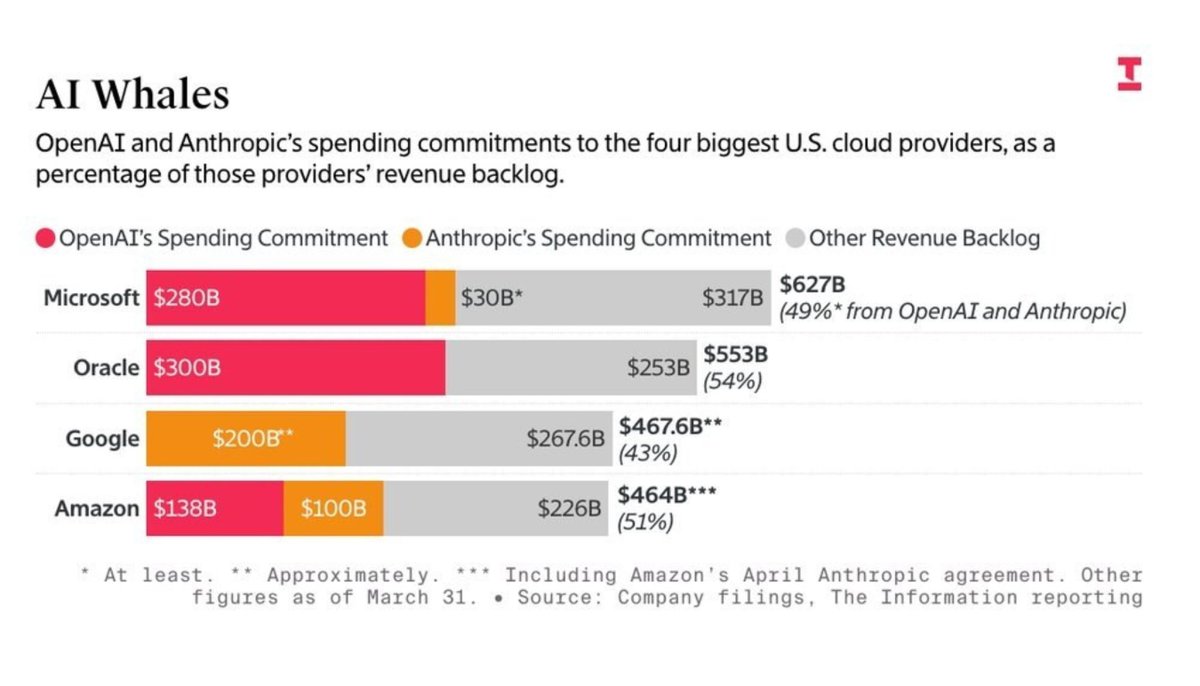

Latest corporate filings show that OpenAI and Anthropic alone make up over half of the entire $2 trillion future cloud backlog held by Microsoft, Oracle, Google, and Amazon.

This massive pipeline is actually being created through a circular accounting trick called a round trip revenue loop.

But how it works ?

A tech giant gives billions of dollars to an AI startup as an "investment". But hidden in the contract is a strict rule forcing the startup to hand that exact same money straight back to the tech giant to rent their computer servers.

Look at the documented case of Microsoft and OpenAI.

When Microsoft invested $13 billion into OpenAI, it didn't just give them cash; it gave them "cloud credits" to use Microsoft servers. OpenAI used those exact credits to train its AI models, and Microsoft then turned around and recorded that server usage as brand new "cloud revenue" from a customer.

The tech giant is literally paying itself with its own money and calling it a sale.

This is why OpenAI’s annual cloud bill has ballooned to over $60 billion, double its actual revenue of $25 billion, kept alive solely by this recycled funding loop.

Anthropic runs the exact same play, spending $2.66 billion on Amazon Web Services in just nine months, which was basically 100% of all the money it earned at the time.

This manufactured demand triggers a second accounting trick where tech giants book massive paper profits. Every time a startup gets a higher value from a new funding round, the tech giant updates the value of its investment on its books and counts that unearned paper gain as direct profit.

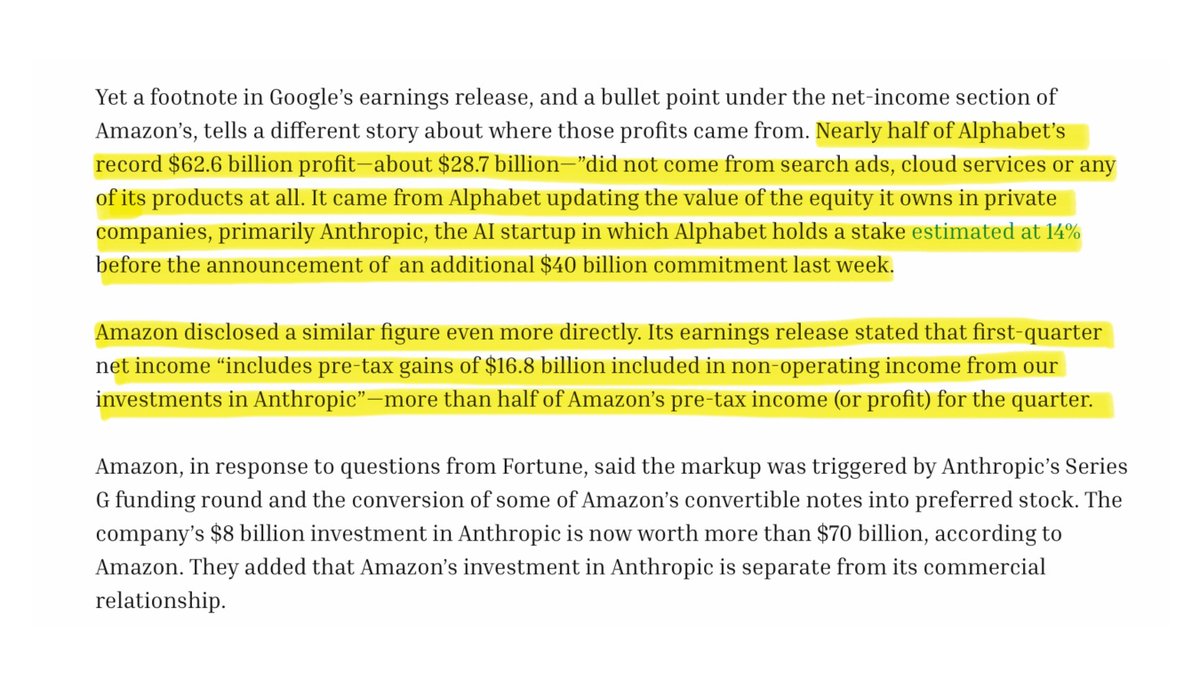

In Q1 2026, Alphabet reported a record $62.6 billion profit, but $28.7 billion nearly half, was just a paper markup on its Anthropic investment. In the same quarter, Amazon reported $30.3 billion in profit, but $16.8 billion of it was just an Anthropic paper gain.

While Amazon reported record profits, its actual free cash flow collapsed 95% to just $1.2 billion because it had to spend $44.2 billion in real cash to build physical data centers.

This has created a massive danger where these giant companies rely heavily on just one or two unstable startups. Microsoft has 49% of its $627 billion future backlog tied to OpenAI, while Oracle has an incredible 54% of its entire $553 billion pipeline relying on OpenAI alone.

This perfectly mirrors the 2001 dot-com crash when Global Crossing and Qwest Communications swapped identical fiber-optic network capacity with each other just to book fake sales.

Qwest had to erase $1.4 billion in fake income, and Global Crossing went completely bankrupt.

The only difference is that the dot-com swaps were illegal, but today's AI loop is fully legal under current accounting rules.

This legal loop inflates tech company stock prices, forcing automatic retirement accounts and index funds to buy even more of these tech stocks. It is a self feeding loop where investments, sales, and stock prices all go up on paper without the AI technology ever making real cash profits.

Gran parte de lo que gráfica @danyscht se verifica en la Cuenca del Golfo San Jorge. Sobre esto y cómo se está abordando desde el territorio en https://t.co/tSybQpFziO

In a new major report, the World Bank conceded that its decades-long war on industrial policy was wrong, saying its old advice “has not aged well — it has the practical value of a floppy disk today.”

But this is not an intellectual awakening.

The World Bank's doctrine shifted because the means through which Western nations can maintain their dominance shifted — not because economists suddenly discovered new evidence.

The world’s wealthiest nations are now pursuing industrial policy so openly that it can no longer be denied to the rest of the world.

When the geopolitical winds shift, so does the ideology of institutions where wealthy nations' interests are deeply entrenched.

The person who built Claude Code just showed exactly how to use it.

30 minutes. Free. Straight from Boris Cherny himself.

Bookmark this before you forget.

Most people using Claude daily are missing 40+ features hiding in plain sight.

This single session is worth more than any $1000 course.

De hecho es al revés.

En promedio la IED fue mas alta con gobiernos "kirchneristas" que con los liberales.

Si sumamos "fusiones y adquisiciones" con Milei la IED da negativa.

Hacer ejercicios econométricos está bien. Pero justamente medir TFP es lo más flojo, lo menos no robusto en el menú. Y sacar estas conclusiones son su peor uso.👇

Donald Trump's green new deal

My latest column for @FT: The US president has inadvertently raised the appeal of renewable energy across the world: https://t.co/HotuPyh8Bz

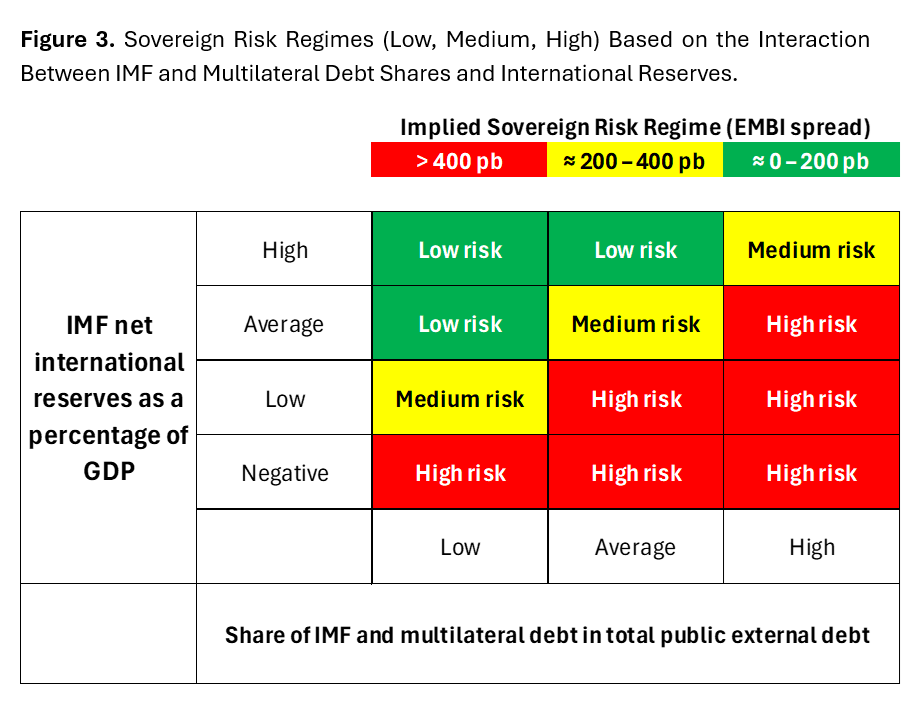

El FMI como freno que impide la baja del riesgo país

Ayer Carlos Pagni habló de esto en @lanacionmas Hace unos días, 1816 publicó un buen informe analizando la deuda senior y junior del país y también algunos medios y consultoras han tocado el tema.

Ni bien se firmó el Acuerdo con el @FMInoticias todo el mundo preveía una baja del riesgo país y el acceso al mercado financiero internacional.

De hecho, el propio Programa está basado en que la clave del financiamiento en los años siguientes sería justamente esa: la compresión del spread soberano de Argentina.

En ese momento, contra la opinión generalizada, creo haber sido el único que aquí y en @ElEconomista

sostuvo que aumentar en USD 20.000 millones la deuda senior generaba un alivio de corto plazo, pero un problema estructural en el mediano plazo.

Demasiada deuda privilegiada lleva a que los tenedores de deuda junior —como los bonistas— vean lógico cobrar una prima adicional por el riesgo de tener que afrontar una quita mayor a la esperada.

Abajo adjunto un artículo enviado a publicar titulado

"Too Much of a Good Thing? Why IMF and Other Official Lending May Raise Sovereign Risk Premia",

donde discutimos la hipótesis —que no es solo para Argentina— de que la relación entre deuda con el FMI (y otros acreedores senior) y riesgo país no es lineal.

Inicialmente, cuando el FMI entra desde cero como acreedor de un país, cumple un rol positivo desde la perspectiva de los bonistas: actúa como "vigilante" de la solvencia macroeconómica y como coordinador implícito de acreedores.

Eso, en principio, reduce la probabilidad percibida de default y comprime los spreads.

Pero ese efecto benéfico para los acreedores tiene un límite: el momento en que el FMI (y otros) son acreedores de una parte sustantiva de la deuda total.

Si aparecen problemas, todos saben que:

1) la deuda con el FMI y otros OI no se toca;

2) los bonistas deberán hacer todo el esfuerzo para afrontar el eventual ajuste;

3) entonces esa situación tiene un precio: más puntos en la prima de riesgo país.

La idea central es que cuando la participación del FMI —y de otros organismos multilaterales como el Banco Mundial, el BID o la CAF— pasa de ser marginal a ser significativa, aparece una externalidad negativa: la ultra-prioridad de cobro frente a cualquier evento de reestructuración.

Hagamos un ejemplo. Si comparamos dos países con iguales "fundamentals":

• En uno, el FMI tiene el 10% de la deuda externa pública.

• En el otro, tiene el 50%.

Ante una reestructuración que implique, por ejemplo, una quita del 20% del total:

• En el primer caso, la carga se distribuye sobre una base más amplia de acreedores privados.

• En el segundo, los bonistas absorben prácticamente todo el ajuste.

Eso implica, ex ante, un mayor riesgo para los bonistas

→ y, por lo tanto, un spread estructural más alto.

No es ilógico pensar que esa "subordinación implícita" agregue un lastre de 100 a 200 puntos básicos difícil de eliminar,

aun con buenos fundamentals.

👉 En otras palabras: el FMI baja el riesgo… hasta cierto punto. Más allá de ese punto, puede empezar a aumentarlo.

La forma de compensar este efecto es conocida:

• mayor acumulación de reservas,

• mejora en el ratio reservas / deuda con privados,

• mayor superávit fiscal.

Vale remarcar que este rol de acreedor privilegiado no es sólo una tradición del sistema monetario internacional.

Está explícitamente establecido en los Acuerdos que se firman con el FMI, donde además queda claramente estipulado -en el capítulo de sostenibilidad de la deuda- que, para hacer un Acuerdo con un país, el Fondo necesita que haya un “buffer” que le garantice dónde descargar eventuales reestructuraciones de deuda que no pudieran evitarse.

Para bajar el paper:

https://t.co/NjOdDV9GmS

#riesgopais #deuda #fmi #deudasenior

This is a fantastic new paper analysing the political economy of China's green transition.

It argues that the interplay between authoritarian centralisation, state-steering of capital, and long-term economic planning is a key reason China has become a clean energy powerhouse.

Todavía hay tiempo para inscribirse a esta Diplo super interesante, que aborda la transición energética desde distintas perspectivas en torno a la economía politica del desarrollo! Un placer participar con una clase sobre el sec nuclear!

Se viene la Escuela de Tópicos Avanzados de Economía Política, organizada por @DevEconNetwork y @idaesoficial, del 13 al 17 de julio en Buenos Aires.

Para estudiantes avanzadxs y graduadxs recientes de economía y carreras afines de América Latina 🌎

La trampa estructural que el petróleo a 109 dólares acaba de revelar

Argentina tiene Vaca Muerta. 860.000 barriles diarios. Superávit energético de USD 8.000 millones anuales.

Y sin embargo el Brent a 109 dólares la golpea igual que a un país sin una gota de petróleo.

¿Por qué?

Porque tener petróleo no es lo mismo que procesar petróleo.

Argentina exporta crudo y reimporta derivados. Tiene gas pero no fertilizantes. Tiene litio pero no baterías. Tiene soja pero no química industrial.

El shock energético transmite inflación por combustibles, logística y tarifas rezagadas —al mismo tiempo— sobre una industria con 40% de capacidad ociosa y PBI manufacturero en niveles de 1985.

La renta llega en dólares con rezago de meses. El costo inflacionario llega en pesos esta semana.

Eso no es mala suerte. Es el costo exacto de no tener política industrial durante dos años.

#Argentina #Petroleo #VacaMuerta #Inflacion #Industria

China crossed 50% (53.9%) penetration in EV heavy-duty truck sales — not cars, not buses, but heavy freight, the most brutally economic transport segment. 2025 sales hit 231,100 units (+182% YoY), with annual penetration at 28.9% vs 13.6% in 2024. #LFP#Lithium

That alone should stop people in their tracks. But the real story is hiding inside the batteries.

🚛 These aren’t car batteries — they’re grid assets on wheels

Typical battery sizes in China’s electric heavy truck fleet:

• Urban / short-haul: ~200–300 kWh

• Regional haul (most volume): 300–450 kWh

• Battery-swap trucks: ~280–320 kWh per standard pack

• Many trucks run 1–2 packs, route-dependent

• Mining / ports / extreme duty: 500–600+ kWh

That’s 5–8× a passenger EV battery, deployed into vehicles that:

• Run far higher daily utilisation

• Cycle batteries hard

• Prioritise durability, uptime & TCO

That’s why LFP dominates.

🔁 Battery swapping flipped the economics

China didn’t just electrify trucks — it industrialised them.

• Standardised packs across OEMs

• 5–10 min swaps

• Batteries owned by operators, not fleets

• Trucks sold cheaper, batteries monetised separately

Capex pain removed. Utilisation up. EV trucks win on pure economics — no ideology, no virtue signalling. Just math.

When fleets save ~RMB 1–1.2m per truck over 8–10 years vs diesel, the choice isn’t philosophical — it’s inevitable.

⚡ The lithium demand shock nobody is modelling properly

This is where it gets explosive.

One electric heavy truck =

• Multiple passenger EVs worth of lithium

• Deployed instantly

• Locked into domestic supply chains

• Bought on fleet cycles, not consumer whim

Unlike car sales, this demand is:

• Sticky

• Utilisation-heavy

• Infrastructure-coupled (swap stations, depots, hubs)

No smooth curve here. Step changes.

Passenger EVs drove lithium demand growth.

Heavy trucks drive lithium demand shocks.

🧨 Why 50% matters

Yes, December was front-loaded. Subsidies, tax timing. Fine. That explains timing, not direction.

You don’t “accidentally” hit 50% penetration in the most cost-sensitive transport segment on Earth.

Once fleets cross this line:

• Procurement logic flips

• Infrastructure locks in

• Resale markets form

• Diesel becomes the risky option

This isn’t a cycle. It’s a phase change.

🔮 The takeaway

If heavy trucks are tipping:

• Diesel demand destruction accelerates

• Battery demand compounds faster than car-centric models assume

• Lithium doesn’t drift — it reprices

This isn’t flashy.

It won’t trend on TikTok.

But it’s the moment electrification moves from transition to industrial inevitability.

Once heavy freight goes electric — there’s no way back.

https://t.co/sTaSSqYZyY

10/10

Stop worrying about the debt and start looking at the accounting.

Watch my full breakdown of why Ferguson is wrong here:

https://t.co/RaiRYVE7i4

#Economics#SteveKeen#ModernMoney