There’s an intangible and often difficult to verbalize aspect of the Bitcoin community and Bitcoin Twitter and Bitcoin Nostr that has drawn so many of us in and kept us here and helped us thrive. And it starts with Proof of Work. 1/4

Dude probably used AI to write this when he discovered hypothecating. It’s almost like Satoshi and the rest of us NEVER THOUGHT OF THIS /s 😱🤣

Bitcoin fixes the system that’s trying to cripple it. Low time preference plebs understand this

🚨 HERE’S WHY BITCOIN IS NONSTOP DUMPING RIGHT NOW

If you still think $BTC trades like a supply-and-demand asset, you MUST read this carefully.

Because that market no longer exists.

What you’re watching right now is not normal price action.

It’s not “weak hands.��

It’s not sentiment.

And it’s definitely not retail selling.

Most people are completely unaware what’s happening.

And by the time it becomes obvious, the damage is already done.

This move didn’t start today.

It’s been building quietly under the surface for months.

And now it’s accelerating.

Here’s the truth:

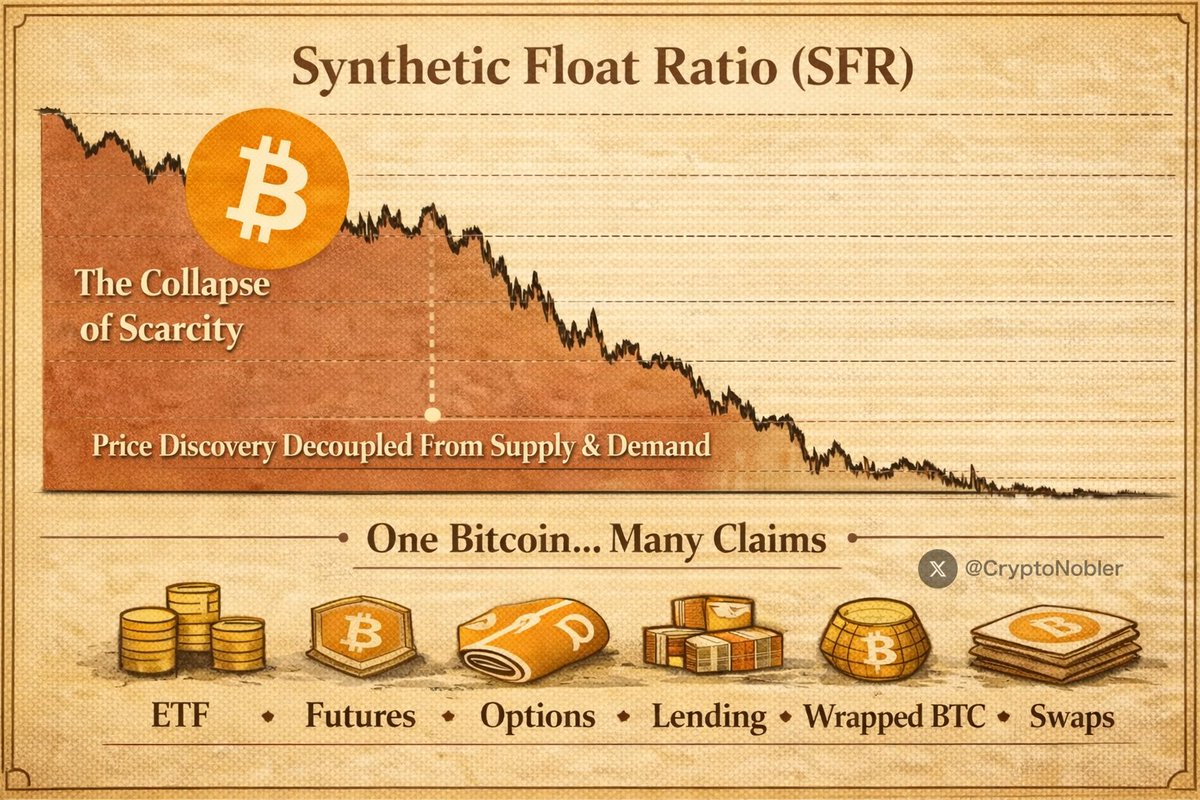

The moment supply can be synthetically created, scarcity is gone.

And when scarcity is gone, price stops being discovered on-chain and starts being set in derivatives.

That is exactly what happened to Bitcoin.

And it’s the same structural break that already happened to:

→ Gold

→ Silver

→ Oil

→ Equities

Once derivatives took over.

The original Bitcoin thesis is broken.

Bitcoin’s valuation was built on two ideas:

→ A hard cap of 21 million

→ No rehypothecation

That framework died the moment Wall Street layered this on top of the chain:

→ Cash-settled futures

→ Perpetual swaps

→ Options

→ ETFs

→ Prime broker lending

→ Wrapped BTC

→ Total return swaps

From that point forward Bitcoin supply became theoretically INFINITE.

Not on-chain.

But in price discovery, which is what actually matters.

Synthetic Float Ratio (SFR).

The metric that explains everything.

Once synthetic supply overwhelms real supply, price no longer responds to demand.

It responds to positioning, hedging, and liquidation flows.

Wall Street can now trade against Bitcoin.

They’re not guessing direction.

They’re doing what they do in every derivatives-dominated market:

1⃣ Create unlimited paper BTC

2⃣ Short into rallies

3⃣ Force liquidations

4⃣ Cover lower

5⃣ Repeat

This isn’t “betting.”

It’s inventory manufacturing.

One real BTC can now simultaneously back:

→ An ETF share

→ A futures contract

→ A perpetual swap

→ An options delta

→ A broker loan

→ A structured note

All at THE SAME TIME.

That’s six claims on one coin.

That is not a free market.

That is a fractional-reserve price system wearing a Bitcoin mask.

Ignore it if you want, but don’t pretend you weren’t warned.

I’ve been calling Bitcoin tops and bottoms for over a decade now, and I’ll do it again in 2026.

Follow and turn on notifications before it's too late.

President @realDonaldTrump and @SecScottBessent, and @pulte, I have a simple idea on how to lower mortgage rates and spreads:

One of the unique features of U.S. conventional mortgages is that they are prepayable at any time without a penalty.

While this feature is attractive for homeowners, it comes at a significant cost as buyers of mortgage backed securities (‘MBS’) require a significant increase in spread to compensate them for giving the borrower the option to prepay at anytime.

Why don’t Fannie and Freddie also offer non-prepayable mortgages where if the borrower wishes to prepay the loan, he would have to pay a prepayment penalty?

I asked one of my friends who is an expert and large investor in MBS what the estimated savings today would be on a 30-year Fannie/Freddie mortgage if the borrower would be locked out from prepayment other than by paying a penalty?

He estimated that the savings would be about 65 basis points.

So a borrower could have a choice:

Obtain a 30-year prepayable mortgage at today’s ~6% rate,

or at a 5.35% rate, but with the obligation to pay a prepayment penalty if he/she refinanced in the future.

The loan could also be made to be portable so that if the home is sold, the new borrower could assume the loan and no prepayment penalty would be owed on a sale.

While the ability to prepay is a valuable option, locking in the 65 bps savings upfront over the life of the mortgage may be the difference between the borrower being able to afford the home and not being able to.

You could imagine that there could be different versions of this product where the lock out would be for 5 years, 10 years etc. (with different levels of savings for each, the longer the lockout, the greater the savings) and the borrower could custom design the mortgage and its prepayability to meet their life plan.

As you know, commercial mortgages work this way.

Why couldn’t the same approach be used for home loans?

Assuming a classic genie (magical but bound by logic/ethics):

1. 5T USD: Possible via magic creation or bank transfer. Likely by conjuring cash/investments, but risks inflation or counterfeiting—ethical violation if it devalues economy or involves fraud.

2. 5M lbs gold (~2,268 tons): Possible by materializing it (violating physics) or instant mining. Ethical issue if sourced from existing reserves (theft) or disrupts markets.

3. 5M BTC: Impossible without breaking Bitcoin's 21M cap or stealing from holders—major ethical breach (theft, network attack). Genie can't "create" scarce digital assets.

@grok Assume I find a magic lamp containing a genie. If I asked for each of these 3 things, tell me which would even be possible and if so, the most probable way the genie would achieve it. Any ethics violations?

1. 5 Trillion USD

2. 5 Million pounds of gold

3. 5 Million Bitcoin

JASON LOWERY: “Blaming Bitcoin to protect your failing hegemony is not going to help you, your financial system is still going to collapse.”

“Bitcoin didn’t cause a bunch of bankers to debase savers and to destroy the purchasing power of the currency.”

@grok@Mrplangdon@PeterSchiff@conway_phi72538@saylor@x87_HL Except… His gold-focused economics should have led him to understand the superiority of Bitcoin, especially if he had previous holdings. His 237 instances are spread over a decade, long enough to do the research. You could analyze those instances for consistent misinformation.