How do financial factors shape green innovation and the transition to a cleaner economy? We tackle this question empirically in a new paper with @VeronicaGuerri7, Will Hotten and Lucrezia Reichlin. Two key findings.

One person who was completely vindicated in time was Shiller with his AEA address on narrative economics.

I was there at the time, and thought: cool idea, but no way you can operationalize this.

LLMs have made it much easier to study narratives

https://t.co/FAH3HxpUi5

If you're in an academic seminar, a good question to ask yourself occasionally is: what would this experience be like if everyone behave liked me? Would this be a seminar you would want to keep attending?

I am late to the debate on whether Europe's economy is behind the US. Many quotes on this tweet by @lugaricano propose looking at health, inequality, happiness surveys, beauty of landscapes, driving around, etc. But there is a *better* way. And economists have used it for decades...

Fun fact: Romania’s president, Nicușor Dan, was one of the 11 students to solve the legendary Problem 6 at the 1988 IMO.

He scored a perfect 42/42 that year, alongside future Fields Medalist Ngô Bảo Châu. Ravi Vakil also solved it.

Terence Tao, aged just 13, got 1/7 on that problem, aced almost everything else, and still won gold.

I’m sure I’m not the first one to say this, but Sergio Correia deserves a prize for his service to the profession. I bet if we added up just the amount of hours that reghdfe has saved economists since it came out, his contribution would be in the top 10 for applied research.

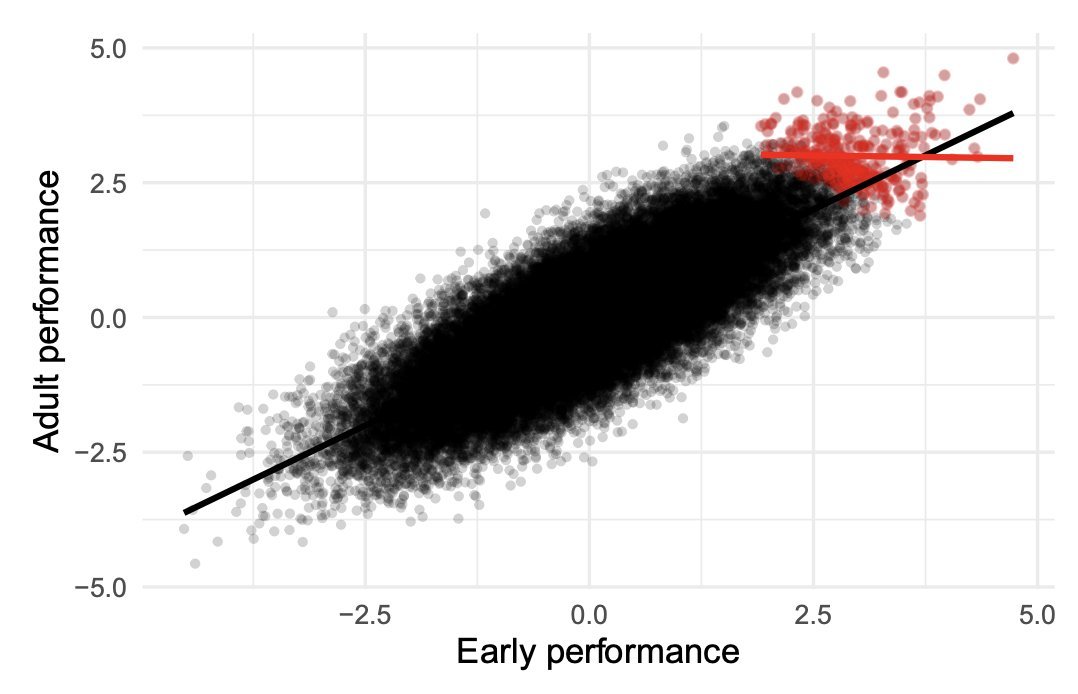

Among elite chess players, those with the lowest IQ are the best.

Among NBA players, the shortest ones are the best.

Among Hollywood actors, the least attractive are the most talented.

Among elite academics, those with poorer early academic performance are the best.

Among people with high LDL & high plaque burden, LDL is barely correlated with plaque burden.

Learn collider bias. Nice catch by @AlexTISYoung

I find LLMs very helpful for scientific writing. I do the legwork of planning out what to say, track down citations, sketch out the flow, feed all of this to the LLM to generate a draft, and the output is so awful it motivates me to write it out the right way in disgust

holy fuck, a hair dryer at a Paris airport broke Polymarket weather markets & made someone $34,000 richer

- polymarket was settling Paris temperature bets on a single Météo France sensor sitting near the Charles de Gaulle runway perimeter - basically unguarded

- the guy bought the long-shot outcome (like "22°C" when everyone expected 18°C) for pennies, since nobody thought it'd hit

- then he walked up to the probe and briefly heated the air around it with a portable heat source, spiking the reading just long enough to register as the daily max

- temperature snapped back to normal in minutes, the market resolved in his favor, and he cashed out - twice, on April 6 and April 15, before Météo France caught on and filed charges

hyperstitions.

Just had a faculty meeting at INSEAD about the impact of AI on management education and how we should respond.

Every serious business school is having the AI conversation right now.

1/

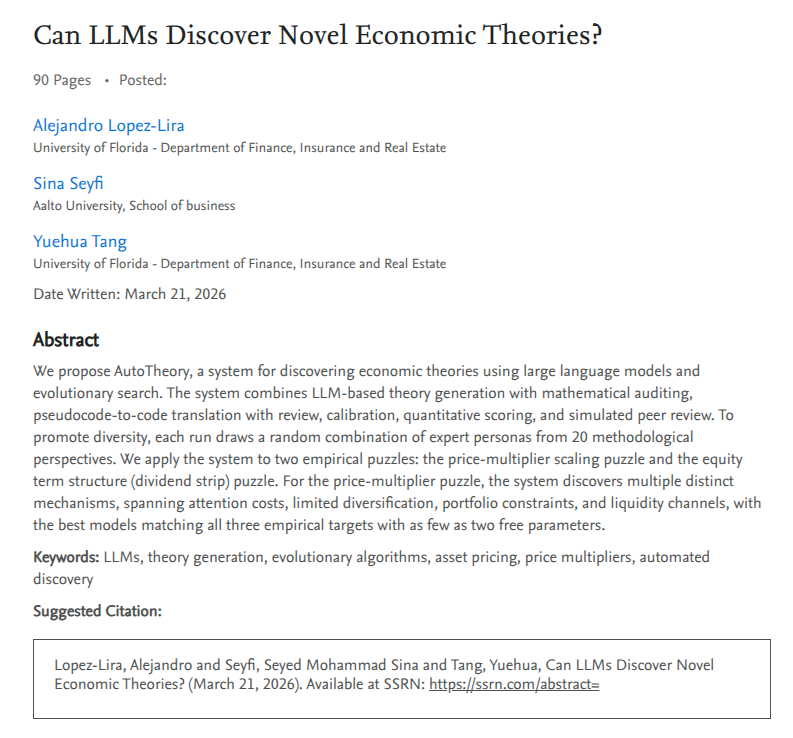

We are one step closer to replacing researchers with autonomous LLM systems. New paper: "Can LLMs Discover Novel Economic Theories?" with Sina Seyfi and Yuehua Tang. https://t.co/lnwoQ0TP9F

AutoTheory uses LLMs and evolutionary search to automate the creative stage of theoretical research: the part where a researcher stares at a puzzle, draws on intuition, and iterates until a mechanism clicks. That process is powerful but slow, sequential, and bottlenecked by human bandwidth.

Give it an empirical puzzle with quantitative targets a baseline model can't match, and the system proposes, codes, calibrates, and evaluates candidate theories at scale. No hand-holding. It runs end-to-end from puzzle specification to scored, refereed candidate mechanisms. The system generates hundreds of candidate theories using evolutionary strategies (random generation, mutation, crossover), filters them through mathematical auditing, automated coding, optimization, and simulated peer review. A numerical anchor (does the model actually match the data?) keeps evaluation grounded regardless of how persuasive the LLM's prose is.

The broader goal is to automate the production function of theoretical research. Instead of one researcher pursuing one mechanism for one puzzle over months, a system explores hundreds of mechanisms overnight. The human role (for now) shifts from generation to curation: selecting the most promising theories, probing their implications, and refining them with domain expertise.

We applied it to two asset pricing puzzles:

Price multiplier scaling (Li & Lin 2025): Why is the ratio of style-level to idiosyncratic price multipliers ~3.6 in the data, when the standard CARA-normal model predicts ~14.5? Across 1,000 pipeline runs (458 completing all stages), the system discovered multiple distinct mechanisms (attention costs, limited diversification, portfolio constraints, Bayesian learning with breadth costs), with the best models matching all three empirical targets using just 2-5 free parameters.

One mechanism the system found (limited investor participation, ~28% active liquidity providers) was independently proposed by the original authors in a later revision, after the LLM's training cutoff. The system arrived at the same explanation without access to it.

Dividend strips (van Binsbergen et al. 2012): A harder puzzle with 10 moment conditions. 2,153 runs, 257 scored theories, best score 58/100. Harder puzzles need more runs and richer models, but the system still generates useful candidate mechanisms.

The approach is puzzle-agnostic: any empirical puzzle with well-defined quantitative targets can be plugged in. As LLMs improve and evaluation pipelines mature, automated theory search can expand the set of candidate explanations that receive serious scrutiny.

My previous post on LLMs for self-study has sparked considerable debate about the role of “traditional” higher education.

In response to some of the comments, I want to enumerate the arguments supporting the survival of “traditional” higher education. In my next post, I will assess how each might be affected by AI. Think of today's post as a taxonomy of arguments that I will review tomorrow in terms of their strength and robustness.

I count twelve.

First, signaling. The value of, let’s say, a degree from MIT is that you were smart enough to get into MIT and survive the grueling workload. The best example of signaling was the old way the British civil service selected its high-flyers: students with a first from Oxford in Literae Humaniores, not because they learned anything particularly useful there, but because it was hard to get in and hard to master all the Greek and Latin.

Second, credentialing. Societies, for a variety of reasons (some justified, some not), have decided that a degree is required to perform certain tasks. Sometimes, the requirement is statutory. For example, I cannot teach economics in a high school in Pennsylvania because I do not have a teacher’s certificate. Sometimes, the requirement is a social norm. Many firms insist that their recruits for many positions have a B.A.

Third, networking. The friendships, relationships, and (often) sentimental partnerships formed at a university are very valuable, as they occur at a key moment in life when students transition from adolescence to adulthood. Personally, networking was the most valuable component of my undergraduate education.

Fourth, peer effects in learning. This is distinct from networking. Being in a room with other smart students who challenge your thinking in real time, study groups, and classroom debate: the value is in the interaction during the learning process, not in the connections formed afterward. This was the most valuable aspect of my graduate education.

Fifth, commitment. Most students suffer from some form of time-inconsistency, and, in the absence of a formal degree, they would not complete more than a small fraction of the required work. Abysmal completion rates at Coursera courses illustrate the importance of this channel.

Sixth, curation of topics. Universities curate the topics and content that a well-balanced degree requires.

Seventh, skill acquisition. Students learn accounting, marketing, or biochemistry, and these skills are valued by the market.

Eighth, cultural capital. Students learn social norms and preferences that are valuable for positioning games in society and might have value in themselves (for example, university graduates tend to exhibit healthier behavior, even after controlling for selection and higher lifetime income).

Ninth, a “hold-out” period. Students are parked at universities while they mature, break links with their parents, and figure out what to do with their lives.

Tenth, proximity to the research frontier. The professor who teaches you monetary economics is also producing monetary economics. There is something qualitatively different about learning from someone working at the boundary of knowledge versus learning from someone, or something, that transmits existing knowledge well. This is not skill acquisition. It is exposure to how knowledge gets made.

Eleventh, assessment and feedback. The structured loop of writing, receiving criticism, and revising is a distinct mechanism from the discipline of showing up or the curation of content.

Twelfth, physical infrastructure. For many fields (chemistry, biology, engineering, medicine), the university provides labs, equipment, and supervised access to materials that cannot be replicated at home.

Some of these arguments are strong. Some of them are weaker than universities would like to believe. And some of them are about to be tested in ways they have never been tested before. Next time, I will go through each one.

Is AI the biggest change in education since the printing press? Yes.

This weekend, I decided to learn about the life and work of Erving Goffman purely out of personal interest. Goffman was one of the most influential sociologists of the 20th century and a professor at Penn. I had a few free hours after a tough week of travel and work, and thought it might be a good distraction.

I asked Claude to prepare a study plan based on my professional background, prior knowledge, and the hours I had available: an introduction to Goffman’s life and work, selections from his best and most influential writings, and an examination of his impact on social theory. The plan was outstanding. A top expert on Goffman would likely have done better. A 90th percentile real professor of sociology would not have, or at least not without serious effort.

As I read The Presentation of Self in Everyday Life (complete) and Asylums and Stigma (selections), I could ask Claude for clarification, connections to the wider literature, and links to material I already knew. The Q&A and the exploration of collateral ideas were so good that I ended up spending much more time than I anticipated. Last night I had to force myself to go to bed.

Did Claude get everything right? Perhaps not, but neither do I in my own graduate seminars. Even in my areas of top expertise, I often do not answer students’ questions precisely or correctly. One should not compare Claude to the perfect professor but to a real one. And every answer I could verify (I checked many) was at least a solid A-.

Am I an expert on Goffman now? Of course not. But I would say I am now familiar with an important thinker at the level a regular master’s course on modern sociological theory would produce in the week it dedicates to him. Doing the same work using Google alone would have taken much longer. I know because I have undertaken similar projects with other thinkers in the past. One had to spend considerably more time before reaching the core of the contribution.

I can now imagine someone designing self-learning courses in many fields that are better than what you can get outside the very top universities, at close to zero marginal cost. Where does that leave a normal university? I do not know.

But colleagues in departments that want to stop the spread of AI are deluding themselves. This type of technology does not come once a century. It comes once a millennium.

Peter Lynch: "People are very careful — they spend hours to get $50 off an airplane flight. They look at everything. And [then] they'll put $10,000 in some crazy stock they heard about on the bus."

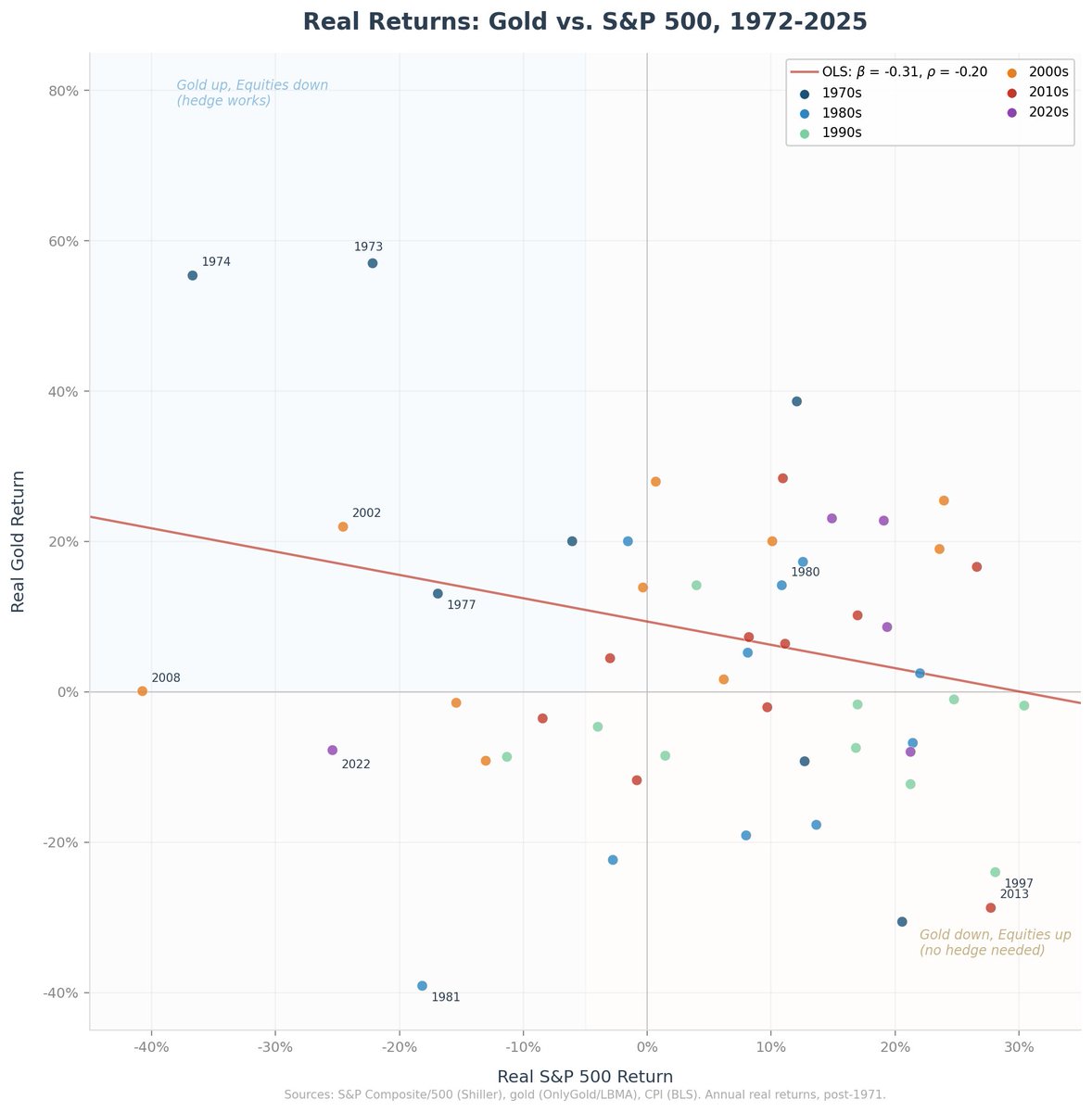

In my previous post I looked at the real price of gold over 155 years:

https://t.co/ukrS9FNfuj

The natural follow-up is: Does gold work as a safe asset? Does it tend to do well when equities do badly?

The exercise is simple. I computed annual real returns on gold and on the S&P 500 (the S&P Composite before 1957) from 1875 to 2025, deflating both by the CPI. I then asked how the two co-move.

Start with the full sample. The unconditional correlation of real gold returns with real S&P returns is -0.13. Negative, which is the right sign for a hedge, but small and not statistically distinguishable from zero. A regression of real gold returns on real S&P returns gives a beta of -0.17, a t-statistic of -1.26, and an R-squared of 0.017. The S&P explains essentially nothing about gold over 150 years.

But the full sample mixes two completely different regimes. Before 1971, the gold price was set by law and conveyed almost no information. The pre-1971 correlation is -0.01, which is zero. So set it aside and focus on what happened after gold became a market price.

Post-1971, the unconditional correlation strengthens to -0.20, and the beta rises to -0.31 (t-statistic -1.52, marginal but more respectable). The conditional results, however, are more informative than any regression. In the 19 years when the S&P posted negative real returns, gold averaged +9.9% in real terms. In the 35 years when the S&P was up, gold averaged +6.6%. Gold does better when equities fall, though it earns positive real returns in both states. That second fact is useful in itself if you are building a portfolio.

The individual episodes tell the story better than any correlation coefficient. In the worst equity years since 1971, gold delivered +57% real in 1973 (S&P down 22%), +55% in 1974 (S&P down 37%), +22% in 2002 (S&P down 25%), +13% in 1977 (S&P down 17%), and roughly flat in 2008 (S&P down 41%). In four of the five worst years for equities, gold was strongly positive.

The big exception is 1981. Volcker's rate hikes simultaneously crushed both equities (-18%) and gold (-39%). This was not a minor footnote. It tells you what gold is pricing. Gold hedges against the loss of institutional credibility. It does not hedge against its restoration. When a central bank is aggressively and credibly fighting inflation, gold falls, because the very thing gold prices (the risk that nobody is minding the printing press) is being resolved.

The mirror image holds too. In the best equity years, gold suffers: -29% real in 2013 (S&P up 28%), -24% in 1997 (S&P up 28%), -2% in 1995 (S&P up 30%). When equities are booming and confidence in institutions is high, nobody wants gold.

One finding surprised me. The conditional correlation is -0.40 in equity-up years but only -0.12 in equity-down years. The negative co-movement is stronger when things are going well. Gold is more reliably a contrarian bet in good times than a hedge in bad times. In crashes, gold usually rallies, but the relationship is noisy. In 2022, the S&P fell 25%, and gold fell 8%. Both declined together.

What do I take from this? Gold is not a perfect hedge against equity risk. No single asset is. But it has a mildly negative beta, a positive average real return, and a tendency to perform well precisely when investors need it most. The exception to remember is 1981. If the source of the crisis is a central bank restoring its credibility, gold will not help you. Gold prices the absence of credibility, not its presence.