One of my unpopular/hot takes is that Crypto is going to have another massive rally at some point.

A lot of the gamification, anti-fiat, and "escaping the permanent underclass" rationale will resurface at some point.

Just zero immediate catalyst given where rates are & the attention towards other things.

The Iranian navy, which has been destroyed eight times, has apparently closed the Strait of Hormuz again, because the United States, for the seventh time, won the war that wasn’t a war, so now the United States has to open the Strait of Hormuz that was already open before the not-war began.

The not-war began because Iran had uranium that was totally, completely, beautifully obliterated, so they can’t build the nuclear bomb they weren’t building, which is why the United States had to start the not-war it definitely didn’t start.

Now the United States, which has nuclear weapons, is threatening to use nuclear weapons to stop Iran from getting nuclear weapons, because nuclear weapons are far too dangerous for countries with nuclear weapons to allow other countries to have.

If the United States saw the United States doing what the United States does in other countries, the United States would invade the United States to liberate the United States from the tyranny of the United States.

The economy is heating up.

Chicago PMI last week was largest increase I've ever seen, except for COVID rebound. Inflation is going to be MUCH higher than expected because of a huge increase to diesel fuel costs. The underlying reason is the enormous fiscal deficit and the very easy monetary policy. We're going to see an inflationary boom. And that's going to hit the bond market like a bomb.

Let's say we get 6% inflation for 2026 and 4% GDP growth. That would put 10-year yield well over 7%.

That earnings yield gets you to ~15x multiple on the S&P 500. Here's what look like, at 15x earnings, for these stocks:

CompanyP/E Price15x Decline

Arm 445 $382$12 -97%

Tesla 232 $419$27 -94%

AMD 170 $514$45 -91%

Palantir162 $142$13 -91%

ServNow74 $123$25 -80%

Broadcom69 $412$89 -78%

TI 52 $305$87 -71%

Costco 50 $984$298 -70%

Lilly 40 $1,127$422 -63%

Nvidia 33 $214$97 -54%

Visa 28 $322$171 -47%

Amazon 31 $254$123 -51%

Visa 28 $322$171 -47%

M.C. 28 $484$259 -47%

Netflix 27 $82$46 -44%

And before you say that could never happen, this is exactly what happened between the end of '72 and the beginning of '75.

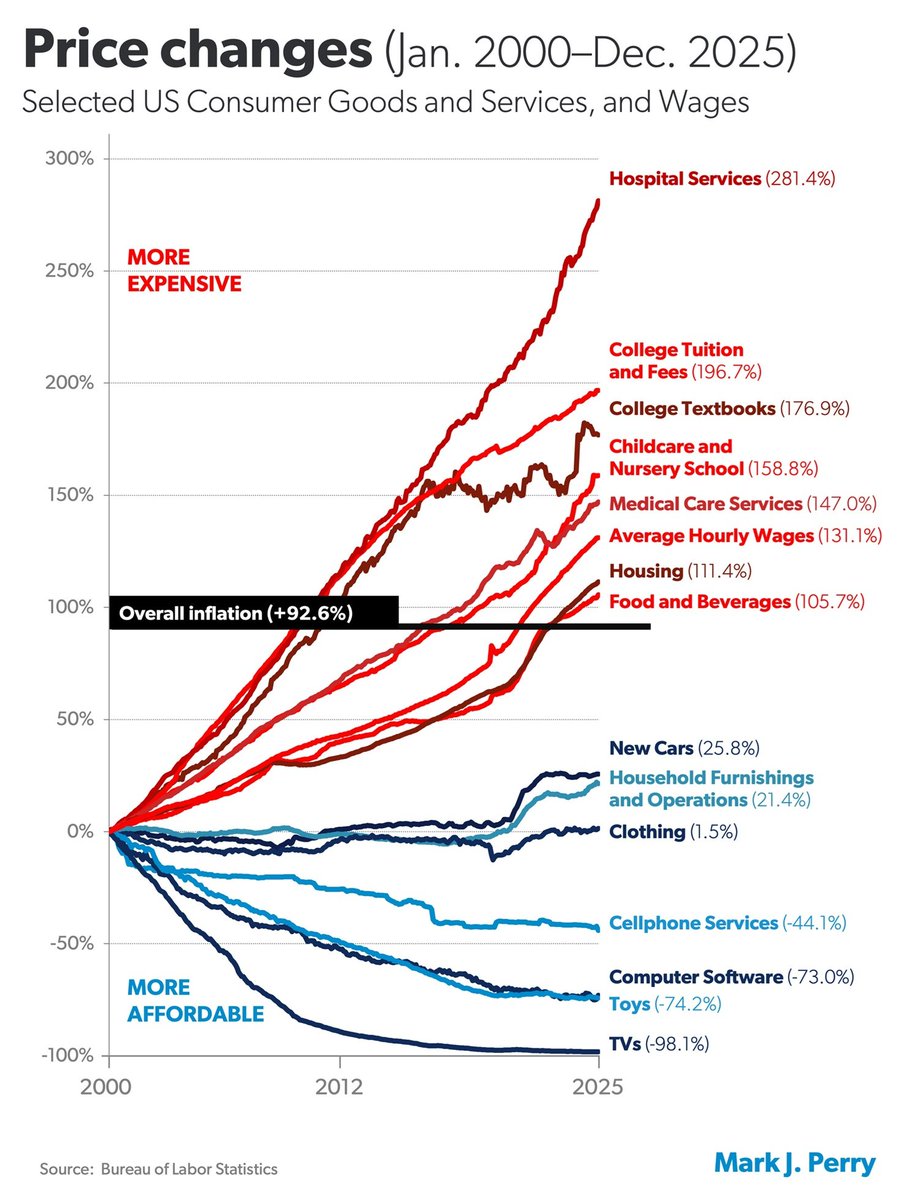

See what happens when the government gets involved and subsidizes the businesses most critical to human life?

The more government subsidy, the faster prices rise.

Hospital services, college tuition, childcare — all heavily subsidized, all up 150%+.

The inflation story in one chart:

Where government spending and subsidies are highest, prices rise the fastest.

Where competition is highest, prices fall.

Meanwhile the categories exposed to real competition and price discovery (electronics, software, apparel) have deflated.

When you subsidize demand without expanding supply, you get exactly this. When you insulate buyers from prices, providers have no incentive to compete on cost

Food for thought.

Wall Street still thinks AI is a productivity story. It just became a fragility and trust story, and that shift ties Anthropic’s Mythos, the Clarity Act, and Bitcoin together in a way investors are badly underpricing.

Anthropic’s Mythos model did more than showcase clever capabilities. It forced policymakers to acknowledge, in public, that the core software of the financial system is now one well‑aimed AI exploit away from systemic risk. When Scott Bessent and Jerome Powell are in emergency meetings with the heads of Wall Street banks to discuss AI‑driven cyber threats, the conversation has moved beyond sandbox innovation and into the realm of financial stability. The implicit message is clear: the incumbent architecture is not built for an adversarial, model‑driven world.

Bessent’s op‑ed arguing that the Clarity Act must pass as a matter of national security is the political counterpart of that realization. If AI can pierce legacy rails, then the United States needs clear, durable rules for digital assets and blockchain infrastructure, not so it can speculate on tokens, but so it can deliberately integrate cryptographic, verifiable, tamper‑resistant rails into the heart of its financial system. Clarity on custody, stablecoins, and blockchain‑based settlement is no longer a regulatory luxury; it is a defence priority.

Put together, Mythos, the Bessent–Powell Wall Street meetings, and the Clarity Act op‑ed point in the same direction: the centre of gravity is shifting from “AI will boost earnings” to “AI will test the integrity of our money pipes.” In that world, open, auditable, cryptographic infrastructure stops being a fringe experiment and starts looking like the logical upgrade path. Public blockchains, and Bitcoin in particular, offer precisely the properties an AI‑exposed system now needs: transparent rules, global replication, adversarial testing at scale, and settlement that does not depend on a single compromised database or trusted intermediary.

The connection investors are missing is that the AI shock and the regulatory turn are not separate stories. Mythos revealed how fragile the old code base is; Bessent’s call to pass the Clarity Act is an attempt to give the US a legal framework to adopt stronger, blockchain‑based rails; and the emergency meetings between Fed, Treasury, and Wall Street are the first visible signs that the establishment knows it cannot patch its way through this era with 1980s technology. When AI flips from a productivity narrative to a fragility and trust narrative, Bitcoin and blockchains stop competing with Wall Street, and start becoming the architecture Wall Street is forced to build on.

The Fed is asking banks how much private credit risk they're carrying

Translation: they don't know.

$1.8 trillion industry. Redemptions spiking. Troubled loans rising. Banks leveraging up the funds that are leveraging up the borrowers. big turn of the credit cycle incoming

Bloomberg on the Fed responding to private credit news:

"The Federal Reserve is asking major US banks for details about their exposure to private credit following a surge in redemptions from the funds and a rise in troubled loans in the industry, according to people with knowledge of the matter.

The queries by Fed examiners are intended to assess the level of stress in the private credit industry and the potential for it to spill over to the wider financial system, said the people, requesting anonymity to discuss the work."

#economy #markets #privatecredit

Let's walk through this together.

Every 10% rise in diesel adds 1.5% to consumer prices within a quarter.

New York Harbor ultra‑low‑sulfur diesel usually trades somewhere in the $2.25 to $3.25 per gallon range. On March 2nd it was $3.18. On March 20, the price hit $4.71 (+48%).

If you own a trucking fleet, your single largest operating cost just went vertical. The only time prices have ever been higher was at the beginning of the Russian-Ukraine war. The price hit $5.33 on May 11, 2022. You might recall what happened to inflation, interest rates, the bond market and the stock market that year.

Europe has its own benchmark called ICE Low Sulphur Gasoil. In calm times it trades between $600 and $900 per metric ton. Today, it’s trading over those previous records around $1,400 -- the highest price ever. Asia is telling the same story. Singapore’s 10‑ppm (parts per million) gasoil, the key reference price for diesel in the Pacific basin, is trading at an all-time high near $200 per barrel, up from $90 pre-Iran-war.

The “crack spread” is the margin a refinery earns for turning crude into diesel. Think of it as the toll the market pays per barrel to get crude oil converted into usable fuel. Normally the crack spread is $15 to $20 per barrel – not a major factor in energy cost. During the worst of the Russia‑Ukraine shock, diesel cracks rose above $50 per barrel. Today, the crack spread is over $70 per barrel.

While it only produces 20% of global crude supplies, the Persian Gulf effectively accounts for more than a third of global diesel supply because its sour crude is the key feedstock for the world's most efficient (and largest) refineries. Additionally, Persian Gulf refining capacity has grown from roughly 8 to about 13 million b/d over the past two decades, with new, highly complex export refineries (Al‑Zour, Jazan, Ruwais, Duqm) designed to run heavy/sour crude and maximize diesel yields.

With the Gulf closed, you are effectively removing about a third of the world's flexible export diesel that supplies Europe, Africa, and Asia.

If the Straight of Hormuz is closed for a year, you'll see diesel trading over $300 per barrel -- roughly 3x its current price. That pushes CPI over 30%. In a year.

You say this is impossible? It's exactly what is happening right now. Pakistan -- a nation of 250 million people and nuclear power -- is eight days from running out of diesel.

So, where would interest rates go if the CPI was 10%+ and there’s ongoing war in the Middle East?

In that scenario, I do not believe the existing federal debt can be financed without a technical default.

One-third of all of the outstanding debt held by the public ($10 trillion) must be refinanced by the end of 2026.

The weighted average coupon on this maturing debt is about 2.5%. If it has to be rolled at 8-10%, the incremental interest cost is roughly $500-700 billion per year, on top of the already-$1+ trillion interest bill.

Each 100 bps (1% higher rate) adds ~$310 billion annually in interest expense. At 10% across-the-board rates, you're looking at net interest expense approaching $2-2.5 trillion per year. Not "some day." Within 12-18 months.

Current federal revenues are $5.6 trillion. If interest alone hits $2+ trillion within 12 months, that's roughly 40% of the budget going to debt service — just the interest!

I believe it’s inevitable that the U.S. will default – just as it did in 1933 and in 1971. The only question is when and what will trigger the panic.

Soaring diesel prices, an ongoing war in Iran, and rates soaring over 10% would do it.

So, for me, if the 10-year cracks 5%... I’m out. The markets will no longer be investable.

Thank you for your attention to this matter.

BREAKING: Iran's Foreign Minister Araghchi says Israel has struck "2 of Iran's largest steel factories, a power plant, and civilian nuclear sites in coordination with the US."

Araghchi says this "contradicts" President Trump's 10-day pause of strikes on Iranian power plants.

"Iran will exact a heavy price," he says.

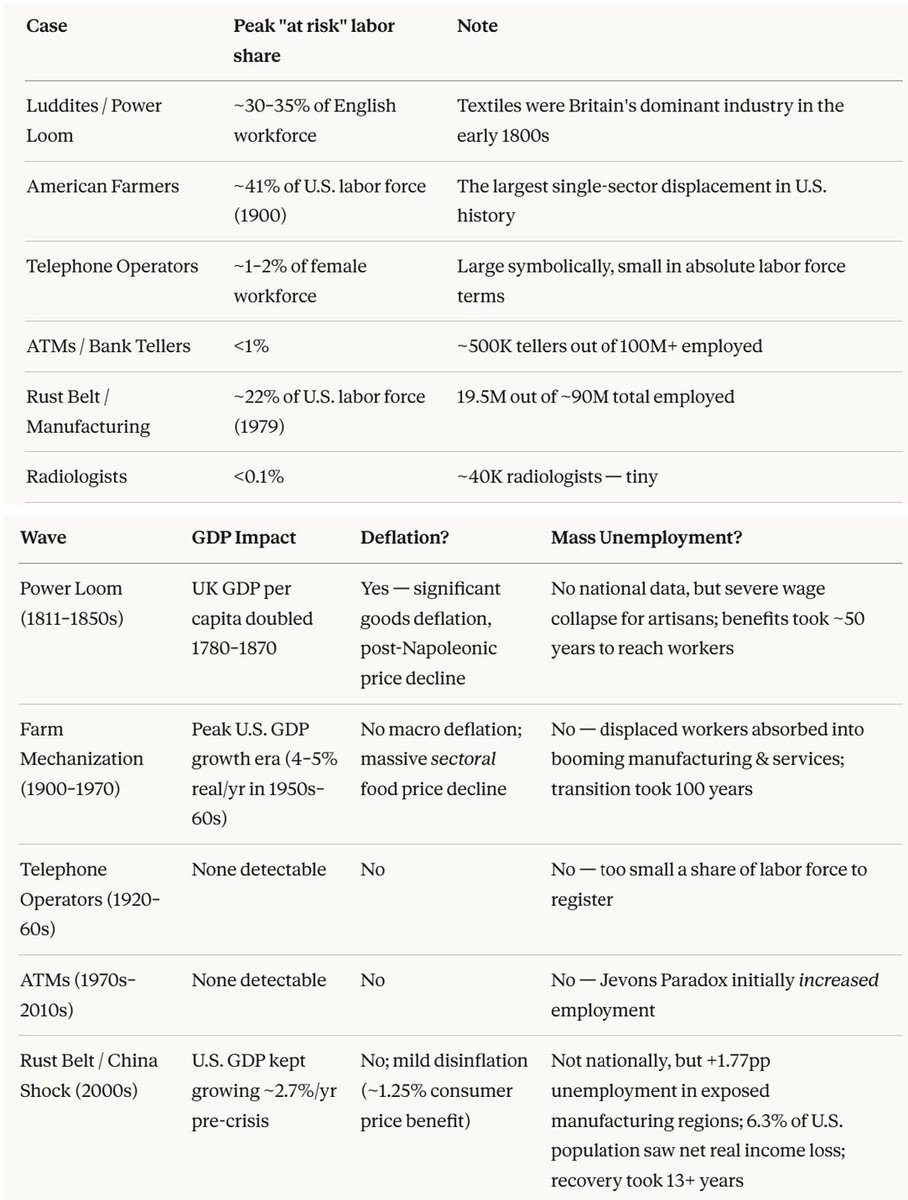

Heard $Druckenmiller on a podcast: "Anybody who believes that(i.e. AI will be very deflationary and it will lead to massive job losses) with conviction suffers from arrogance and not an open mind…every technological revolution since was known to man, it’s been declared, for jobs it’s the end of the world…So let’s say the pessimists are right on AI, it’s possible you get a government response with printing and universal income."

That got me intrigued, so I asked $Claude and $GPT to go back through history and review a few cases where societies feared that new technologies or structural shifts would trigger permanent mass unemployment:

The Luddites (1811-1850s); American farmers (1800s-1970s); Telephone operators (1920s-1960s); ATMs and bank tellers (1970s-2010s); The Rust Belt (1980s-present); Radiologists and AI (2016-present).

Full case study: https://t.co/So3zbjs1tc

In none of these cases did we get sustained, economy-wide deflation or permanent mass unemployment.

---

What actually feels different this time?

Speed. The shift from 41% to 2% of the labor force in agriculture took roughly a century. Telephone operators faded over about 60 years. ATMs played out over roughly 40 years. Even Rust Belt deindustrialization - often seen as shockingly fast - unfolded over 20-30 years. AI could move much faster.

---

What happens if AI really does cause deflation or unemployment?

The Fed has four main anti-deflation tools:

- Cut interest rates

- QE

- Forward guidance

- Coordinate with fiscal stimulus - the 2020 playbook

These tools can support aggregate demand. What they cannot do well is determine who benefits.

The most likely macro outcome may look something like a Rust Belt at scale: nationally, GDP still grows, unemployment stays moderate, and headline deflation never really shows up. But underneath those aggregates, inequality widens and pain gets concentrated.

---

If $Dario is directionally right - say 50% of entry-level white-collar jobs disappear within 1-5 years - the math gets meaningful quickly:

- Current unemployed = 168M x 4% = 6.7M

- 50% of entry-level white-collar jobs displaced = 5M-7.5M

- Unemployment could rise toward roughly 7-9%

- Historically, U.S. unemployment has usually ranged between roughly 4% and 10% outside extreme crises. A move from 4% to 7-9% would not be unprecedented - but it would be large enough to reshape politics, wages, and social expectations.

---

Long way of saying: I’m trying not to be “arrogant without an open mind.”

As $Druckenmiller said: "you just have to always be looking at what other people might not be, and then if you’re prepared for it mentally, you can adjust quickly enough, um, in your portfolio to it as it unrolls."

+++

Full analysis: https://t.co/So3zbjs1tc

We all knew this was coming… but today I heard about it actually happening.

A seed stage company backed by a well known VC openly admitted (in a board deck) that their strategy is to get access to a large incumbent’s software from a customer, clone the entire thing using Claude Code, and offer it at 90% less.

Not “build something better.” Just copy it and offer it for less.

The VC endorsed this as the GTM strategy. And even wrote back in writing that it was a good idea.

Using a customer’s licensed access to reverse engineer a product and clone it is ethically bankrupt. I don’t know how else to put it.

It likely violates terms of service. It may violate trade secret law as well (but I’m certainly not a lawyer).

And a reputable VC putting this in writing in a board deck is genuinely insane.

But it’s going to happen anyway.

Everywhere… all the time.

I don’t know where this ends, but we all knew this was coming and now it’s here.