Morgan Stanley is launching its own Bitcoin ETF today -- MSBT --becoming the first major Wall Street bank to do so. It’ll also be the cheapest in the cohort. Late to the game, but leaning on a classic playbook: win on fees and scale.

https://t.co/ZWNj2S7vD6…

Working from home leads to more shopping at higher prices. One mechanism seems to be that WFH shifts shopping more to men, who shop faster and are less price sensitive, from Scott R. Baker, @I_Am_NickBloom, Stephanie G. Johnson, and Jana Obradović https://t.co/MsmbbRjOt5

@SpencerJCox My @BYUMarriott colleague Mark Johnson and I would love to sit down and talk with you about our research examining the financial harms of legalizing online sports betting. See our paper at https://t.co/1aYRIkVLao. I think our work would be helpful background for you.

Rebranding betting as a financial product doesn’t reduce the harm it causes, especially for young men.

We’re ready to defend our laws in court and protect Utahns from companies that drive addiction, isolation, and serious financial harm.

More here: https://t.co/3Ge0pdRJ61

🔗: https://t.co/diwPrMa3RP

Debate about the political independence of the Federal Reserve, highlighted over the past year in large part by President Donald Trump’s haranguing of the U.S. central bank over interest rate policy, continued this week after the president named Kevin Warsh as his choice to succeed current Fed chairman Jerome Powell.

Today’s debate over the design and purpose of the Federal Reserve mirrors, in many ways, challenges that arose amid conditions wrought by the Great Depression, namely, can the Fed act in the long-term economic interest of the nation if its decisions are subject to political pressure?

That was certainly on the mind of Utah Banker Marriner Eccles as he assumed the helm of the Fed in 1934, a time that found the U.S. central bank in a sorry state of fragmentation and weakened by its undue deference to the U.S. Treasury Department. Eccles is widely credited with establishing the modern-day version of the U.S. central bank.

In a Deseret News interview, @BYUMarriott professor and former Federal Reserve economist @JasonKotter explained why keeping politics out of monetary policy is crucial for the country’s economic stability and how important a role Eccles played in establishing the central bank’s independence.

Read more about the Federal Reserve, Eccles and the interview with Kotter at the link above.

✏️: @DNTechHive, Deseret News

I recently interviewed with @Deseret to discuss why the independence of the Federal Reserve is important. Check out the article at https://t.co/Y6Wk1OQD8O. Economists disagree about lots of things, but we are pretty much united in the view that Fed independence is crucial.

New paper on bank runs with Correia and Luck:

"Bank Runs With and Without Bank Failure"

Questions:

- What are the determinants of runs?

- When do bank runs result in bank failure?

- Can runs trigger the failure of healthy banks and amplify small shocks into large crises?

- Are runs themselves the initial cause of financial distress or are they a symptom of deeper fundamental solvency problems in the financial system?

What we do:

- Apply LLMs to historical newspapers to uncover over 4,000 runs on individual banks in the pre-FDIC US banking system from 1863 to 1934. Capture the most famous runs (Bank of the US

- Merge data on runs and other bank-level events discussed in newspapers (suspensions, failures) to bank-level fundamentals (harder than it sounds!)

What we find:

(1) Runs are considerably more likely in weak banks, but can also occur in strong banks, especially in response to negative news about the real economy or the broader banking system.

(2) However, runs typically only result in failure for banks with weak fundamentals [see figure below]. Strong banks survive runs through various mechanisms, including interbank cooperation, equity injections, public signals of strength, and suspension of convertibility

(3) At the local level, poor fundamentals necessary for runs to translate into large declines in lending. Moreover, bank failures (with and without runs) translate into substantially larger declines in deposits and lending than runs without failures.

Overall takeaways:

- Poor fundamentals are key for whether runs pass through into failure and have severe consequences for the broader economy.

- The findings temper the view that small shocks can result in large jumps to bad equilibria via runs on demandable debt.

Full paper here. Comments welcome. Given the methodology and evolving AI tools, we expect to make refinements to the runs database over time. Any input is welcome.

https://t.co/mbqoFf5g03

If you are looking for a last minute gift for parents/grandparents, I recommend checking out Remento. It is a fantastic way to record family stories. Super easy to use. You choose a prompt and your parent uses their phone to record a response.

My kids have loved hearing stories about my parents’ childhood. It has been a fantastic way to connect as a family. And I’ve learned some things about my parents that I never knew. One of the best gifts I have ever given.

We are doing a lot of work to understand these things empirically. All I can say at the super early stage is that however big people think this problem is, it’s probably larger.

"We know there’s a gender gap in visible tasks, things like who is cooking dinner, doing the housework, coordinating child care. What we don't currently know is whether that gender gap extends to the invisible mental load.” Read our Q&A with @olgastoddard: https://t.co/O7ZhjQvXUR

Fed Chair Powell on independence: "We're never going to be influenced by any political pressure. People can say whatever they want. That's fine. That's not a problem, but we will do what we do strictly without consideration of political or any other extraneous factors."

🚨 New working paper with @CGorback !

We ask what happens when households are more likely to WANT to own a home for cultural reasons? We find homeownership increases, they're more responsive to credit supply shocks, and more of their retirement portfolios are in real estate. 🧵

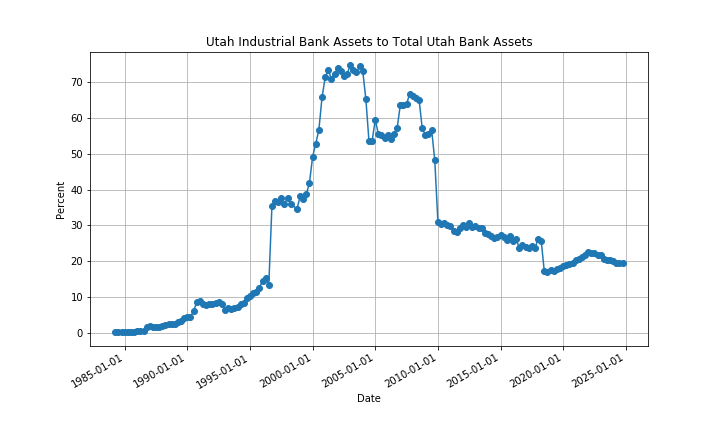

While industrial banks are a small part of total banking assets (about 1%), they play a huge role in Utah, where they make up 20% of bank assets. At their peak in the early 2000s, industrial banks made up 75% of Utah's bank assets.

Over the last few months, I helped CNBC with a brief segment highlighting the role of industrial banks in Utah. Industrial bank charters allow non-financial companies to own a bank. Watch the clip and learn more at https://t.co/DuVDZoIr3m

Utah became a hub for industrial banks thanks to a historical quirk (exemption to the Bank Holding Company Act in 1987 for states with then-active industrial bank charters) and proactive state banking regulators. Today, around 89% of industrial bank assets are headquartered in UT

New paper alert! We estimate bank franchise value and its exposure to interest rate risk, i.e., its duration. We look at the combined effect of several moving parts: (1/n)

You can listen to the new Christmas album from my son's orchestra at https://t.co/UKghsLOIvr, or search for Counting Christmas Blessings by Lyceum Philharmonic. Such a talented group of teenage musicians! It is so fun to have my son be part of this group.

![EmilVerner's tweet photo. New paper on bank runs with Correia and Luck:

"Bank Runs With and Without Bank Failure"

Questions:

- What are the determinants of runs?

- When do bank runs result in bank failure?

- Can runs trigger the failure of healthy banks and amplify small shocks into large crises?

- Are runs themselves the initial cause of financial distress or are they a symptom of deeper fundamental solvency problems in the financial system?

What we do:

- Apply LLMs to historical newspapers to uncover over 4,000 runs on individual banks in the pre-FDIC US banking system from 1863 to 1934. Capture the most famous runs (Bank of the US

- Merge data on runs and other bank-level events discussed in newspapers (suspensions, failures) to bank-level fundamentals (harder than it sounds!)

What we find:

(1) Runs are considerably more likely in weak banks, but can also occur in strong banks, especially in response to negative news about the real economy or the broader banking system.

(2) However, runs typically only result in failure for banks with weak fundamentals [see figure below]. Strong banks survive runs through various mechanisms, including interbank cooperation, equity injections, public signals of strength, and suspension of convertibility

(3) At the local level, poor fundamentals necessary for runs to translate into large declines in lending. Moreover, bank failures (with and without runs) translate into substantially larger declines in deposits and lending than runs without failures.

Overall takeaways:

- Poor fundamentals are key for whether runs pass through into failure and have severe consequences for the broader economy.

- The findings temper the view that small shocks can result in large jumps to bad equilibria via runs on demandable debt.

Full paper here. Comments welcome. Given the methodology and evolving AI tools, we expect to make refinements to the runs database over time. Any input is welcome.

https://t.co/mbqoFf5g03](https://pbs.twimg.com/media/G_t-m1nWUAAMwcO.jpg)