@ptuomov This is so beautifully written and brutal in its clear-eyed view of reality. Do you have any other favorite papers on these topics other than the writings of Asness and Lamont as you mentioned?

@SowingAlphaSeed@frothyassets Thanks! Do you hold them to expiry? I run levered L/S and share your view about trying to protect the tails cheaply, but haven’t settled on a single way.

IMHO Scott Kennedy at the REIT forum (https://t.co/Dy4SkSPkPI) does good granular analysis of BDCs like $CSWC with accurate estimates of weekly NAVs and quarterly earnings forecasts. I don’t agree with some of the strategic perspectives (some secular losers are “strong buys” for example, based on discounts to NAV, though they will be given high “risk” scores). But the analysis is detailed and informed.

I don't think these companies should be put into SPY and QQQ immediately.

We need to the public markets to flush out any private markets valuation disconnects first.

VC multiples are always way too high, even for great companies.

@orrdavid With shorts that seem obviously headed to zero, I find a main challenge is to balance between trading (covering) to protect against violent upswings, versus doing nothing but eating a big temporary setback as the market gets irrational for a while again.

@orrdavid I think the correlation makes sense. Their quant process emphasizes value, quality, and momentum—much like a good fundamental investor. But they run their strategies with such small weights that they care little about getting any given company “right” or “wrong.”

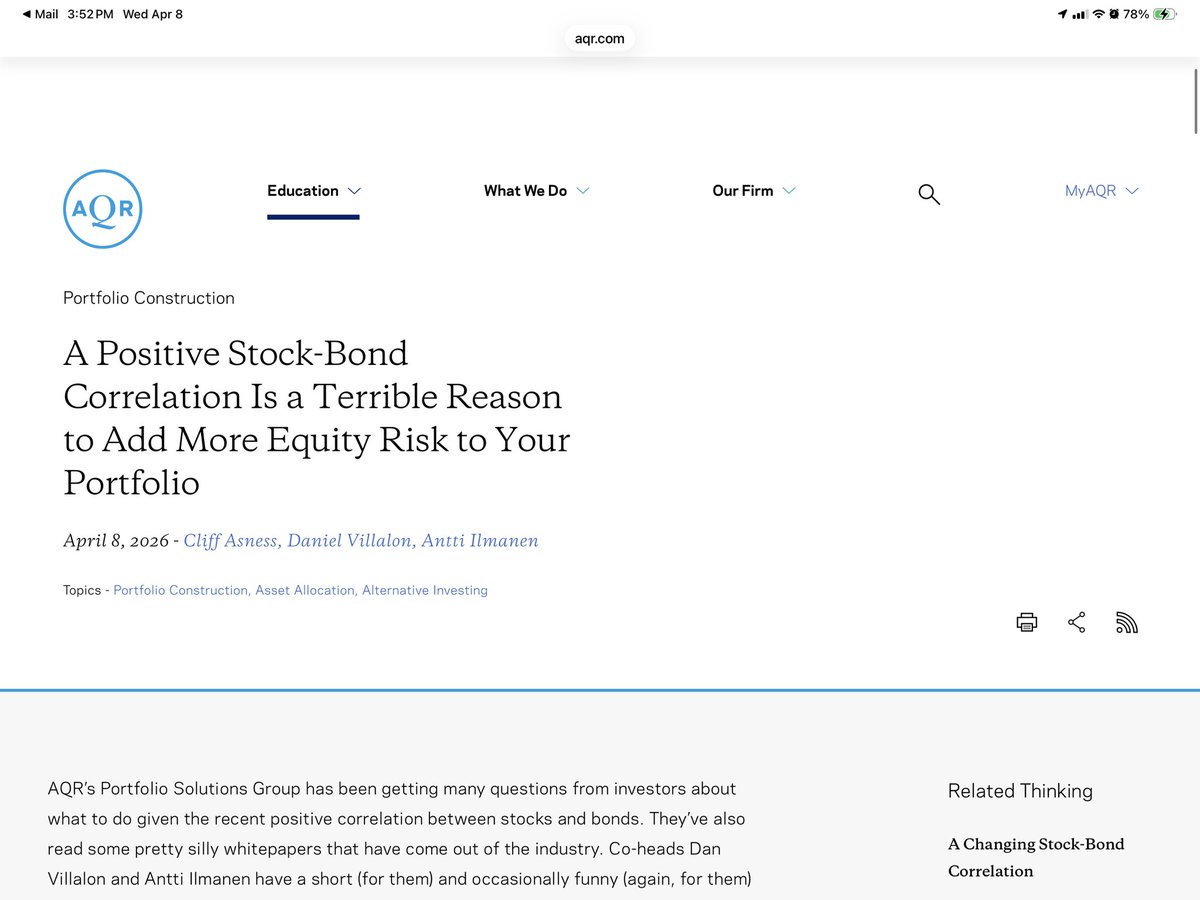

One of the dumber things you hear lately, from a lot of supposedly non-dumb people, is “stocks and bonds are now trading positively correlated so you now desperately need this other investment that’s way way more correlated with stocks than are bonds.”

Those investments are the typical. Privates (which are just equity, so it’s “you need more equity to diversify your equity”), buffer funds (which are just equity + cash minus some number), and crypto (which increasingly trades like equity, and is, you know, mostly nonsense, but even if you love it it’s currently bringing more equity exposure than bonds).

My colleagues latest explaining:

$CAR stock makes the pain of shorts really obvious. Until enough are forced to capitulate, it probably stays strong. And we probably continue to get more extreme weird blow outs in junk like $BIRD until that happens.

Very hard market to be a long/short...

I am incredibly disappointed the federal government announced plans to remove the extremely important and used protected bike lane on 15th Street along the National Mall. This is one of the most popular bike lanes in the District and it connects DC residents and visitors to Downtown to the Wharf and to Virginia. This is an important avenue to keep pedestrians and bicyclists safe, and to keep bikes and scooters off the sidewalks in these high traffic areas.

I am working on alternatives to protect this bike lane. I will keep you posted.

@DrewCohenMoney Thanks! What was giving me pause is that the total impact of the debt discount is getting captured across time on all 3 financial statements, whereas the SBC impact on a shareholder is not. But if you’re creating a FCF multiple based on a single period, then this makes sense.