🚀 WATCHLIST IF YOU'RE BULLISH ON #DEFENCE & #AEROSPACE 🇮🇳��️

These listed companies could remain in focus as India's defence manufacturing ecosystem continues to expand:

🔹 Paras Defence & Space Tech

🔹 Data Patterns

🔹 Apollo Micro Systems

🔹 Astra Microwave Products

🔹 Azad Engineering

🔹 MTAR Technologies

🔹 Avantel

🔹 Premier Explosives

🔹 Unimech Aerospace

🔹 AXISCADES Technologies

🔹 CFF Fluid Control

🔹 NIBE

🔹 TechEra Engineering

🔹 Shree Refrigerations

📌 Save this watchlist and track their order books, execution, and earnings over the long term.

⚠️ Disclaimer: This post is for educational purposes only and is not investment advice. Please do your own research (DYOR) before investing.

It's surprising to see many stalwarts of Investing fraternity lamenting the sale of #Axiscades share by the promoter without going into the background.

Do they not go through the concall details? No efforts Pundits?

For those who are not aware, the Chairman quite clearly said in Q1 26 concall (42.00 minutes onwards) that concerns had been raised by the JV partners on the promoter being Politically Exposed Person, their shareholding needs to be brought down to below 50%

This sale is quite in line with that.

I don't have anything to say whether Power 930 will be achieved or not, but this is the context of the sale.

Not a financial advisor please do your due diligence

#investing

I've been staring at Anondita Medicare's numbers for the last two days and I keep asking myself the same question — is this the next Cupid?

Not in a "buy this stock" way. In a "wait, this setup looks familiar" way.

But here's the thing — and this is where I want to be honest with you instead of hyping a narrative —

So this isn't a "which one to buy" post.

It's a "here's exactly where each one is strong, and where each one is exposed" post. Because that's the only way you actually understand if a smaller player has a real shot at closing the distance — or if it's just wishful pattern-matching.

Let me walk you through why.

1/Cupid was a boring rubber company for years. Then it quietly became a WHO-certified export machine, then a nitrile innovator, then — out of nowhere — a ₹331 Cr bet on retail through Baazar Style. Each phase looked unrelated until you zoomed out.

Anondita feels like it's mid-transition through that exact same arc right now. Contract manufacturer → building its own brand → chasing the same global certifications Cupid already has in hand.

That's the pattern that got my attention.

2/ The Business Models

Anondita: B2B contract manufacturer transitioning into its own brand (the classic "COBRA" playbook — Contract → Owned Brand)

Cupid: Already a hybrid — strong global exports + a fast-scaling domestic FMCG arm

One is becoming what the other already is.

3/ FY26 Financials — Small vs Scaled

Revenue • Anondita: ₹137.42 Cr • Cupid: ₹357.71 Cr

EBITDA Margin • Anondita: 37.48% • Cupid: 32.63%

Net Profit Margin • Anondita: 24.96% • Cupid: 30.26%

Interesting — Anondita is actually more efficient at the operating level right now. Smaller, but tighter.

4/ Where Cupid is simply ahead

→ Only Indian manufacturer with dual-polymer dipping lines (latex + nitrile, zero cross-contamination)

→ Actively developing Nitrile Female Condoms — a category one single global player has historically monopolized, at 25-35% pricing premium

→ Already holds full WHO/UNFPA prequalification (male + female). Anondita is still in advanced application stages

→ Exports to 125+ countries — genuine global diversification

This is the gap that matters most. Certifications and global tenders take years to build, not quarters.

5/ Where Anondita actually punches above its size

→ India's first MDSAP certification under ISO 13485:2016 — one audit clears USA, Canada, Brazil, Japan, Australia. Cupid doesn't have this

→ 100% in-house printing, packaging, boxing — zero vendor dependency

→ Runs entirely on CNG biofuel — real energy-cost insulation most peers don't have

These aren't small edges. If Anondita converts these into export wins, the MDSAP shield alone could open doors Cupid still has to fight for.

6/ The Retail Play — very different philosophies

Cupid's approach:

Buy the ecosystem. ₹331.53 Cr into Baazar Style Retail = instant access to 260+ stores, scaling to 500+ in 2-3 years. Expected to add ₹150 Cr incremental revenue by FY27. Backed by "Cobra" and "Angel" sub-brand personal care lines.

Anondita's approach:

Build the pyramid brick by brick.

26 Super Stockists → 195 Distributors → 4,569 Retailers, concentrated in North, East, West India. Slower, but it's owned infrastructure, not a bought one.

One bought speed. One is earning it the traditional way.

7/ The Forward Maps

Cupid: ₹660 Cr revenue target for FY27 → ₹1,150 Cr by FY29, with ₹390 Cr net profit. Driven by tenders, premiumization, retail expansion.

Anondita: 60-70% revenue growth targeted for FY27, EBITDA margin normalizing to ~30%.

Big swing factors — South African government tenders and UNFPA market access by late FY26/early FY27. Long-term raw material security via an in-house latex plantation coming in 2029.

Cupid's map is proven execution. Anondita's map is a bet on catalysts landing on time.

8/ My honest read

Anondita isn't the next Cupid today. It's Cupid at an earlier chapter — smaller, hungrier, with real structural advantages (MDSAP, in-house ops, energy cost edge) but still missing the global certifications and distribution scale that took Cupid years to build.

Whether it closes that gap depends entirely on execution — the UNFPA approval, the South African tenders, converting owned-brand into real market share.

That's the thing to track, not the comparison itself.

This is purely my personal analysis for learning and discussion — not investment advice. Please do your own research before making any decisions.

What's your read — does Anondita have what it takes to follow Cupid's path, or is this too early to call? Drop your thoughts below.

#cupid #SmallCapStocks #smallcap

One brokerage did 30 yr DCF to value #Aequs and the target price is still 50x FY29 EV/EBIDTA

30 yr DCF… estimating FY56 sales and cashflow… wow

Request to do the same for #Azad

Indian Amines players: with ADDs on EDA & Acetonitrile on China, Saudi and Taiwan, we expect a significant upside in margins going forward. On the raw material side, prices have eased for both methanol and ammonia.

Growth triggers for Viyash Scientific summarised : Major medium term growth to be attributed by multiple formulations going off patent and company having strong pipeline for companion animal vertical .

Data sourced via @stockscansin

Disclaimer : Not a buy / sell recommendation.

Tam for EMS industry

India is emerging as a key global electronics manufacturing hub, with the EMS industry expected to grow at 25-30% CAGR over FY24-29E.

Growth is driven by the China+1 shift, electronics exports reaching ~USD48b in FY26 (+25% YoY), and policy support through PLI, INR400b ECMS and semiconductor initiatives.

With India accounting for only 4-5% of the global EMS market, increasing component localization and export-led manufacturing provide a long runway for growth.

EMS companies which will go backwards into component manufacturing are the ones where complete integrated business models will be created

High-Quality Small Cap Stocks to Watch

🔹 Atlanta Electricals

🔹 Quality Power

🔹 KRN Heat Exchanger

🔹 Sigma Advanced Systems

🔹 CMR Green Technologies

🔹 Sedemac Mechatronics

🔹 Apollo Micro Systems

🔹 Precision Wires

🔹 KSH International

🔹 TD Power Systems

🔹 Aeroflex Industries

🔹 Inox India

🔹 Senores Pharmaceuticals

🔹 Powerica

🔹 Viviana Power Tech

🔹 Syrma SGS Technology

🔹 Sansera Engineering

🔹 GMDC

🔹 ACME Solar Holdings

🔹 Marine Electricals

🔹 Tenneco Clean Air India

🔹 Park Medi World

🔹 Yatharth Hospital

🔹 Omnitech Engineering

🔹 Aequs

🔹 Krishna Defence

🔹 Modern Insulators

🔹 Gala Precision Engineering

🔹 Universal Cables

🔹 Azad Engineering

🔹 POCL (Pondy Oxides & Chemicals)

🔹 Lloyds Engineering Works

📌 These companies operate across sectors such as Power, Defence, Electronics, Precision Engineering, Industrial Manufacturing, Healthcare, Renewables, Cables, and Capital Goods. They are worth tracking and studying from both a fundamental and technical perspective.

One pager Growth catalysts summarised for Ather Energy

Key triggers include doubling the capacity in H2 of this year and the launch of mass product platform EL .

Disc : Not a buy sell recommendation

Data sourced using @stockscansin

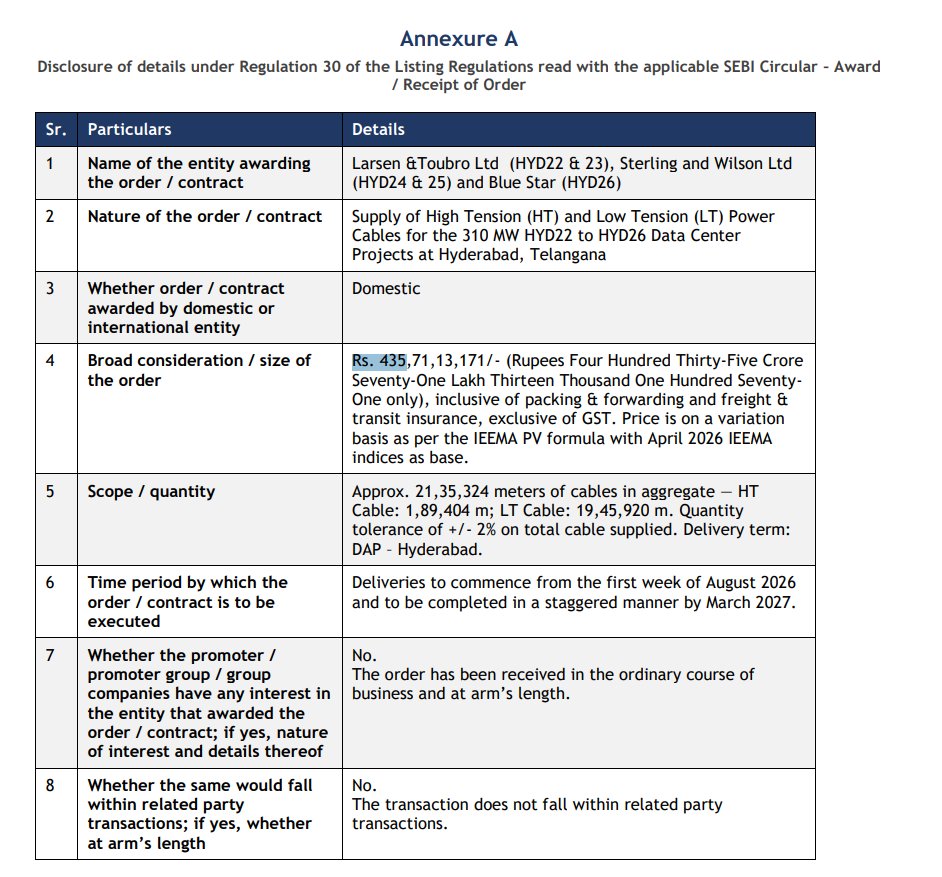

Diamond Power Infrastructure Ltd

#DIACAB

Order won- 435cr for supply of HT & LT cables for Hyderabad Data Center.

Execution time- Aug 2026-March 2027

Note- They are also raising 2000cr via QIP

"By 2030, We Want to Be Recognised Globally as a Diversified Engineering & Solutions Company": Parag Satpute, MD & CEO, Greaves Cotton — "India Continues to Remain the Centre of Our Operations"

The Context

Greaves Cotton entering a fresh growth phase under its new business strategy, transforming from an engine maker into a diversified engineering company

Parag Satpute (MD & CEO) speaks on FY26 performance, the ₹500-700 crore investment plan, Dubai expansion, export strategy, growing focus on energy solutions, and the roadmap to build a globally recognised automotive engineering and solutions company by 2030

FY26 Performance — Double-Digit Growth

FY26 marked the transition from strategy to execution under the "Greaves Next" strategy

Consolidated revenue grew 18% to ₹3,437 crore; standalone revenue rose 19% to ₹2,365 crore

Consolidated EBITDA stood at ₹239 crore; Operating PBT (Profit Before Tax) at ₹154 crore, with margins improving by 210 basis points

Standalone EBITDA reached ₹320 crore; Operating PBT ₹312 crore

Growth was broad-based: energy solutions growing 20%, mobility solutions 16%, industrial solutions 6%

Also crossed ₹1,000 crore in quarterly consolidated revenue during Q4 — an important milestone

Performance reflects Greaves Cotton's transformation from a 165-year-old single-cylinder engine manufacturer into a diversified engineering company

Today, operates across mobility, energy and industrial solutions, while expanding into electric mobility through Greaves Electric Mobility and in financial services through Greaves Finance

India continues to remain the centre of operations, engineering and manufacturing, with facilities at Chhatrapati Sambhajinagar, Talegaon and Nagpur serving both domestic and export markets

International business contributed 13% of core business revenue in FY26, up from 9% a year earlier

Sees significant opportunities across the Middle East, Africa and Europe

For FY27, focus will remain on disciplined execution, expanding margins, scaling growth opportunities, and maintaining prudent capital allocation while continuing to build a diversified engineering business

Dubai Expansion — Strategic Rationale

Recently established Greaves International Trading FZE (GITFZE) in Dubai

Marks a key step in strengthening international business under the new strategy

Based in Dubai, will serve as a regional hub for trading, distribution, customer support and supply chain coordination across mobility, energy and industrial solutions businesses

Initially covering the GCC markets, will later expand into the Levant and Africa, reinforcing strategy to deepen customer proximity and expand global footprint

Energy Solutions — Growing Focus

Mobility will remain a core business, but energy solutions offer significant long-term potential given India's infrastructure, industrial and data centre ecosystems expand

Opportunity extends beyond gensets to integrated power solutions, lifecycle services, remote monitoring and battery energy storage systems

Energy solutions grew 20% in FY26, while aftermarket business expanded around 35%

Going forward, all three verticals — mobility, energy and industrial solutions — will remain key growth engines

Investment Plans

Planning an investment of ₹500-700 crore to strengthen flexible manufacturing, multi-fuel platforms, advanced powertrain technologies and engineering capabilities across all three businesses

Objective: build long-term competitiveness and multiple growth engines rather than simply adding manufacturing capacity

Capital allocation will continue to be guided by strategic relevance and sustainable value creation

2030 Vision

By 2030, want Greaves Cotton to be recognised globally as a diversified engineering and solutions company

Through new strategy, strengthening technology capabilities, expanding internationally, and moving beyond products to integrated engineering solutions, lifecycle support and long-term customer partnerships

While showcasing Indian manufacturing and engineering on the global stage

Core Theme:

Greaves Cotton's FY26 results — 18% consolidated revenue growth, margin expansion, and international revenue nearly doubling its share — mark a decisive validation of its pivot from a legacy single-cylinder engine manufacturer to a diversified mobility-energy-industrial engineering conglomerate; with the new Dubai trading hub anchoring GCC-to-Africa expansion and a fresh ₹500-700 crore investment aimed at flexible, multi-fuel manufacturing capabilities, Satpute's strategy bets on energy solutions (up 20%, tied to India's infrastructure and data-centre boom) as the next major growth engine — positioning the 165-year-old company to reinvent itself as a globally recognised, India-rooted engineering and solutions brand by 2030.

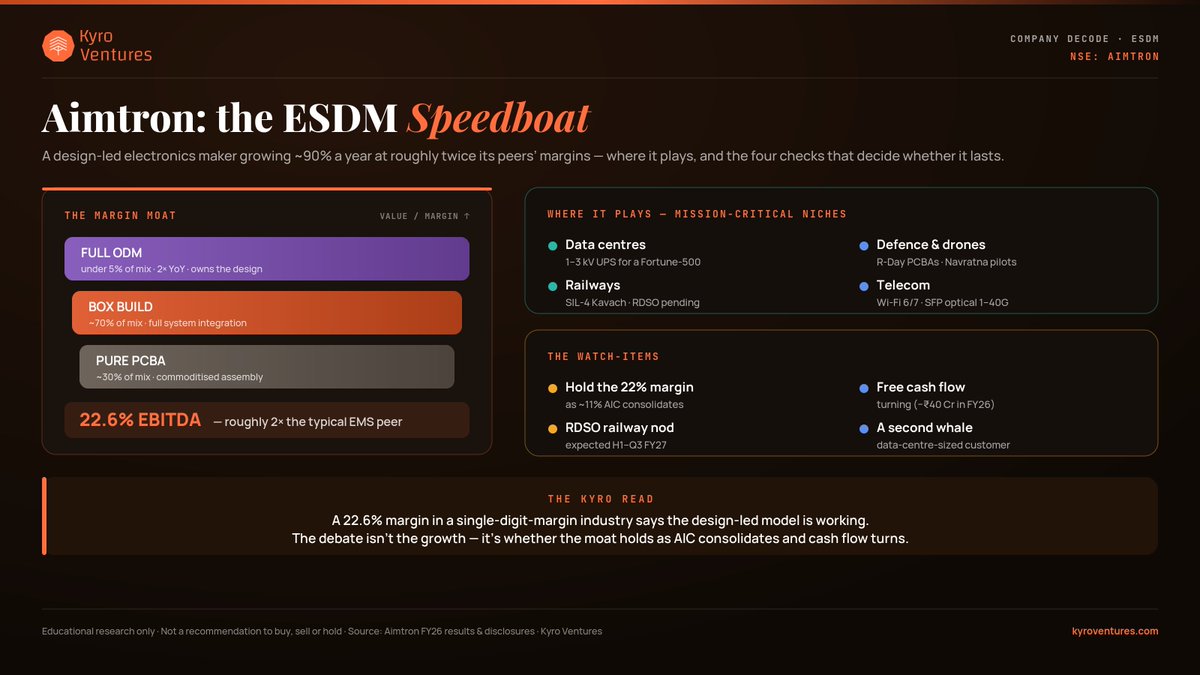

Aimtron Electronics just tagged a fresh all-time high Here's the actual business behind the move.

It isn't a commodity PCB assembler. It's an ESDM player: ~70% of its mix is now "box build" — full product integration, not just stuffing boards — which is why it earns a 22.6% EBITDA margin versus the 6–9% typical of Indian EMS. That single gap is the whole thesis.

The numbers back it: FY26 revenue +89% to ₹301 Cr, PAT +79% to ₹46 Cr. Order book ~₹600 Cr (≈2x sales) with live RFQs near ₹900–950 Cr — real forward visibility, not a vibe.

And it fishes in high-barrier ponds: 1–3 kV data-centre UPS for a Fortune-500, SIL-4 railway safety (Kavach, RDSO approval pending), defence drones, Wi-Fi 6/7 + optical telecom — plus a just-closed US acquisition (AIC) that opens Fortune-500 supply chains.

The other side, because there always is one: at ~70x, a lot is already in the price. Free cash flow was negative in FY26 (~−₹40 Cr), working capital is heavy, the US deal dilutes margins before it helps, and several marquee wins still rest on single customers.

So four things decide the next leg — does the 22% margin hold as AIC consolidates, does cash flow turn, does the RDSO nod land, and does a second data-centre-sized customer show up?

Full decode - https://t.co/BiAwtYrvO5

Disc: Not a recommendation

The market saw Cyient DLM "miss" FY26: revenue −17% - It missed the more interesting number.

The order book hit an all-time high — ₹2,417 cr, a record 1.5× book-to-bill — while margins rose to their best-ever.

For this kind of business, the order book is a clock and revenue is its echo, about a year later. FY25's weak intake became FY26's soft revenue. FY26's record intake is FY27's promise.

A coiled spring finally loading — or a backlog that won't convert?

Kyro Issue #5 reads past the headline ↓ https://t.co/Rnrh9wszk5

Disc: Not a recommendation

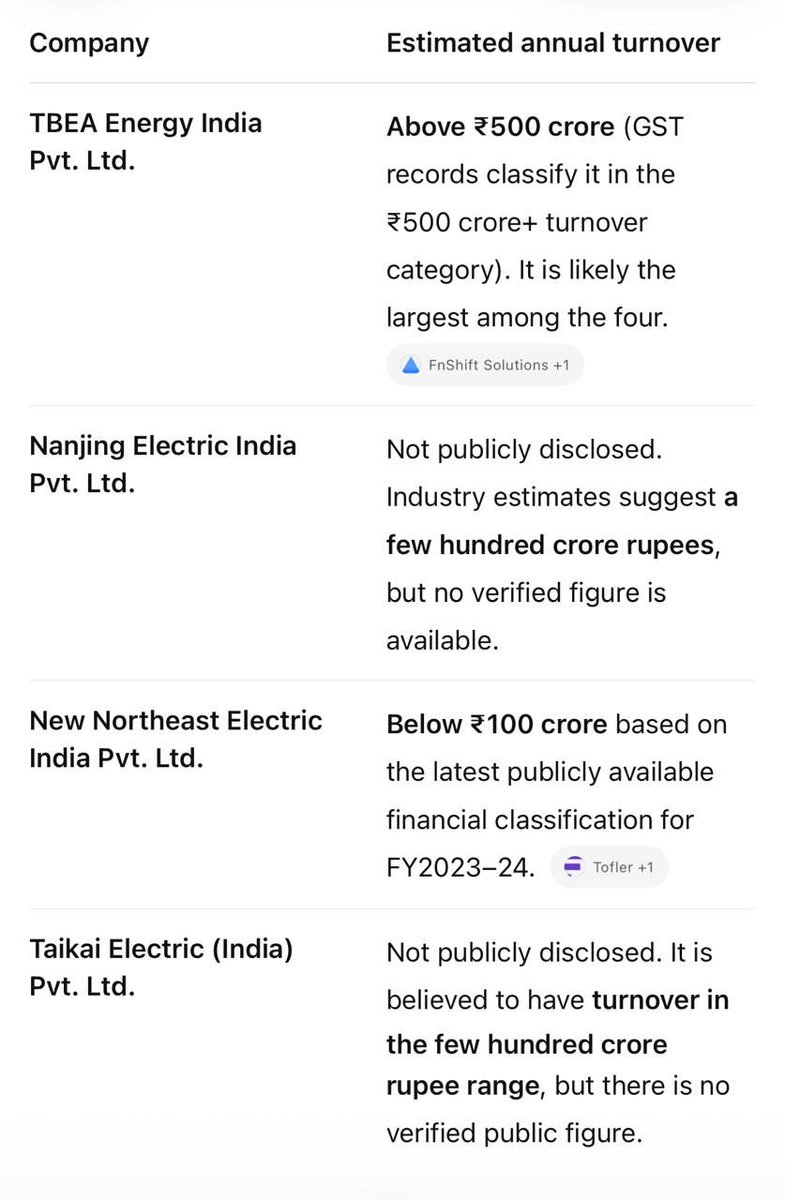

@MithunSarkari Took help of AI to gauge turnover of these Chinese companies. Collective annual turnover of all the four companies is not more than 1500 crores. So, this news is more noise than the substance.

CG POWER, POWER INDIA - No MATERIAL IMPACT

This is applicable only to Chinese cos have plants in India.

EXPECT RECOVERY IN POWER CAP GOOD STOCKS

Transformer: Four Chinese companies allowed to participate in bidding

*Not material impact

*This only allows Chinese companies manufacturing entities in India to participate

*This is along expected lines

ICICI Securities

2/ FY26 was a conscious reset, not a slowdown.

Mgmt deliberately exited volatile brand partnerships, upgraded its customer mix and shifted towards higher-value niches.

The result 👉

▪ FY26 revenue declined 6.4% YoY to 1,768.6 Cr.

▪ But EBITDA grew 7% YoY

▪ PBT grew 18.2% YoY

▪ PAT grew 4.2% YoY

▪ EBITDA margin improved from 6.83% → 7.81%

▪ PBT margin improved from 4.06% → 5.13%

Mgmt: "These decisions, while tempering near-term revenues, have structurally strengthened our core business. The turnaround is already visible in Q4 FY26."