My third year on the floor was one of my most memorable and satisfying of my career. Why? I made $63k. I did not blow out. I paid my bills. I paid my tithe to the gubment. In my mind, I was a success. Great mental capital boost year for me! @AnthonyCrudele

Admin bloat is a big problem and addressing this issue should be the main focus of University leaders as they consider other measures that directly hurt our core mission of research and teaching.

At MIT, for example, faculty grew only 9% from 1985-2023. Administrative staff grew 189%. https://t.co/nAQNqzXAaK

Today was the worst day on SPX this year, the worst day in 164 trading days, and the 2nd worst day in the past year. It was the 8th worst day in the past decade.

There's so much to say about this chart. it shows to very related measures: the ratio of the single stock VIX (VIXEQ) to the $VIX versus SPX 1m implied correlation.

The higher the ratio the lower the implied correl and you can see we are an absolute extreme.

You might say the market is "complacent" by way of the record low IC. Agree the sense that there is a disregard for the potential for a macro shock that hits all assets at once. Said shock would move the current level down and to the right in the chart.

But what's really driving the ratio up and IC down is the level of single stock implied volatility. The number of stocks enveloped in a "spot up, vol up" dynamic is significant. Thus, the VIXEQ is higher now than at the peak of the market shock in late March!

When a stock surges, investors who want to stay long but are worried the rug may be pulled out start looking at call options. They allow you to walk away if things reverse. That demand forces implied vol higher. From the option seller's standpoint, stocks are exhibiting huge one-day "up shocks" that are both difficult and costly to hedge. That gets priced in.

I am reposting my Tweet here on "SK Hijinks" because it' may be the strongest example of the feedback loop between price, implied vol and the overlay of short gamma products.

I think we are getting closer to a tipping point and there's a sharp, tradable reversal forthcoming.

https://t.co/jOrMKeNG13

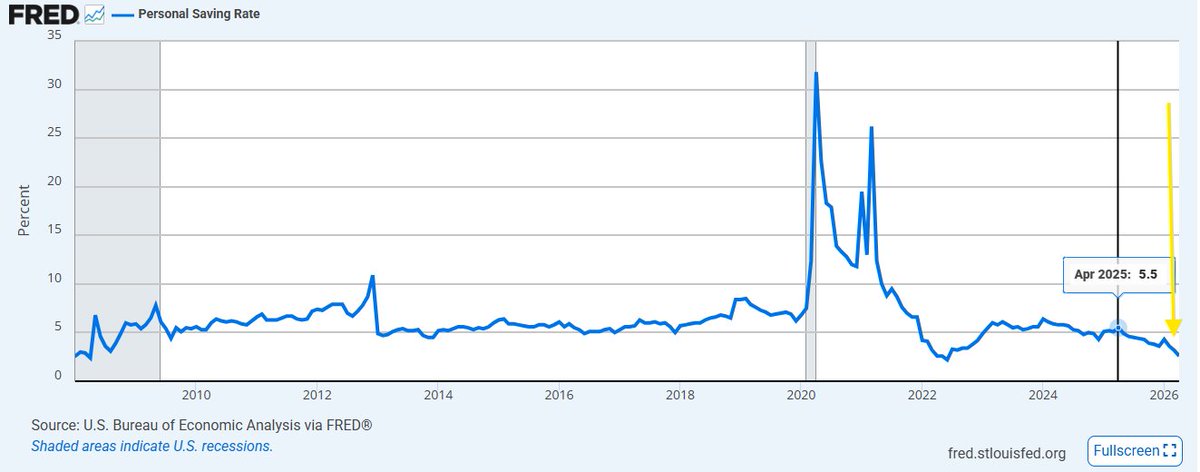

This is stunning.

Personal savings rate April 2025: 5.5%

Personal savings rate April 2026: 2.6%

That's a sharp plunge.

It underscores how squeezed Americans are right now with higher prices and incomes not keeping up.

Maybe you can explain some of this away by Baby Boomers retiring, but not all of it.

Short-ish rant: factor rotation, factor timing, factor horoscopes, skibidi toilet regression and many other quantitative malfeasances originate from quantitative "researchers" (both on the buy and sell side) whose incentive was to raise their status (and comp) by capturing the attention of investors. Because of the Bullshit Asymmetry Principle, dislodging these misconceptions is 10x harder than creating them. Ideally, incentive misalignments should be solved with contracts. But also, like in many professions, an ethical oath would help. First rule: "I won't bullshit the portfolio manager and the business owner alike even if doing so would benefit me".

Feel free to like anonymously, I won't out you.

this is an interesting article. I see things the same way as the author. @QTRResearch

"The Iran war may end sooner than many expect, not because global leaders suddenly become responsible, but because the bond market is forcing them into a corner. Financial instability is becoming the greater threat. Policymakers now face an impossible balancing act between inflation, debt servicing costs, economic slowdown, and geopolitical conflict".

https://t.co/UDRoJvIi5o

I don't understand the grave dancing on QVR's downfall.

It's tough to build any business and sad to watch a few bad months sink 5+ years of hard work.

I hope everyone there lands on their feet.

I really don't get the pile-on against @bennpeifert personally. He's contributed tons of education to the discourse on options/volatility on this hellsite. You can dislike his politics/personal choices without cheering his downfall.

Intraday trend-following strategies are often presented as if the entry signal is the only thing that matters.

In reality, a source of dispersion in performance can emerge from a far less discussed component: the exit policy.

In our latest research piece, we take a simple ATR breakout model on SOXX and keep everything unchanged except for one design choice: how the trade is managed after entry.

We test four distinct exit mechanisms:

1️⃣ Session Open

2️⃣ Session Midline

3️⃣ VWAP

4️⃣ PSAR

What makes the experiment particularly interesting is that all four approaches are intuitive and logically defensible.

Yet despite identical entries and identical position sizing, the realized outcomes diverge meaningfully across key stats.

The deeper we went into the analysis, the clearer one point became:

Once evaluation moves beyond a single metric, the idea of a universally “best” specification starts to break down surprisingly quickly.

This naturally leads into one of the most underrated concepts in systematic trading, in our opinion:

Ensembling.

Rather than trying to predict which specification will dominate going forward, a more robust solution may simply be choosing not to choose.

You can read the full research piece from the link in the first comment 👇

#SystematicTrading #QuantTrading #IntradayTrading #TrendFollowing #AlgoTrading #QuantitativeFinance #TradingResearch #CTA #PortfolioManagement #MomentumTrading

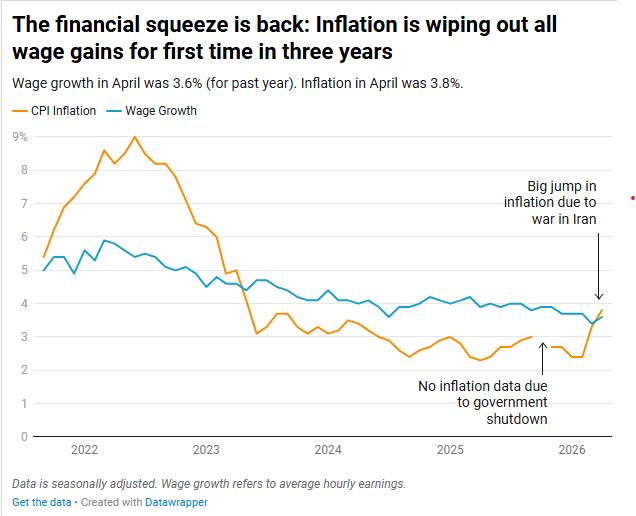

JUST IN: Inflation is now eating up all wage gains for the first time in about three years. This is painful for Americans and a true financial squeeze.

CPI Inflation in past year: 3.8%

Wage gains: in past year: 3.6%

In this video podcast "Cuban's Collar is Jensen's Alpha", I walked through Mark Cuban's spectacular hedge on shares of YHOO back in 1999 and how the economics of the trade were so favorable to him because of implied volatility, skew and interest rates.

In 16 minutes, I think you'll learn a good deal about the pricing dynamics for a "zero cost collar"

https://t.co/nNlbiyoOd9

The same setup exists now for $INTC which is in a sharp "spot up, vol up" episode as a result of realized volatility on up days of 100 versus just 73 on down days this year. Someone lucky enough to be long the shares (that means you, Trump!) can do a zero cost collar out to Dec'28 and limit the downside exposure to just 10% but still enjoy upside of 60% at expiration. The 90/160 collar is zero cost. These are fantastic economics.