This year’s Consensus in Miami made one thing clear: the infrastructure layer of modern finance will be built by teams that understand both technology and regulation.

The best conversations were not about hype, but about regulatory clarity, institutional adoption, payments, compliance, and products that can scale beyond early adopters into the financial mainstream.

That is where the real opportunity is.

#Consensus2026 #CapitalMarkets

A new bar is being set in fintech.

Growth alone isn’t enough. Digital assets are becoming infrastructure. Regulation is turning into advantage.

The next phase rewards those who get all three right. https://t.co/cN4l2X2r8w

Very excited to add @HSBC payments to @CantonNetwork. Soon we will show what’s possible when you have the right partners at the table.

https://t.co/aEcIZu6PAo

The Phoenicians never held a Mediterranean Economic Summit or signed trade treaties. They simply showed up with purple dye, cedar wood, and an eye for profit -- and accidentally created the ancient world's first global economy.

FinTechs are becoming banks while banks are acquiring FinTechs.

→ Revolut is now a bank both in the EU & the UK. Soon, the US as well.

→ Nubank has been a bank in Brazil since 2016, & just got conditional approval in the US.

→ Adyen holds (specialized) banking licences across the EU, UK, and the US.

→ SoFi is a bank since 2022.

→ PayPal, Affirm, Upstart, etc., all recently submitted their banking charter applications.

Yet, it’s significantly harder to be a well-run bank than to have a good app.

Anthropic's biggest miss of 2026 just happened.

Peter Steinberger built OpenClaw — the hottest AI agent on the planet right now.

180K+ GitHub stars. 3.4M views on the announcement tweet. Baidu integrating it. Used in 100+ countries.

And he built it alone. One person. One lobster mascot. 🦞

The kicker? He originally named it "Clawdbot" — after Claude. He recommended Claude Opus 4.6 as the default model. He was basically Anthropic's biggest unpaid evangelist.

Anthropic's response? A trademark cease-and-desist letter.

OpenAI's response? "Come build the future with us." Sam Altman called him a genius on X.

Steinberger spent last week in SF talking to every major lab. Both Zuckerberg and Altman personally courted him. He chose OpenAI.

Here's the part that hits different for the "one person billion dollar company" crowd:

Steinberger openly said he could have turned OpenClaw into a massive company. He chose not to. His words: "What I want is to change the world, not build a large company."

Sam Altman, Dario Amodei, Andrej Karpathy — they all predicted the first solo billion-dollar company would happen by 2026.

Steinberger was the closest anyone has come. 180K stars. Global adoption. Zero employees. Zero VC. And he walked away from the company-building path entirely.

The man sold PSPDFKit for €100M+ before this. He didn't need the money. He needed the mission.

Three lessons from this:

Person building for fun and enjoying his work can do wonders.

Your biggest fans can become your biggest competitors. Don't send cease-and-desists when you should be sending job offers.

And the one-person billion-dollar company might not look like what we expected. The person who could build it might simply choose not to.

What a time to be building in this space.

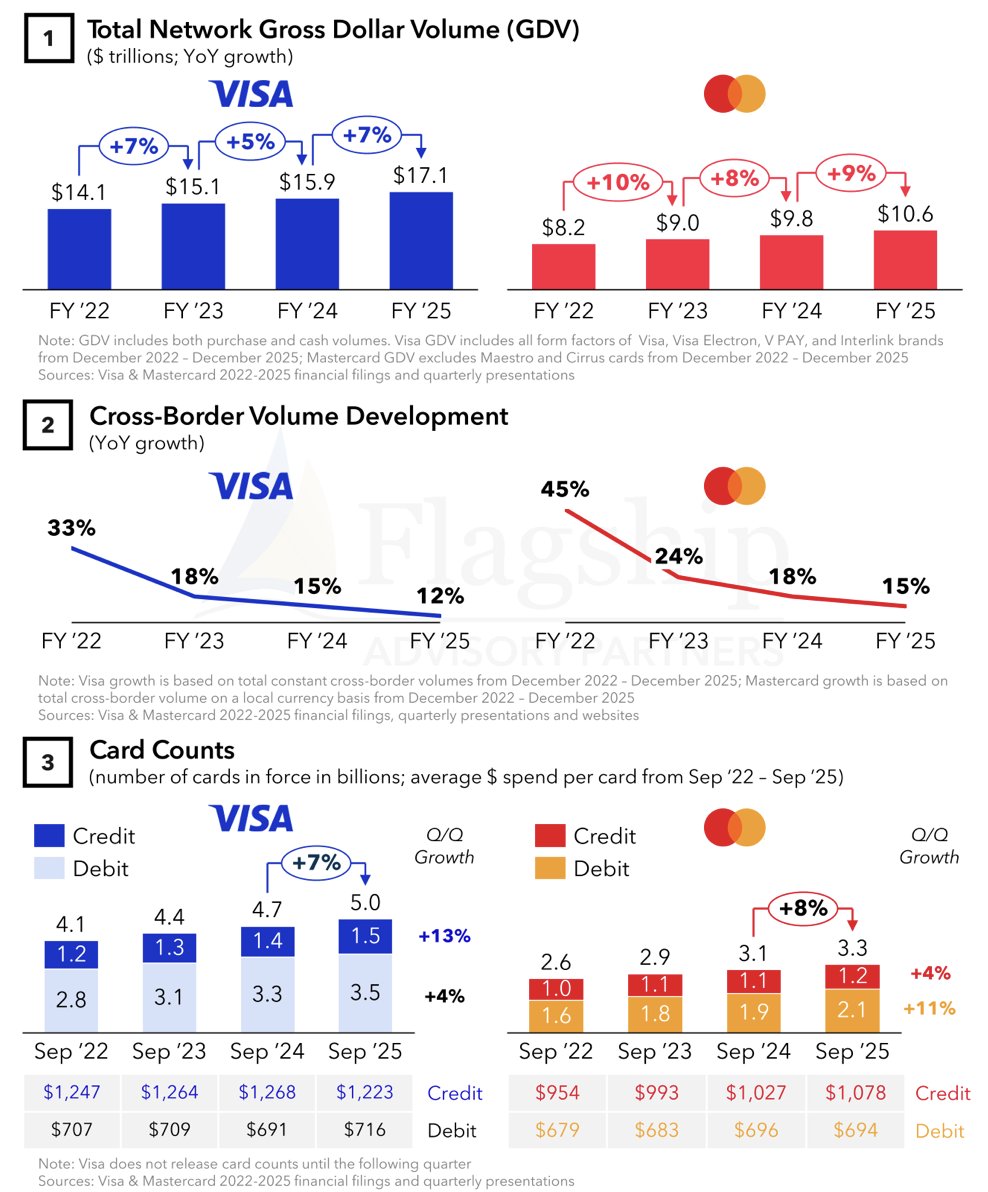

💳 Visa and Mastercard just closed another strong year.

But the quality of growth is quietly shifting..

Visa and Mastercard delivered solid FY2025 results:

• GDV up 7% (Visa) and 9% (Mastercard)

• Net revenue up 12% and 16% respectively

• Value-added services increasingly driving the upside

On the surface: business as usual.

Under the hood? A few trends stand out:

1️⃣ Cross-border growth is slowing — for the third consecutive year

Visa cross-border growth decelerated from 15% → 12%.

Mastercard from 18% → 15%.

Still strong. But the post-pandemic rebound tailwind is fading.

2️⃣ The global card mix is shifting

Visa is leaning more into credit (+13% credit card growth).

Mastercard is leaning more into debit (+11% debit card growth).

Interestingly, Visa saw average spend per credit card decline, suggesting volume growth is increasingly card-count driven, not purely spend driven.

3️⃣ Tokenization is becoming core infrastructure

Over 50% of Visa transactions are now tokenized.

Mastercard is nearing 40%.

Tokenization isn’t just security anymore — it’s embedded into wallets, credentials-on-file, and digital commerce optimization.

4️⃣ Incentives remain aggressive

Client incentives as a % of GDV continue to rise.

Competition between networks, and against local schemes + account-to-account rails, is very real.

The big picture:

Card networks are still compounding at impressive scale.

But the growth mix is changing:

Less pure cross-border momentum.

More value-added services.

More technology layers on top of the rails.

I highly recommend reading the complete source article with more interesting info & stats on this topic by Flagship Advisory Partners: https://t.co/AVJ0UFpX2k

Legora is the fastest YC company of all time to become a unicorn.

It's about to break the record for fastest to $5bn as well.

It finished @ycombinator less than two years ago and is now raising at a $6bn valuation.

Incredible stuff.

AND it's being built in Europe by Europeans

The Dutch:

- Invent the modern stock market in 1602

- Build the financial capital of the world

- Decline slowly for centuries

- Go out with financial suicide in 2026 by taxing unrealized gains at 36%

Remember when Milton Friedman would go around and explain basic economic principles clearly and broadly to the public? We need more of that.

Otherwise we're left with public intellectuals who talk about economics for *decades* without knowing even the basics.

@R_Thaler doing great work pushing back, but wow.

Ive heard two insane things:

1- South East Asia is the fastest growing ecom market on earth.

All the big tech giants are pushing their betas here.

It is the wild west. Billions in spend, millions of merchants, gold rush vibes.

2- Eastern Europe has higher ecom GMV than western europe.

I didnt check this.

But people are saying there are a dozen+ 100m+ brands JUST focused on the former soviet union.

No UK, no Germany, No france.

Poland, Romania, Croatia.

High English penetration.

Entire population online.

GDP exploding.

USA is still number one.

UK, Canada, Australia easier expansion.

But...

Maybe the future is Malaysia, Indonesia, and Poland...

Netflix made $45.2 billion in 2025. YouTube made $44 billion in ad revenue. On a like-for-like basis, these two are nearly identical.

YouTube gets to $60 billion by bundling in YouTube TV, YouTube Premium, YouTube Music, and NFL Sunday Ticket. Comparing that combined number to a single streaming service is like comparing Alphabet’s total revenue to Disney+ and declaring Google won the streaming wars.

The number that actually matters: YouTube paid creators $100 billion over the past four years while spending $0 on content production. Netflix spent $16 billion on content in 2024 alone and has to keep writing that check or the library evaporates.

Google bought YouTube for $1.65 billion in 2006. It now earns that back every 10 days.

YouTube built a model where the content creates itself, the audience sells to advertisers, and the platform collects rent on every transaction. Netflix writes a $16 billion check every year just to keep the catalog from shrinking.