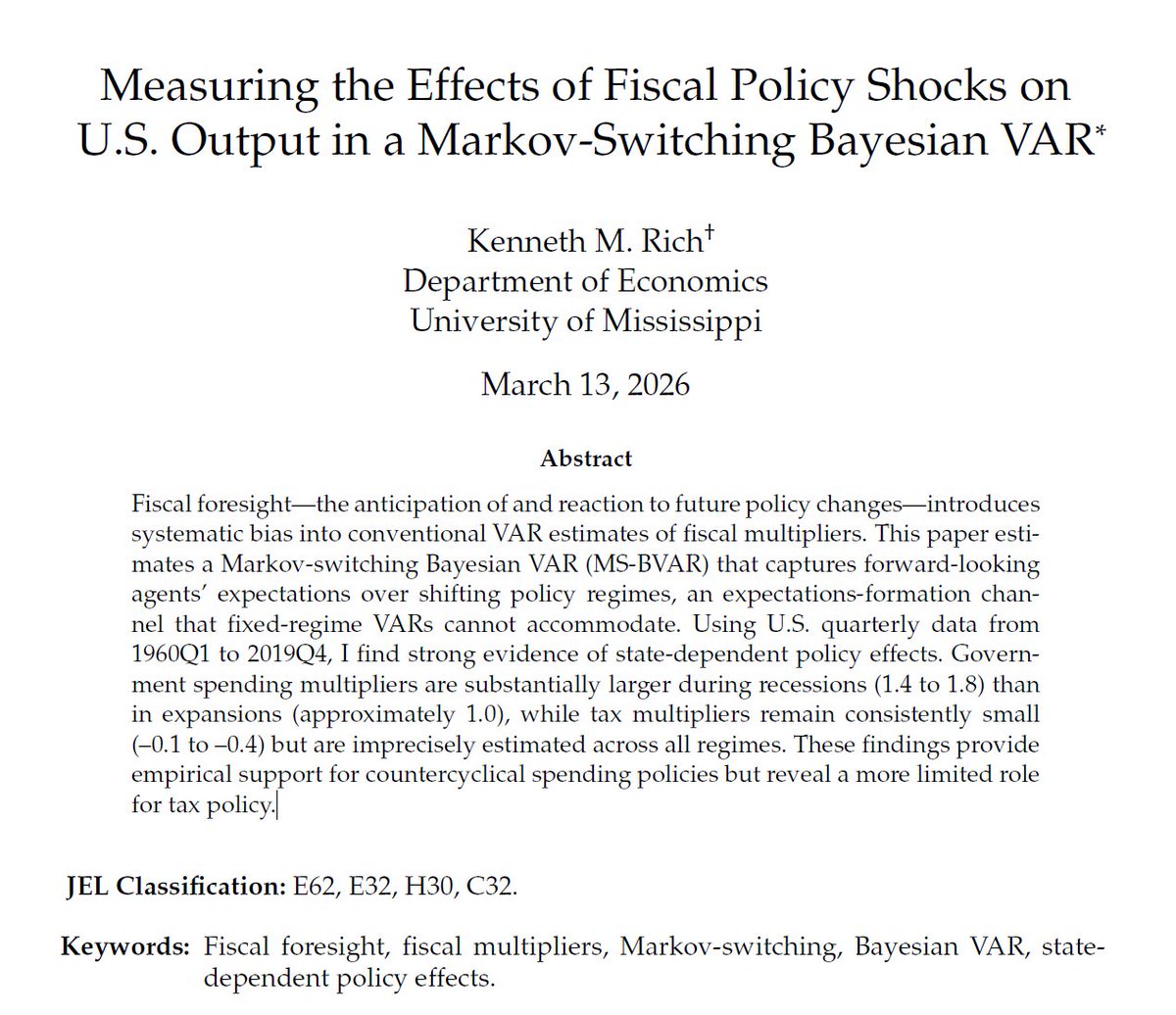

New draft out!

Must be spring break — another paper update 😅

Conventional VARs can't recover fiscal shocks when agents anticipate policy changes.

I demonstrate that an MS-BVAR solves this by showing that regime switching is both the source of foresight and the key to identification.

Key Results:

1) Spending multipliers are large and state-dependent (1.4–1.8 in recessions, ~1.0 in expansions).

2) Tax multipliers: consistently small across all regimes — much smaller than conventional estimates suggest.

https://t.co/EcfG3bavMG

To add to this: Both Keynesians (e.g., Tobin) and Monetarists (Brunner and Meltzer) shared views about monetary transmission that most New Keynesian models simply ignore.

For instance, Tobin (AEA: P&P, 1961) and Brunner and Meltzer (JPE, 1972) emphasize that a complete theory of monetary transmission must discuss how policy changes the relative price of inside to outside money.

My 2023 BEJM paper discusses this in more detail.

One of the things you quickly learn when doing serious work in economics is that seemingly disperate ideas may be strongly related.

Local projections and VARs are a good example. Of course, if you know about Dufour's work, you heard of Dufour and Renault (1998) and you were not at all shocked by equivalence results in Plagborg-Moller and Wolf (2021).

That isn't all. DSGE models imply a VARMA structure. That's the ABC (and D's) paper of Fernandez-Villaverde et al. (2007). More generally, a DSGE model is a constrained DFM. The empirical tools we use estimate the objects we often care about in theory -- dynamic causal effects of shocks, their share of variance explained, etc. And you can write *all* of this using the treatment effect or potential outcome language most often seen in microeconometrics. Some non-trivial insights on the difficulty to estimate nonlinear effects emerge from that (e.g., Kolesar and Plagborg-Moller, 2025).

A lot of people who comment on social media go for political punch lines, engaging in attention farming and limiting themselves to superficial differences. But that's unserious.

@mikekofoed@ekgibbons Mine too.

However, I always joke with my students that the most unrealistic part about the West Wing is that an economist was elected President.

I personally teach Intermediate Macro using the Garin, Lester, and Sims text (which is available on Eric Sims’ website).

We cover a simple two-period consumption-saving model that can be extended to discuss topics like microfoundations, Ricardian Equivalence, and the Neoclassical and New Keynesian models.

This paper seems like a great complement to consider for future classes.

All for incorporating DSGE models into the undergraduate curriculum.

Sobre a discussão IS-LM e/ou DSGE na graduação, deixo pra outros. Minha contribuição para o graduando interessado (ou algum professor que busca ideias): leiam este artigo!

https://t.co/HKOevvU8gX

@AngusBylsma My intermediate macro in undergrad was 4 weeks review of Principles, 4 weeks Solow, and the remainder was IS/LM.

However that was about 14 years ago 💀