Weakness in wage growth stands in contrast to the strong labor market narrative many are taking for granted as reality. AHE at 3.4% at cycle lows, and averaged 2.7% last 3m annualized.

We provide this estimate of net corporate supply and demand of share to our clients. Even we are surprised with how sharply the scarcity of equities has shifted to neutral. It doesn't include RSU sales which we include with a different cohort and are exploding higher in supply

Till last month my $40 @github co-pilot subscription could easily last the whole month. With new changes, 50% credits consumed in 4 days. #Vibecoding will fade at this pace and will severely impact many companies.

A brief musing. What if someone had a great idea or it was mailed down from some deity.

The idea was a way to increase output. The key thing about this "pure" idea is it was implanted in every humans brain and incorporated in every corporate plan instantly AND it took no capex to implement. Also the nature of the idea was such that it had no impact on the leverage of capital owners vs labor in either direction. What would be the macro economic consequences? As far as I can tell it would be a pure standard of living increase for all Society in a relatively equal way. I muse about this because it helps me understand how a less clean productivity miracle is distributed

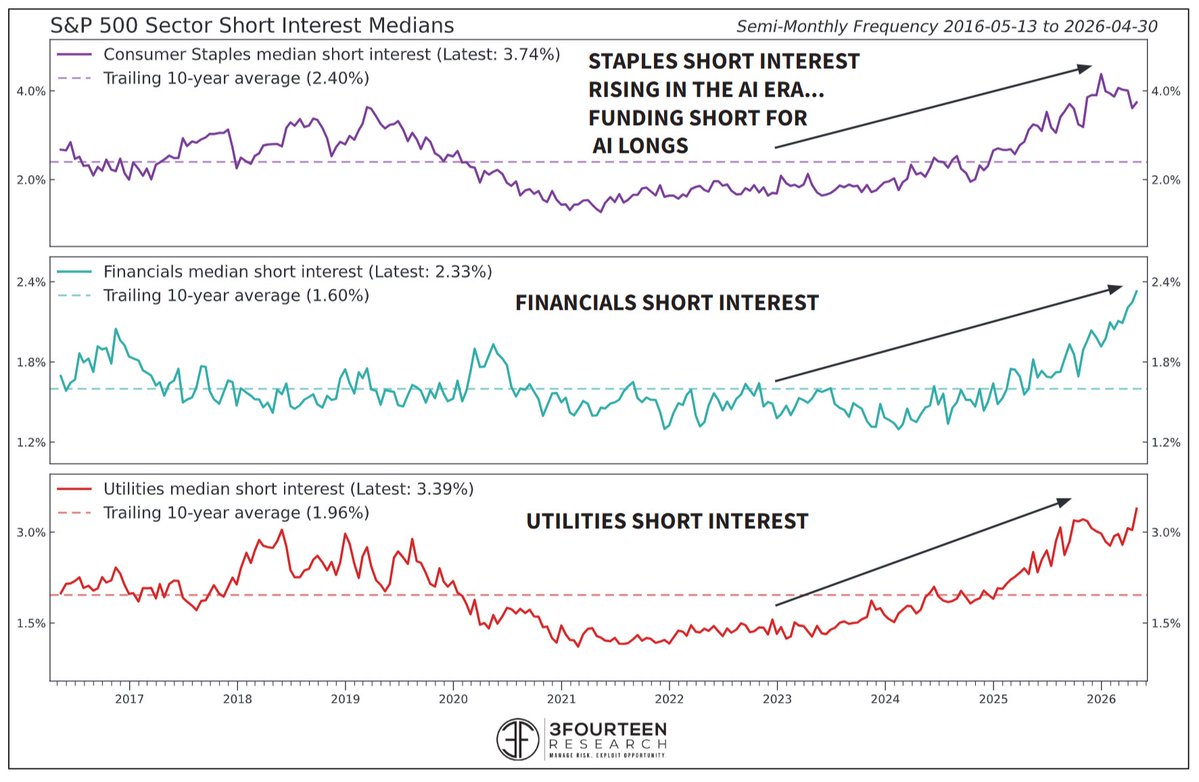

This market is still semis vs funding shorts.

Short interest in non-AI market segments started hooking higher in mid-2024.

You really see it on a day like today (SOXX -2% vs SP EW +.78%).

AI Doomers say $7-$8 trillion in AI infrastructure investment by 2031 cant possibly achieve a value creative ROI. It sounds too large as it has a scary word “trillion” on it. Here’s a different macro perspective:

- Total Developed World wages bill is ~$30 tr going to $38 tr by 2031

- Total Developed World corporate revenues are ~$130 tr growing to $165 tr by 2031.

- To achieve a value creative 15% ROIC over $8 tr of AI investment, requires incremental NOPAT of $1.2tr = EBIT of $1.5tr by 2031.

- Or; at an avg developed world EBIT margin of 12%, that implies $12.5tr of revenue growth.

That can be achieved by EITHER:

- Only one year of wages bill inflation banked in cost savings (over 6 years); or

- Additional cumulative revenue growth across developed world corporates of 8% over 6 years or 1.3 percentage points p.a.

- or; a conbination of the above

The most likely major component is the first one mentioned. While tokenmaxxing is plain stupid and wasteful, the weight of evidence from corporates is that they are slowing or entirely stopping new hires as they are able to bank efficiencies that AI generates. Coding teams, customer service staff, back and middle office, middle management etc etc.

Continued revenue growth, flatter headcount, rising EBIT margins.

The evidence supports this. Across the US, Japan and even Europe, corporate margins are at or near record highs and rising.

Why equity 101?

Today's Google issuance (something i have been forecasting for 6 months) may be a one off or may be a start of a broad use of funding via equity issuance for all the capex folks and even Costco or Walmart or anyone else. Why equity?

That takes me back to my first lessons of corporate finance learned in 1986-1988 as a quant corporate finance analyst. The topic is extremely well understood and the basis of corporate finance theory for a half century and probably longer. It has three big concepts

1. Is asset liability matching

2. Is optimal capital structure

3. Is cost of capital.

All else equal a company wants to perfectly match its assets to its liabilities and share holder equity.

All else equal a company wants to optimize its capital structure given investor, tax, and accounting policy, regulatory requirements, and return on investment maximization.

All else equal it wants to tap the cheapest form of funding given a current need.

So starting with asset liability matching. Let's start with a simply case

A company has a machine that produces its product as its only asset and it will last exactly ten years and threw off a variable but basically fixed profit. The best way to fund that would be 10 bonds of 1-10 years in maturity of equal amounts. In other words a mortgage. But because the profits are variable from the machine the company needs some equity as buffer for years in which the earnings fall a little short. At the end of 10 years the mortgage is paid off. The asset is worthless and the equity has accrued cash equal to the difference between the earnings from the machine and the interest on the mortgage. Perfect asset liability matching.

So a company is not as simple but every company and its entire finance staff run by its CFO estimates its asset returns and duration of its assets ability to produce returns through their life.

In tech companies who have only IP and no current revenue all the future revenue and profit is years from now and they need to fund everything with equity. A well established manufacturing company with very certain profits can fund with debt. Banks and insurance companies own financial assets on one side of their balance sheet which they can easily liability match on the other. So the CFO staff decides what mix of debt and equity they should have based on their business mix

However all isn't equal. Lots of factors play into capital structure optimization. For instance when I started my career tax policy shifted to significantly favor debt issuance vs equity. That conflicted with historic stigma of being below investment grade rated by the rating agencies. Mike Miliken provided demand for this junk bond paper and a combination of tax policy and the relatively small increase in interest between A and BB credit convinced companies to leverage up. The white shoe corporate finance advisors advised their investment grade clients to ignore this market and perpetuated the stigma. But that simply led to LBO firms raiding these companies and loading them up with debt. Optimal capital structures changed for decades to more debt and less equity.

So times change and optimal capital structure evolve.

What also matters is the cost of various forms of capital. Keeping it simple there is corporate debt which has yield for each maturity. Cost is easy. Equity is tricky. The Classic academic theory used to calculate cost of equity is the CAPM model. In that model equities cost is equal to the risk free rate + the equity market risk premium +|- a bit more or less to compare the riskiness of a specific equity to the market.

And we enter the world of the unobservable

No one knows what these numbers are. Even the risk free rate needs a relevant maturity which itself depends on assumptions. So basically no one knows and the hack is to use historic excess returns of equities over risk free rates. Ibbotson is the gold standard for that

1/2

🦔GitHub Copilot switched to token-based billing this morning and users are already out of credits. Pro+ subscribers paying $39 a month are reporting 60% of their credits gone in two hours of normal use. One user lost 20% of their allowance from a single file review with no code changes. Another hit their monthly cap before the calendar even flipped to June.

Orgs with shared token pools have no way to see individual usage, so entire teams get cut off when one person runs a heavy prompt. Users are canceling and moving to Claude Code and Codex. GitHub community forums are on fire.

My Take

Flat-rate AI subscriptions were always subsidized. Everyone in the industry knew it. Today the subsidy ran out for a few million developers at once. The problem is a lot of companies already restructured around these tools. They cut headcount and told remaining engineers to lean on Copilot instead of building skills internally. Those companies now depend on a tool whose cost just became unpredictable and whose usefulness completely changes when you have to ration prompts to stay under budget.

The developers moving to Claude Code and Codex will hit the same wall eventually. Every AI provider faces the same unit economics. Anthropic filed its S-1 this morning, and the durability of its revenue depends on whether customers stick around once real pricing kicks in everywhere. If a $39 subscriber cancels after one day because the tool became unusable, multiply that across millions of seats and the churn risk becomes very real.

Today showed what happens when AI pricing meets reality. The companies that built their workflows around cheap tokens just discovered the tokens aren't cheap anymore and the people who knew how to do the work without them are already gone.

Hedgie🤗

While folks on this site are talking about the total of 3 equity raises that $Goog has done as if its some how rare it completely misses the point that GOOG has been handing shares out to employees who then sell to the market for its entire history. What is new is the shift from net retiring shares to issuing. Last quarter they cancelled share repurchase resulting in RSU net issuance and next quarter they will let rsu go uncovered again and issue 80BN more.

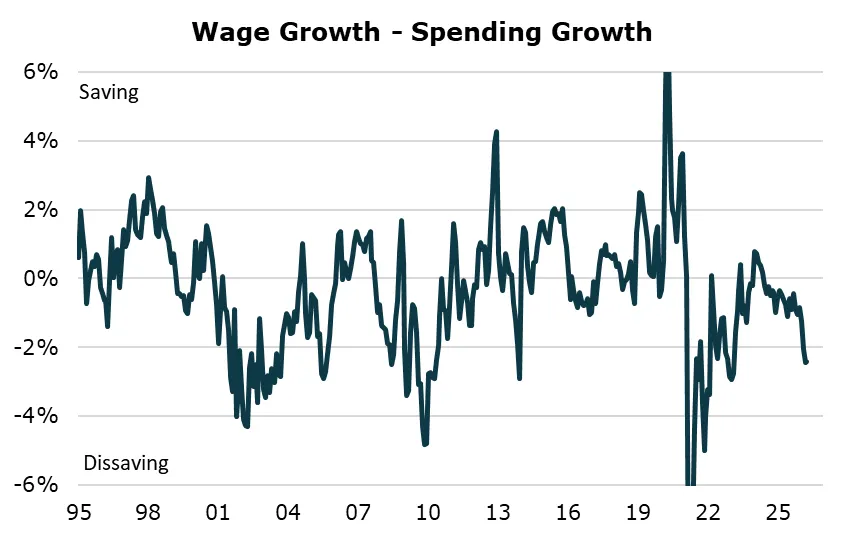

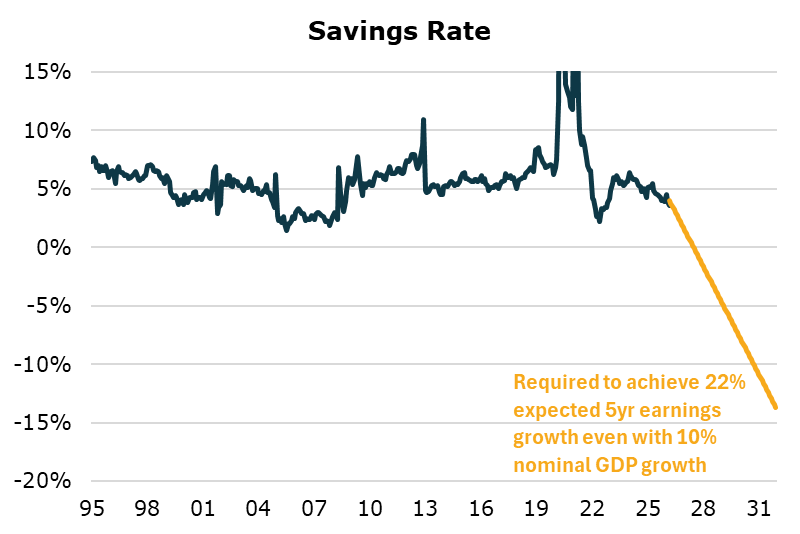

Households on A Knife's Edge

Real incomes are now contracting, but households have kept up spending so far. Without income or price relief, their choice of whether to keep dissaving will define the US economy in 2H26.

https://t.co/yj7U3lcam7

AI Mania Hopes vs. Macroeconomic Reality

Equity investors are extrapolating the recent quarters of strong earnings growth to expect the strongest 5yr earnings growth in history, requiring increasingly implausible future macro outcomes.

https://t.co/RGEbJLLics

Stealing from the future 101. This 101 will attempt to describe facts. It is not political except to say that the outcome was entirely bipartisan. It spans 46 years of a wide variety of political alignments.

The big takeaway is every single member of society has benefitted

I love AI and use it every day. However, over the past 24h in three conversations I had with C-level executives from corporates or PE the following same (!) came up on their AI initiatives:

- At the moment, it is only cost. We expect positive ROI within the next 2-3 years

- Our token cost has exploded and is x-times above budget

- We encourage and measure our staff in token consumption so they are AI ready. There is duplication in our work

- We cannot afford to not invest as the competition will and we fall behind

- We are now actively working on getting our AI cost down (eg move to open source or away from latest model within same lab)

IT sector capex as a share of S&P capex is at record highs

peak dot-com bubble: 25%

peak AI bubble: 36%

At the same time, the inputs that make all this capex possible, commodities, sit at record lows relative to the S&P.

AI infrastructure requires enormous amounts of copper, steel, aluminum, uranium, gas, and rare earths, yet capital continues to crowd into tech while starving the sectors supplying the physical backbone of the buildout.

Signs the equity lift from an Iran deal is pretty modest.

Suggests a lot more upside in bond prices & downside in oil here than upside in stocks (which already priced in the best case outcome). h/t @augurinfinity