🧵 After first learning about modern portfolio theory and construction, I settled on the typical Boglehead Three-Fund Portfolio: Total US Stock, Total International Stock, Aggregate US Bonds. Adjust stock/bond ratio to match risk.

Here are my "improvements" so far:

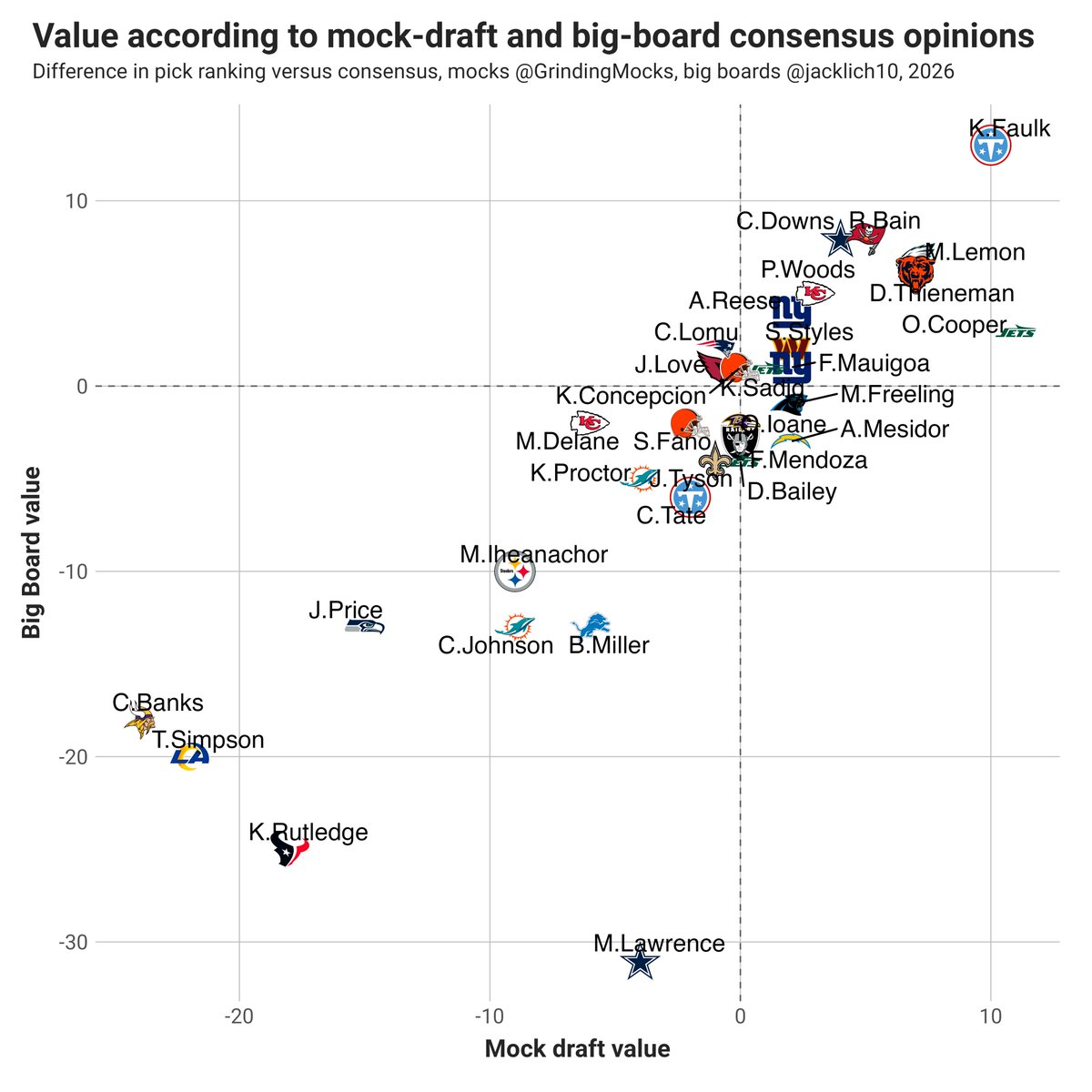

Biggest "reach" in the first round according to the consensus big board: Malachi Lawrence

By consensus mock drafts: Caleb Banks

Biggest "steal" by both metrics: Keldric Faulk

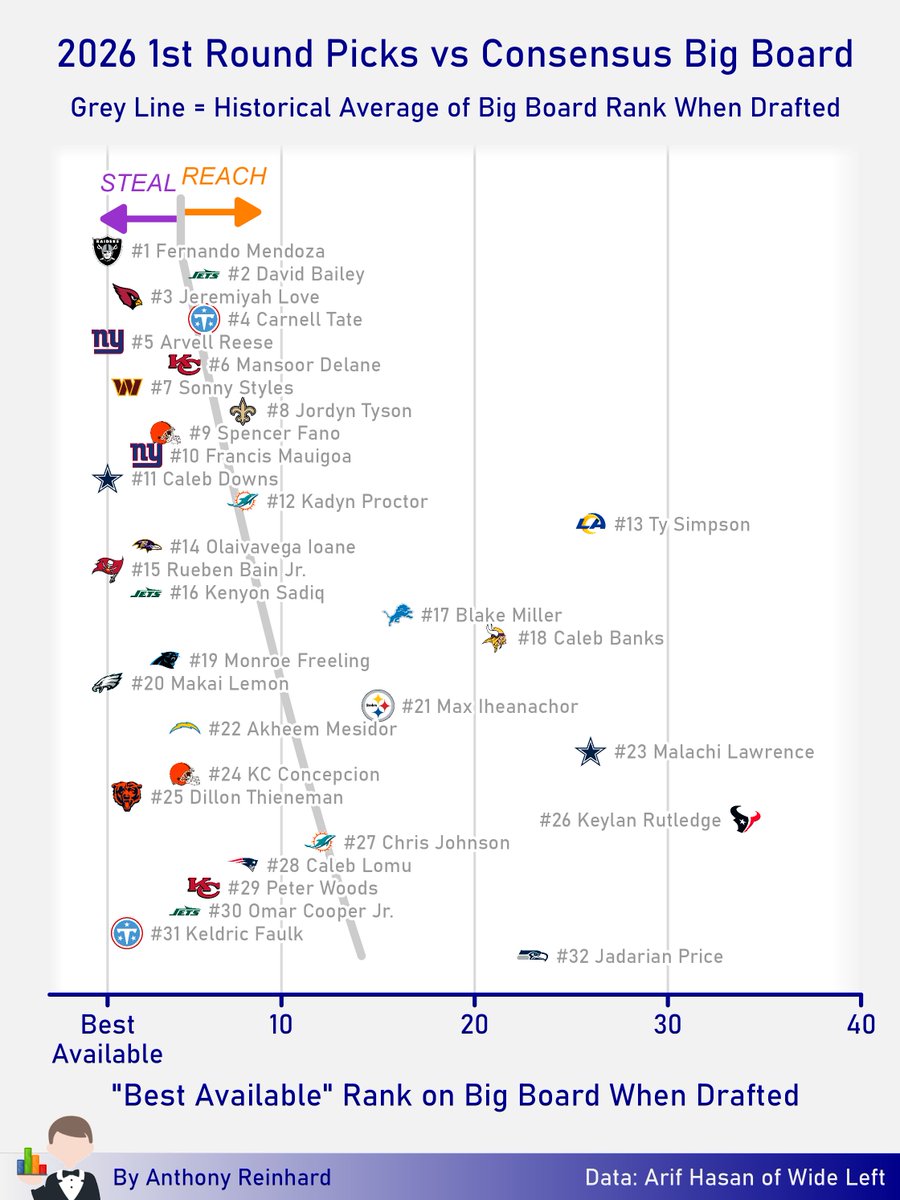

Here is where each of tonight's 1st round picks sat on @ArifHasanNFL's consensus big board at the time they were drafted. The grey line indicates the average "best available" rank from previous drafts.

@Chiefs247365 And what comes out of the organizations themselves might be even worse (smoke and mirrors, saying a whole lot to say absolutely nothing.) Although there are some guys, like Spags, whom I generally tend to take at their word.

At the time of pick No. 6, there was a 90% chance Mansoor Delane would make it to pick No. 9, per the Draft Day Predictor.

Even if that number is a little high, that's the hidden cost of trade-ups: there's a substantial chance the Chiefs gave up a 3 and a 5 for nothing!

@SamMonsonNFL Applies even moreso to announcers who *guess* what the penalty will be WHEN THE REFS ARE GOING TO ANNOUNCE THE *ACTUAL* CALL IN TWO SECONDS

Was looking out at a pond a couple minutes then heard a guy yelling behind me. I didn't think anything until hearing a growl...a pit bull literally wearing a "service animal" vest charged me.

Thankfully didn't have to bring out my knife but was assured "he is usually nice" 🙃

@michaelreynolds "Reality: Many SRI funds have outperformed traditional indexes over the past decade."

Explanation: Likely due to these funds being overweight large-cap US growth.

Sorry, I don't buy the outperformance salespoint.

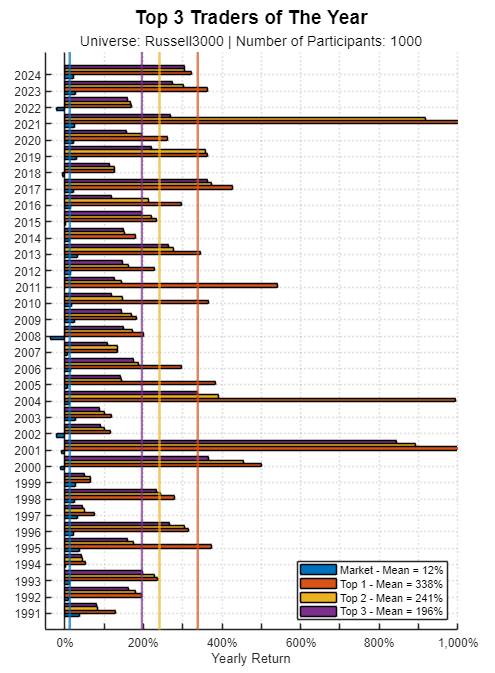

Many legendary traders are celebrated as “Market Wizards.”

But how can we tell whether an extraordinary track record truly reflects skill, or whether it could simply emerge from randomness?

To explore this question, imagine a large group of investors trading the market over many years.

Suppose none of them has any particular skill. They invest in stocks largely driven by intuition or gut feeling.

Even in such a world, probability tells us something remarkable: when enough participants are involved, a small number will inevitably end up with spectacular performance.

This observation becomes even more relevant in environments where many traders compete and are evaluated over relatively short periods of time, sometimes just a single year.

In our study, we simulate exactly this situation.

Thousands of investors start with identical conditions and trade over time with no informational advantage.

We then analyze the distribution of outcomes and focus on the traders who end up at the very top of the performance ranking.

What we find raises an important question about how we interpret exceptional track records in financial markets.

The full analysis and results of the experiment are available here.

(link in the comments)

Q—What supplement should you take for heart health?

A—None

https://t.co/TX6W1A4uha

"The American Heart Association concluded that there is not enough evidence to support the use of any supplements to prevent cardiovascular disease."

“There are no adequate data that support cardiovascular benefit for supplements in healthy people who eat a healthy diet" (—me)