Leopold Aschenbrenner's Situational Awareness fund is heavily reliant on the real AI bottleneck: power & data center infrastructure to bring massive GPU clusters online

Here are his top holdings:

$BE: 22.79%

$SNDK: 18.79%

$CRWV: 14.42%

$IREN: 10.40%

$CORZ: 10.09%

$APLD: 8.30%

$RIOT: 3.69%

$CLSK: 2.71%

Thesis in one sentence: The AI race won't be won by who has the best model, it will be won by who can bring compute online the fastest and at scale.

AI power demand is becoming one of the biggest AI Bottleneck of this decade.

Goldman Sachs predicts that power demand could surge 200% by 2030.

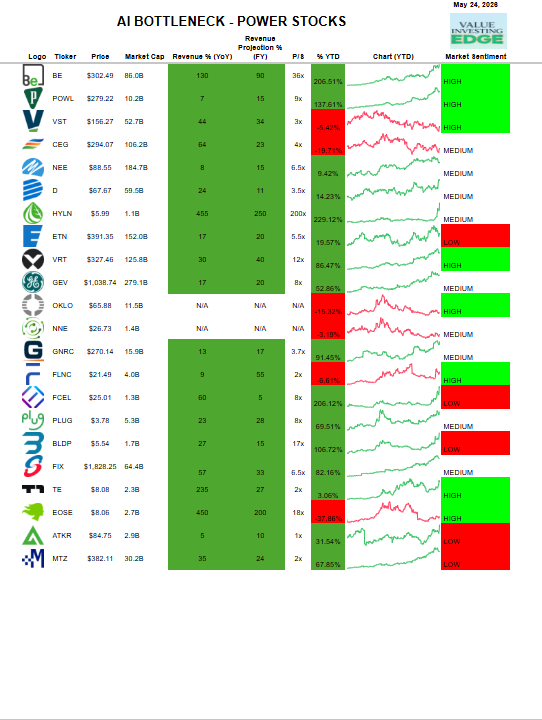

Power Generation

$VST — Vistra Corp.

$CEG — Constellation Energy

$NEE — NextEra Energy

$D — Dominion Energy

$GEV — GE Vernova

Nuclear

$OKLO — Oklo Inc.

$NNE — Nano Nuclear Energy

Grid, Electrification

$ETN — Eaton Corp.

$POWL — Powell Industries

$HUBB — Hubbell Inc.

$ATKR — Atkore Inc.

Data Center Infrastructure

$VRT — Vertiv Holdings

$FIX — Comfort Systems USA

$EME — EMCOR Group

$PWR — Quanta Services

$MTZ — MasTec

Fuel Cells / Hydrogen

$BE — Bloom Energy

$PLUG — Plug Power

$FCEL — FuelCell Energy

$BLDP — Ballard Power Systems

$HYLN — Hyliion Holdings

$GNRC — Generac Holdings

Energy Storage

$FLNC — Fluence Energy

$EOSE — Eos Energy Enterprises

Solar Energy

$TE — T1 Energy

Bookmark for research and invest in the best ones!

There is a near-perfect correlation between US oil prices and US CPI inflation, as shown in our below analysis.

Oil prices have averaged near $100/barrel since March 6th, or 79 days.

The longer this persists, the more inflation we will see.

Asset owners are the only winners.

A message for my $TSLA friends eyeing the SpaceX IPO $SPCX.

I traded $TSLA for years. I know the community. I know the excitement when Elon takes something public. But before you chase @SpaceX at $1.75 trillion, read the S-1 carefully.

SpaceX doesn't need your money.

They raised at $800B in private tenders six months ago. They could raise $50B privately tomorrow with a phone call. This IPO isn't about raising capital. It's about giving insiders liquidity.

95% of @SpaceX shares are held by insiders. Only 5% will be publicly traded. Insiders hold $1.66 trillion in paper wealth they currently can't sell. The IPO changes that.

And they've structured it so insiders can sell BEFORE the standard 180-day lock-up expires. @SpaceX built in early release provisions -- after the first earnings report, insiders can sell up to 20% of their shares.

They're also reserving 30% of IPO shares for retail. Ask yourself -- when has Wall Street ever given retail the best seats in the house unless retail was the product?

100x revenue.

$4.9B net loss.

xAI burning $6.4B a year while @Starlink subsidizes it.

This isn't 2020 Tesla at 20x revenue with a clear path to profitability. This is a different risk profile.

Now here's the part I want you to actually consider.

SpaceX's S-1 sizes their satellite-to-phone business (Starlink Mobile) at a $740 billion TAM. Their Connectivity segment does $11.4B at 63% EBITDA margins. Those numbers are real and impressive.

But buried in the S-1, @SpaceX names their D2D competitor: $ASTS .

@AST_SpaceMobile $40 billion market cap.

Not $1.75 trillion. $40 billion.

Here's what $40B buys you:

98.9 Mbps proven from space to unmodified phones (SpaceX does 3-5 Mbps)

The only low-band D2D spectrum access on Earth (indoor coverage SpaceX can't match)

All three US carriers forming a joint venture around ASTS technology

Google invested $358M

their largest public equity holding

AT&T, Verizon, Vodafone as equity investors

$3.5B cash, $1.2B contracted backlog

3,900 patents, custom ASIC in production

Three satellites launching on a Falcon 9 next month

60 carrier partners covering 3 billion subscribers

@SpaceX at $1.75T is pricing perfection across rockets, satellites, AI, and Mars. One miss and it corrects hard.

$ASTS at $40B is pricing uncertainty in a $740B market where the technology is already proven and the carriers have already chosen sides.

The Tesla community knows what it feels like to find a mispriced stock before the world catches on. $TSLA at $30 pre-split wasn't obvious to anyone except the people who did the work.

$ASTS at $106 in a $740B market with 33x faster speeds than SpaceX D2D, a carrier JV, and institutional discovery just beginning -- that's the same kind of setup.

So before you throw money at a $1.75T IPO where insiders are building exit ramps, maybe look at the $40B competitor they named in their own filing.

Not financial advice. Just math.

$ASTS 🛰️

cc @SawyerMerritt@unusual_whales@DanBTC916

chainlink CCIP absorbed $4b in assets from layerzero in 60 days after their vulnerability disclosure. kelp DAO moved $1.2b, lombard $800m, kraken moved their entire bridge infra. zero CCIP exploits since launch vs $2.8b stolen from competing bridges. SGX just adopted chainlink for OTC FX settlement in the world's 3rd largest FX market. LINK sits at $6.8b market cap securing $110b in value. the cross-chain infrastructure war ended and most people were looking at shitters when it happened

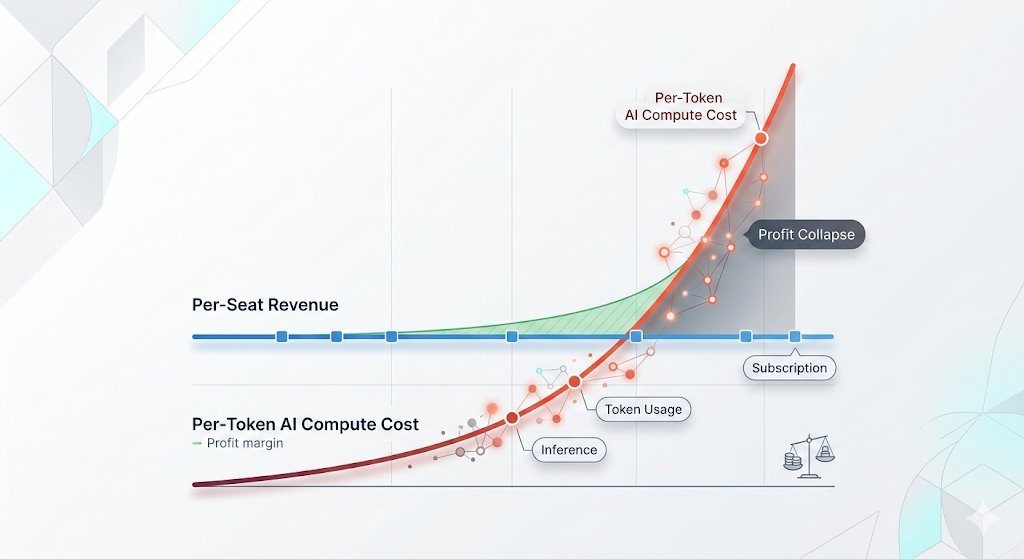

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

8 undervalued stocks Leopold Aschenbrenner is signaling you to buy through his latest 13F reports. It is not $BE, $MU, or $NVDA, but:

• $HIVE — HIVE Digital

• $RIOT — Riot Platforms

• $TE — T1 Energy

• $APLD — Applied Digital

• $IREN — IREN Limited

• $BTDR — Bitdeer Technologies

• $KEEL — Keel Holdings

• $CLSK — CleanSpark

These stocks are all undervalued, with massive potential to create generational wealth.

Not financial advice. Do your own research.

DTCC processes $2.5 quadrillion annually and just named ondo as a tokenization partner for July production launch on Canton Network. $4.6 trillion in daily repo volume moving to atomic settlement. clearstream integration bridges european custody (€16T AUC) into the same pipe. CLARITY Act cleared senate banking 15-9 two weeks ago. october full production opens access to 3,600+ DTCC member firms. the entire thesis breaks if DTCC decides to build tokenization in-house, but the coalition they assembled (goldman, BNY mellon, moody's, microsoft) suggests they chose the partner route. ondo already runs $600m in tokenized treasuries. that number looks small until you realize the rails it sits on are about to connect to the largest settlement system on earth

kraken went exclusive chainlink CCIP for all current and future wrapped assets. $4b+ migrated from layerzero in 48 hours after the $292m kelp exploit. ZRO dropped 20%+ on the exodus. the part that compounds: every protocol that wants kraken integration now has to build on CCIP. 47% of layerzero OApps were running the same 1-of-1 DVN config that got drained. 94% admin key overlap between layerzero labs and nethermind DVNs. production multisig keys were being used for shitter trading and LP provisioning. the bridge market just split into two tiers in a single weekend and the institutional tier has one provider

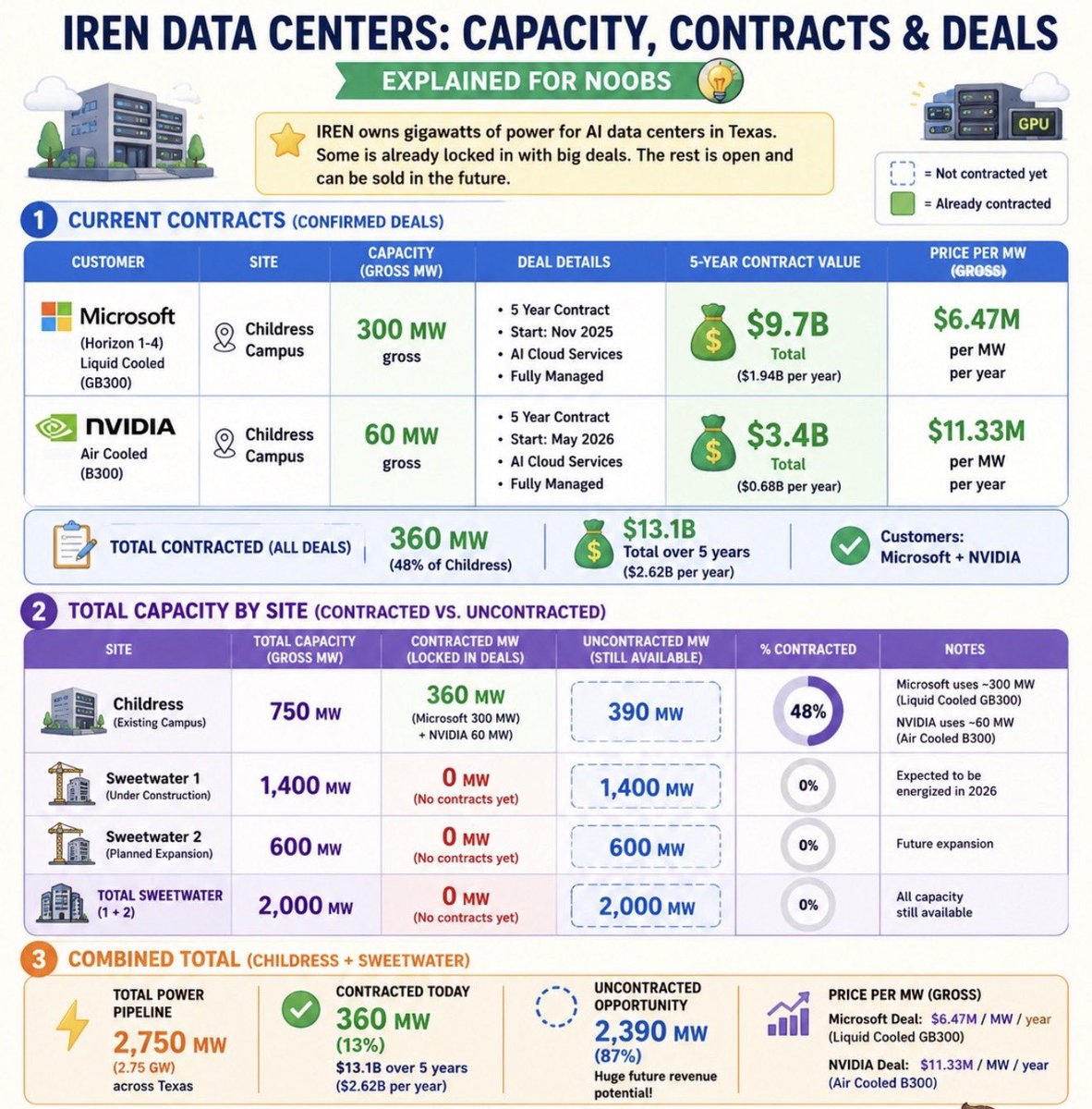

$IREN : Ran some numbers on Saturday Napkin Math.

$IREN math is getting WILD 👀

Already signed:

• Microsoft = 300 MW → $9.7B

• NVIDIA = 60 MW → $3.4B

That’s:

• 360 MW contracted

• $13.1B total value

• $2.62B annualized revenue

BUT…

Childress still has:

• 390 MW UNSOLD

If future AI-cloud pricing improves:

• another ~$15B+ possible

• ~$3.8 - 4.5B/yr potential

Then add:

• Sweetwater 1 = 1.4 GW open capacity

At current AI infra pricing:

• ~$12–18B/yr possible from SW1 alone

Total potential 2027 🤯 for 750 + 1400 MW = 2.15 GW

• ~$15–22B+/yr revenue opportunity WOW.

They have total 5 GW so still has 2.8 GW, this is insane opportunity.

I swear this guy does NOT miss. Incredible.

This is getting insane... $VELO up 40% in two days since this mf'er bought, $LUNR up 48%, $NBIS up 51%, etc.

Just buy what he buys and you'll beat the markets lol.

Okay folks, this qualifies as BREAKING NEWS!

Harold “Sonny” White, the warp drive pioneer behind NASA’s EagleWorks Lab, just stepped out of stealth with Casimir Inc. to unveil MicroSPARC: the first battery free chip to harvest continuous electrical power straight from the quantum vacuum via the Casimir force.

The 5 mm × 5 mm device uses millions of custom microscale Casimir cavities fabricated on a substrate. Inside each cavity, two fixed conductive walls create a region of negative vacuum pressure (the well known Casimir effect). Stationary micropillars anchored in the middle act as antennas. Electrons from the cavity walls then quantum tunnel to the pillars because the interior is a lower energy “quieter” zone — and the probability of tunneling back is orders of magnitude lower. This one way “quantum ratchet” flow generates a measurable DC current with no external power source or moving parts.

Prototypes already fabricated at university nanofab facilities (Texas A&M AggieFab, MIT.nano) have been tested in RF-shielded, low noise chambers for weeks. The team reports outputs ranging from millivolts to volts at picoamp to microamp levels using precision electrometers and Kelvin Probe Force Microscopy. Target performance for the first commercial chip: ~1.5 V at 25 µA (≈40 µW continuous). Stacking and scaling could reach milliwatts or even watts per device.

Initial applications are ultra low power: always on IoT sensors, wearables, and medical implants. Longer term roadmap includes trickle charging phones, powering small electronics, and eventually grid independent homes or EVs. Commercialization is targeted for 2028, starting at ~$100/W before dropping toward $10/W.

White ties the work directly to his earlier theoretical paper on emergent quantization from a dynamic vacuum and sees it as a practical power source for the deep-space missions he’s long championed.

Extraordinary claims require extraordinary evidence, and independent scientists have so far declined public comment. But if the engineering scales as hoped, MicroSPARC would represent a genuine paradigm shift: continuous, maintenance free power drawn from the fabric of spacetime itself.

A bold leap from warp-drive theory into real hardware. Progress (and vacuum-powered chips) marches on.

Photo: MicroSPARC | Casimir Inc.

Source: https://t.co/11tlwNSf71

LLM hallucinations are a massive roadblock to enterprise adoption of AI.

Swift, UBS, Euroclear, & 20+ major organizations advanced a solution to the $58B+ annual corporate actions problem by leveraging Chainlink to reduce AI hallucination risk.

LINK everything.

$LINK at $10

Most mispriced asset in the world.

2030 base bull target: $221,926

Not a typo

The math:

• DTCC + 8 institutional partners

• $184T of value secured

• 15% stake floor on slashable LINK

• 55% of supply locked operationally

• Reserve absorbs 50% of fees

• Float collapses from 727M to 357M

• Multi-chain network coefficient (50+ chains)

• Replacement-cost premium (embedded infrastructure)

Value capture isn’t from fees. It’s from required collateral.

When a network secures $184T of institutional value, every dollar of that needs slashable $LINK behind it.

Strong bull: $288K

Hyper bull: $355K

👇👇👇👇👇👇👇

Why value capture works this way

Oracle networks aren’t priced like fee businesses. They’re priced like collateralized infrastructure.

#Chainlink securing $184T means ~$27T of slashable LINK has to back it. With float collapsing to 357M, the stake floor alone clears north of $75K. Add P/S on $46B in fees, multi-chain network effects, and the premium institutions pay for systems they can’t switch off — you land at six figures.

This isn’t speculation. It’s what happens when a token becomes the collateral for global finance. Visa trades on irreplaceability, not fees. LINK is the same trade — except supply is fixed and float is shrinking.

The market still sees a crypto. By 2030, it’s the bond posted against tokenized capital markets.

🚨 Anthropic just showed a 24-minute workshop on how to actually do prompts for Claude.

Taught by the people who built it.

Free. No registration. No paywall.

I've seen $300 courses that don't cover what they teach in the first 8 minutes.

Watch it and bookmark it now.

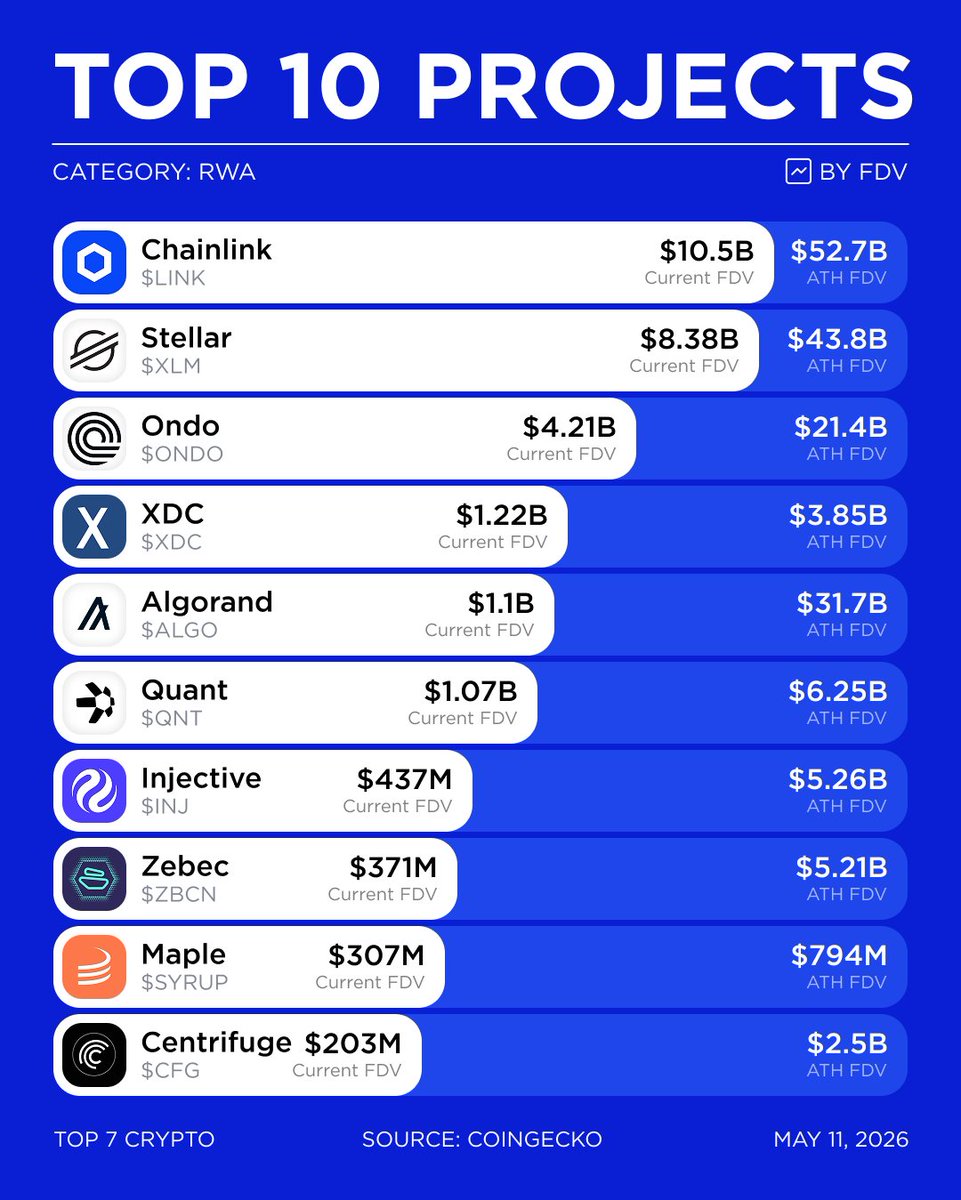

Top 10 Real World Assets Projects by FDV

RWA projects are pushing tokenized assets into the mainstream, connecting traditional finance with on-chain infrastructure. Here are the top 10 projects driving the narrative.

$LINK $XLM $ONDO $XDC $ALGO $QNT $INJ $ZBCN $SYRUP $CFG

Data source 🔗 @coingecko

amazon launched agentcore payments on may 8 routing AI agent transactions through x402 in USDC on base. 161k monthly active agents, up 669% month over month, $100m+ in Q1 volume. the part that matters for positioning: chainlink's payment abstraction layer converts enterprise fiat payments into LINK and deposits them into the chainlink reserve automatically. every dollar an AI agent spends through x402 creates programmatic LINK accumulation. chainlink already pulling $39.64m in annual oracle fees. now there's a second structural demand vector scaling with agent commerce volume that has amazon, mastercard, and coinbase backing it through the linux foundation. LINK has a treasury accumulation mechanism disguised as payments infrastructure.

WHO'S STILL HOLDING $LINK RIGHT NOW? 👇

Because the gap between what this protocol delivers and what the market pays for it has never been wider.

🟢$30 trillion in total value enabled.

🟢More than U.S. GDP.

🟢Seven years. Zero exploits.

And the token? still sits at $9.

Swift chose Chainlink. DTCC chose Chainlink. Euroclear chose Chainlink. JP Morgan chose Chainlink. Mastercard chose Chainlink. Fidelity International chose Chainlink. UBS chose Chainlink. The Central Bank of Brazil chose Chainlink. SBI chose Chainlink.

These aren't speculative partnerships. These are the institutions that clear, settle, and move the world's capital.

And they all independently arrived at the same infrastructure layer.

CCIP weekly volume just surged 260% to $1.3B. Record exchange outflows. 970K LINK pulled off exchanges in one day. ETF inflows past $111M.

Whale wallets holding 1M+ grew 25% in the past year.

Amundi, Europe's largest asset manager, launched a Chainlink-powered tokenized fund that hit $400M in three weeks.

Coinbase is pushing exchange data on-chain through Chainlink's DataLink.

The U.S. Department of Commerce uses Chainlink oracles for GDP and inflation data.

SEC and CFTC classified LINK as a digital commodity. Chainlink's deputy general counsel sits on the SEC's Crypto Task Force.

The protocol that powers 65%+ of all DeFi oracle services, connects the world's largest financial institutions to blockchain, and just crossed $30T in value enabled trades at $9.

If you're still holding, you see what the price doesn't show yet.

The fundamentals aren't waiting for the market to catch up. They're compounding regardless.

HODL! 💎

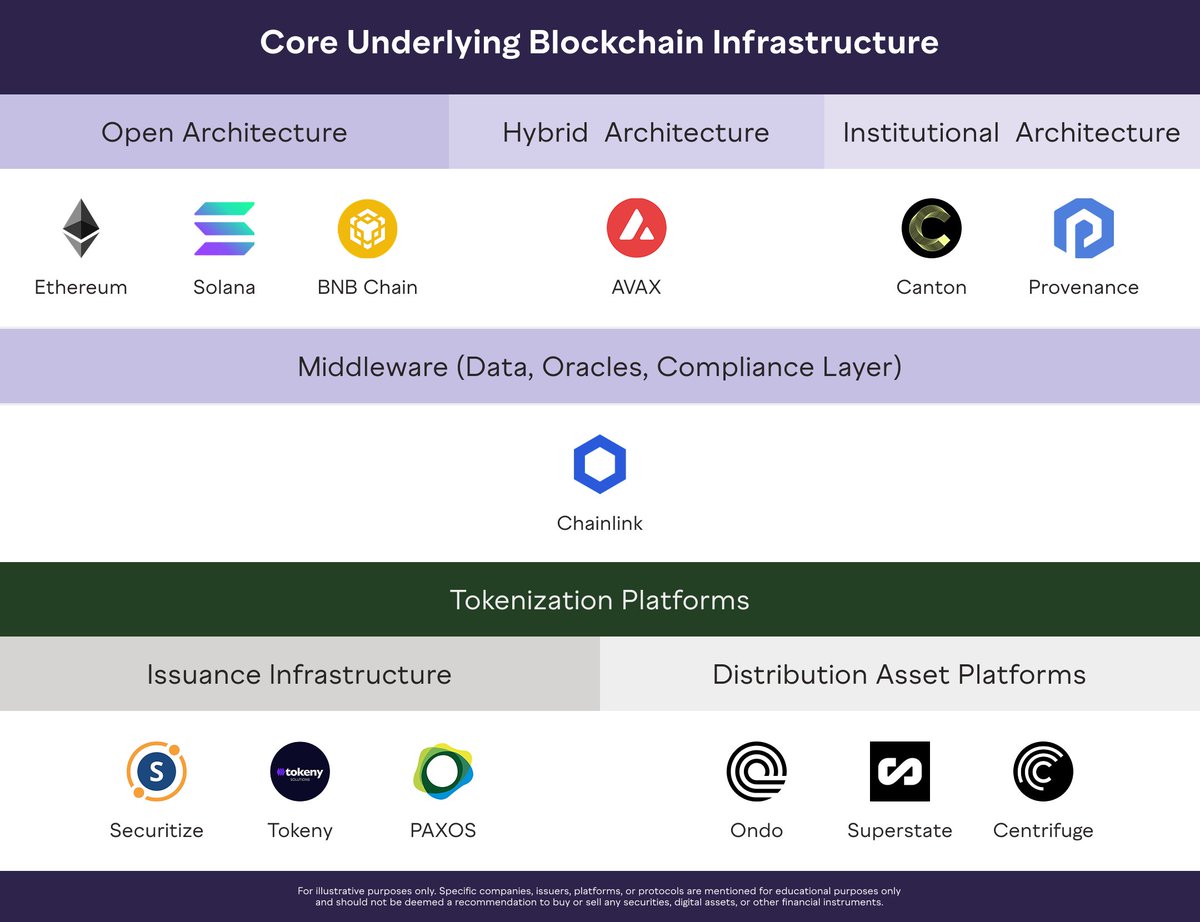

1/ Tokenization is poised to transform capital markets

Grayscale Research believes $ETH $SOL $CC $BNB $AVAX $LINK are well positioned to benefit from more than $300T+ in assets moving onchain 🧵↓