This will be looked at as one of the biggest head fakes in the history of markets.

Correct, right in line with the four-year cycle, during Q4 of 2025, to get the majority to think it's still valid, then completely front-run it as the macro aligns with the business cycle while the masses wait for their beloved 2028 halving event.

It's masterful. The amount of capital that will be left sidelined and chasing will be historic.

This has been my thesis for quite some time.

Prediction: On June 18th $VIX will be at $14 and $SPY at $780 and the Monday after the 3 day weekend it'll open down 2% marking a substantial pullback week with some big news that ends the gamma squeeze and leads to an elevator down kind of week.

$BTC has spent nearly 9 years inside this rising channel - and I don't think that changes anytime soon.

If we get a dip closer to the lows of the channel in the coming months, you best believe I'll be loading up the truck. 🚛

In a hyperinflationary environment, the single most important financial decision you can make, and the one almost nobody who lives through one is psychologically prepared to make, is to maximize fixed-rate, long-duration debt against productive assets, because the entire mechanism of hyperinflation is a wealth transfer from creditors to debtors, and the only question that matters, in the moment it begins, is which side of that transfer you have positioned yourself on.

The math is brutal in its simplicity. If you owe a bank $400,000 at a 30-year fixed rate of 6%, and the currency loses 90% of its purchasing power over five years, you are, in real terms, paying back the bank in lottery tickets. The house you bought with that loan retains its real value, because it is a physical asset that the inflation cannot touch. The bank, which lent you future dollars and is now receiving past dollars, takes the loss. You take the gain. The transfer happens silently, invisibly, on the loan amortization schedule, every single month, while the people around you who saved in cash, held bonds, or refused on principle to take on debt watch their lifetime savings evaporate in real time.

The Weimar industrialists who emerged from 1923 with their fortunes intact, and in many cases multiplied, were not the ones who hoarded gold or moved their assets to Switzerland. They were the ones who borrowed aggressively, in the local currency, at fixed rates, against factories and farms and apartment buildings, and let the inflation pay off the debt while they collected rents and revenues that repriced upward with the currency. The same pattern played out in Hungary in 1946, in Argentina in the 1980s, in Zimbabwe in 2008, and in every other major inflation event of the modern era. The borrowers won. The savers lost. The people in the middle, who tried to be cautious and hold cash and wait for clarity, were the ones whose lives were quietly destroyed.

The reason almost nobody acts on this knowledge in advance is that the human brain treats debt as danger, and treats saving as safety, and these instincts are correct in stable monetary environments and exactly inverted in unstable ones. The middle class, which has been trained for generations to fear debt, is structurally the worst-positioned group when the currency starts to fail. The wealthy, who use leverage as a tool, and who hold the productive assets that the leverage was used to acquire, are structurally the best-positioned. The asymmetry is not an accident. It is the entire mechanism by which monetary debasement transfers wealth from one class to another, every time it has happened, in every country it has happened in, for as long as currencies have existed.

You do not need to predict the timing. You need to structure your balance sheet, in the years before the event, in a way that benefits if it arrives. Fixed rate, long duration, productive assets. The trade has worked for 400 years. It will work for the next 400. Almost nobody will run it, because almost nobody is willing to be the person who took on debt while everyone they know was paying theirs down, which is, as it has always been, the entire reason the people who do run it end up owning everything on the other side.

We are now in the parabolic, melt-up phase. Where and when it peaks is anyone's guess. It's also the exit phase, not enter. Just remember, it's better to be a year too early, than a day too late.

If you bought the S&P in late 2024 betting on 8-10% returns, you're about to lose a decade of your financial life.

Billionaire investor Howard Marks on the JP Morgan chart everyone's ignoring:

At the end of 2024, the S&P was at a P/E of 23. Historically, every single time the market hits a P/E of 23, the next 10 years returned between 2% and -2% annualized.

NO exceptions.

What this means: if you invested $100K at the end of 2024, by 2034 you'll have between $82K and $122K.

Best case (2% annualized): you barely beat inflation

Worst case (-2% annualized): you lose 18% of your money

Either way, high-yield savings beats your "aggressive" portfolio

This isn't a bearish prediction. It's a historical certainty based on the price you chose to pay.

@thesamparr@ShaanVP

Ben Felix reveals the 5% rule for deciding whether to rent or buy a home

"You account for all of those unrecoverable costs the owner has, and the renter investing in the stock market and investing the cost difference"

"What you'll find looking at expected stock returns and expected real estate appreciation, you can very easily show that there is an equivalence. There is a level of rent where you are indifferent between renting and owning"

"If you divide the price of a home by 5% and then divide that number by 12, you will get the monthly rent that is equivalent to the unrecoverable cost of owning that home"

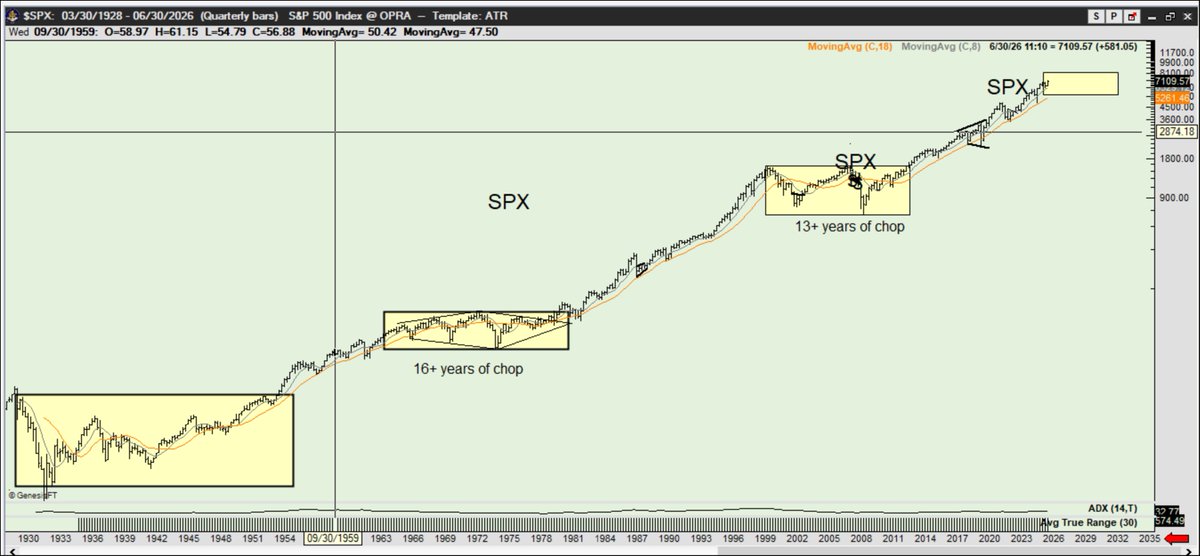

U.S. equity investors -- get ready for five to ten years of chop suey

During the past 100 years the S&P index chopped sideways for 54 years. That is 46 years of no new net gain (other than from dividends)

S&P Index is entering another major period of chop $SPX

When you get the email: "We are thrilled to offer you the role. The base salary is $85,000." (And you know the market rate is $120k).

USE THE GOLDEN COUNTER-OFFER:

People will go to college for 4-6 years to work a job they hate for 40 years and those same people will quit trading if they don’t get rich inside of year 1.

If you truly want it then just show up everyday and it will happen for you when it is meant to happen.

Never quit!

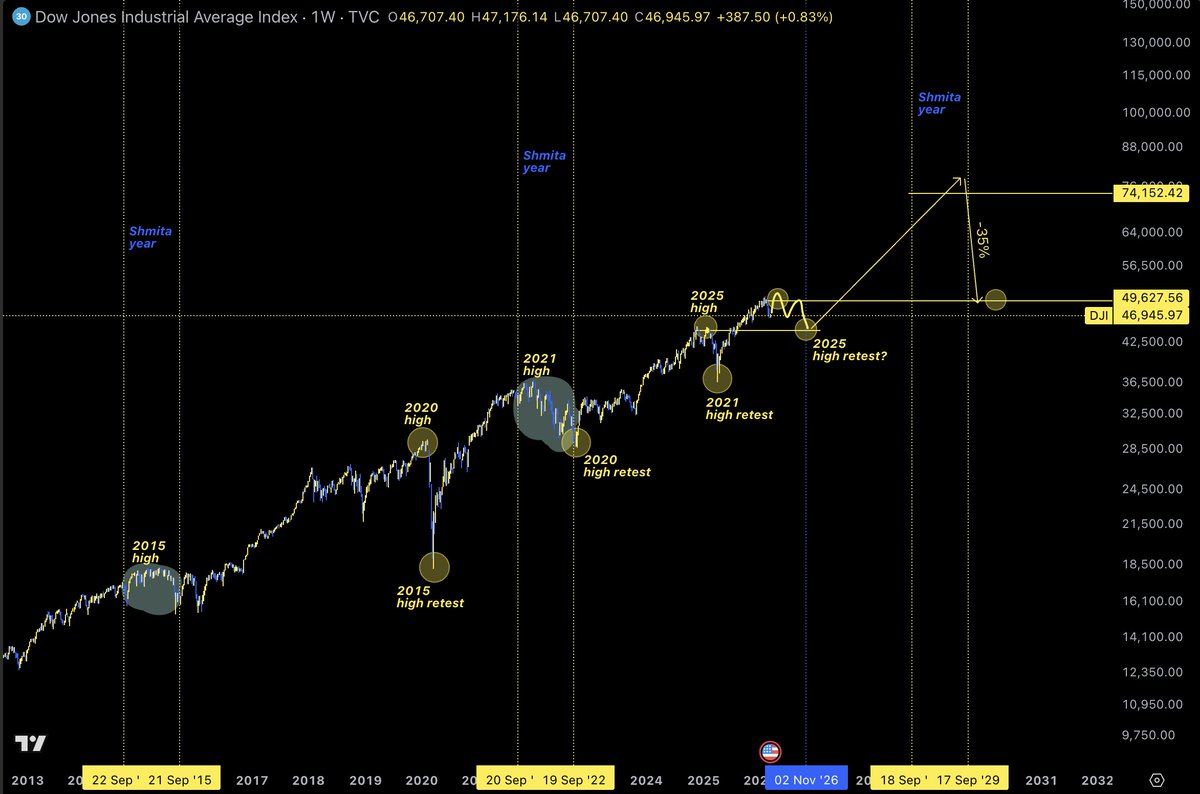

$DJI -35% discount

If yields fail to collapse this year, and they just continue to trend (even to the downside), then we could only see a test of the 2025 highs, with continuation up into the next Shmita year

So if it doesn't happen this year, in a mid-term year, then in 2027 it most likely doesn't happen, in 2028 chances become more likely, by 2029 they become most likely

But the secular cycle continues up. It's a game of liquidity.

Follow it, I post for free every 2 days:

https://t.co/JunKkMQ8kl