Strait of Hormuz over the last 24 hours.

Interesting traffic flow in the Southern lane.

No visible movements since IRGC announced closure. It could be dark transits, I will report back tomorrow.

Source: @MarineTraffic

$ASTS Interesting if true...

ULA Vulcan mission carrying 5 AST BlueBird Block 2 satellites. No public confirmation from AST or ULA that I've seen. But if AST is potentially reserving Vulcan capacity, that would suggest deployment plans are far more aggressive than many realize 🚀

Come along for a deep dive in reading between the lines. And in the documents not made public.

We’ll be discussing SDA futures program. And how $ASTS is affected.

🐈⬛ CatSE: ”The smoking gun of a upcoming Golden Dome contract in plain sight”

1/n

$ASTS J-LEO update: End-of-June "winner selection" is only an internal estimate (subject to change). Preliminary notice to winner is private. Official public announcement comes only after final Grant Approval Notice — expected mid-July to mid-August 2026.

Credit to @ayano_kova for sharing the link to the J-LEO project details. Highly recommended to follow her for her detailed articles on Japanese Space programs & advancements.

You can read her article on J-LEO Project here -->

https://t.co/tN6pwhMshN

🤖🇫🇷 𝗡𝗶𝗰𝗲 𝗲𝘀𝘁 𝗲𝗻 𝗽𝗮𝘀𝘀𝗲 𝗱𝗲 𝗱𝗲𝘃𝗲𝗻𝗶𝗿 𝗹𝗲 𝗻𝗼𝘂𝘃𝗲𝗮𝘂 𝗰𝗲𝗻𝘁𝗿𝗲 𝗻𝗲́𝘃𝗿𝗮𝗹𝗴𝗶𝗾𝘂𝗲 𝗱𝗲 𝗹𝗮 𝗱𝗲́𝗳𝗲𝗻𝘀𝗲 𝗲𝗻 𝗘𝘂𝗿𝗼𝗽𝗲 𝗽𝗼𝘂𝗿 𝗹𝗲𝘀 𝗜𝗔 𝗮𝘂𝘁𝗼𝘂𝗿 𝗱𝗲 𝗹𝗮 𝗹𝘂𝘁𝘁𝗲 𝗮𝗻𝘁𝗶-𝗱𝗿𝗼𝗻𝗲𝘀 𝗮𝘃𝗲𝗰 𝗹’𝗶𝗻𝘀𝘁𝗮𝗹𝗹𝗮𝘁𝗶𝗼𝗻 𝗱𝘂 𝘀𝗶𝗲̀𝗴𝗲 𝘀𝗼𝗰𝗶𝗮𝗹 𝗱𝗲 𝗠𝗔𝗥𝗦𝗦

La bataille contre les drones se joue désormais autant dans les logiciels que dans les missiles.

Le groupe australien EOS vient d’annoncer plus de 10 millions d’euros d’investissement à Nice pour y installer son centre européen dédié à l’intelligence artificielle de défense et à la lutte anti-drones.

Derrière cette décision se cache l’acquisition de MARSS, une entreprise fondée à Monaco qui a développé NiDAR, l’un des systèmes de commandement et de contrôle les plus avancés du marché, déjà déployé sur plus de 60 sites à travers le monde.

À la clé : jusqu’à 150 emplois hautement qualifiés, un renforcement de l’écosystème de Sophia Antipolis et une nouvelle preuve que la France attire de plus en plus d’acteurs internationaux de la défense de haute technologie.

Dans notre article, on vous explique pourquoi EOS a choisi Nice plutôt que Paris ou Toulouse, comment fonctionne la plateforme NiDAR capable de réduire les temps de réaction de plusieurs minutes à quelques secondes, ce que représente réellement le marché anti-drones aujourd’hui, et pourquoi cette implantation pourrait renforcer la souveraineté technologique européenne face aux solutions américaines.

Notre article complet :

👉 https://t.co/30eXxAWaV6

#Défense #Drones #IA #Innovation #france #armee

$QS The biggest takeaway isn’t just that Honda signed an agreement with QuantumScape.

It’s that Honda spent years evaluating the technology before moving forward. Global automakers don’t commit engineering resources and R&D budgets without extensive testing.

What’s even more interesting is Honda’s comment that QuantumScape’s batteries could add value across “a range of applications,” not just electric vehicles. That opens the door to future opportunities in robotics, AI infrastructure, industrial equipment, and energy storage.

One partnership doesn’t guarantee commercial success, but it does provide third-party validation from one of the world’s most respected engineering companies.

For long-term investors, that’s often more meaningful than hype or speculation.

Strait of Hormuz over the last 24 hours.

@WindwardAI counts 26 tankers.

It is evident that IRGC continues to throttle traffic flow.

Maybe I was optimistic in assuming 30-40. Let's see.

Source: @MarineTraffic

$QS Exactly. Honda $HMC isn’t entering a multi-year industrialization and technology transfer agreement with QuantumScape for charity. Honda has spent years developing its own all-solid-state battery technology, invested heavily in dedicated pilot manufacturing, and conducted extensive internal R&D. After evaluating QuantumScape’s cells and manufacturing approach, and seeing that the ceramic separator engineering solved their problems, Honda decided the technology offered compelling enough advantages to move forward with a formal development and IP transfer partnership. That’s about as strong a validation as investors can ask for from one of the world’s most sophisticated battery and automotive companies.

We now have Volkswagen Group and all of its brands, plus Honda, standing behind what appears to be the leading solid-state battery technology. Honda evaluated the landscape and selected QuantumScape for a multi-year industrialization effort. The significance of that decision is only beginning to be appreciated.

Eagle Line is operational. The Cobra separator process has been demonstrated to partners. IP transfer hiring is underway. Volkswagen has stated the technology is expected to reach limited premium vehicle deployment before broader scaling over the next several years. The path toward commercialization continues to take shape.

QuantumScape is also expanding its focus beyond passenger vehicles. CEO Siva Sivaram has repeatedly highlighted AI data centers as a major opportunity. The company launched its “Powering the AI Factory” initiative and recently appointed a dedicated VP/GM of Data Centers. Data center, grid, and energy storage partnerships are becoming an increasingly important part of the story.

Management has indicated that additional OEM relationships remain undisclosed, including a pure-play EV manufacturer. Nissan remains a possibility. $TSLA Tesla remains a possibility as well, particularly given JB Straubel’s involvement with QuantumScape and his deep experience across EVs, energy storage, and AI infrastructure.

Honda’s decision adds to a growing list of industrial validations. Multiple global OEMs have spent years evaluating solid-state battery technologies and QuantumScape continues to attract some of the largest and most sophisticated partners in the industry.

Additional OEM announcements, industrialization milestones, AI infrastructure opportunities, production ramps, and new market applications all sit ahead.

The low-price accumulation window for $QS will start to close.

$QS Reverse-Engineering QuantumScape's OEM List, and Why the Data Keeps Pointing at $TSLA Tesla, Nissan, and $F Ford

Yesterday, QuantumScape ($QS) confirmed a multi-year joint agreement with $HMC Honda R&D covering both solid-state research and manufacturing, following Honda's completion of a technology evaluation that QS's CEO called one of the most rigorous assessments of its technology to date. That's the second major OEM after Volkswagen.

Here's the part worth sitting with: the geolocation data called Honda well before the press release. A while back, a redditor pulled mobile ad ID (MAID) data to map foot-traffic between QuantumScape's facility and OEM R&D sites, basically legal espionage, believe it or not! Honda R&D Palo Alto lit up as one of the strongest bi-directional signals in the set (4.71). Yesterday it became official.

So the method just got validated. VW was always public knowledge; Honda was not, until recently, though many of us found obvious clues (like the fact that Honda needed a ceramic separator process and they were stuck on it). That track record is the reason to take the rest of the list seriously.

Confirmed:

VW Group ($VWAGY) ✅

Honda ($HMC) ✅ (new, as of yesterday)

Here's where the same data plus public breadcrumbs point next.

Nissan ($NSANY). Spotted at the Eagle Line event and featured in shareholder materials, with a strong engagement correlation in the geolocation set (Nissan R&D Palo Alto to QS Factory, score 2.11). High confidence. Remember, Nissan is platform sharing so we are talking about Renault–Nissan (Infiniti)–Mitsubishi brands also.

Tesla ($TSLA). This is the one that lights up. Tesla HQ is the single strongest connection in the entire dataset (8.34), with Tesla Kato Road adding a second bi-directional signal (2.37). Tesla co-founder JB Straubel sits on the board, now on the strategic board. Tesla is very likely the "pure-play" EV OEM working with QS.

Ford ($F). The most likely other OEM. The Ford and Solid Power ($SLDP) JDA has been wound down. Solid Power's 2025 10-K states that, effective Dec 31, 2025, the companies amended the JDA "in connection with the winding up" of their cell-development work and extended it only through March 31, 2026. A freed-up Ford plus a 6.55 bi-directional geolocation score with QS (strong in both directions) is hard to ignore. Ford clearly does not see future value in Solid Power's SSB technology, which is well known to be inferior to QS's.

Wild card: Rivian ($RIVN). Closely aligned with VW Group, which holds a direct equity stake in Rivian and has committed up to $5.8 billion through 2027, including a 50/50 joint venture, Rivian and VW Group Technology. That JV is built around software and zonal electrical architecture rather than batteries, so a QS-to-Rivian battery path would be a separate step, but the depth of VW's involvement is why Rivian stays on the radar at all. The base case is that QS could reach Rivian via the VW vector regardless, though the data leans Tesla as the standalone EV name here, not Rivian.

One more data point, and it comes from Factorial's own lead OEM (thanks to @Defiantclient2 for finding it). Mercedes-Benz's infographic for the 1,205 km Stuttgart-to-Malmö drive lists a pneumatic cell support system holding a constant 28 bar as a feature of the Factorial-cell EQS ($FAC). An active pressurized-air system at a constant 28 bar is not something you fit into a motorcycle or a cost-sensitive mass-market pack. Contrast that with QuantumScape, which ran its anode-free QSE-5 cells in a Ducati V21L at IAA Munich, a bike with no room for a pneumatic rig, precisely because its ceramic separator is built to operate at comparatively low external pressure. All roads keep confirming what the thesis laid out a long time ago.

If I'm wrong, I'll own it. But this looks like the OEM list.

I've NEVER BEEN MORE BULLISH $QS 🚀🚀🚀🚀

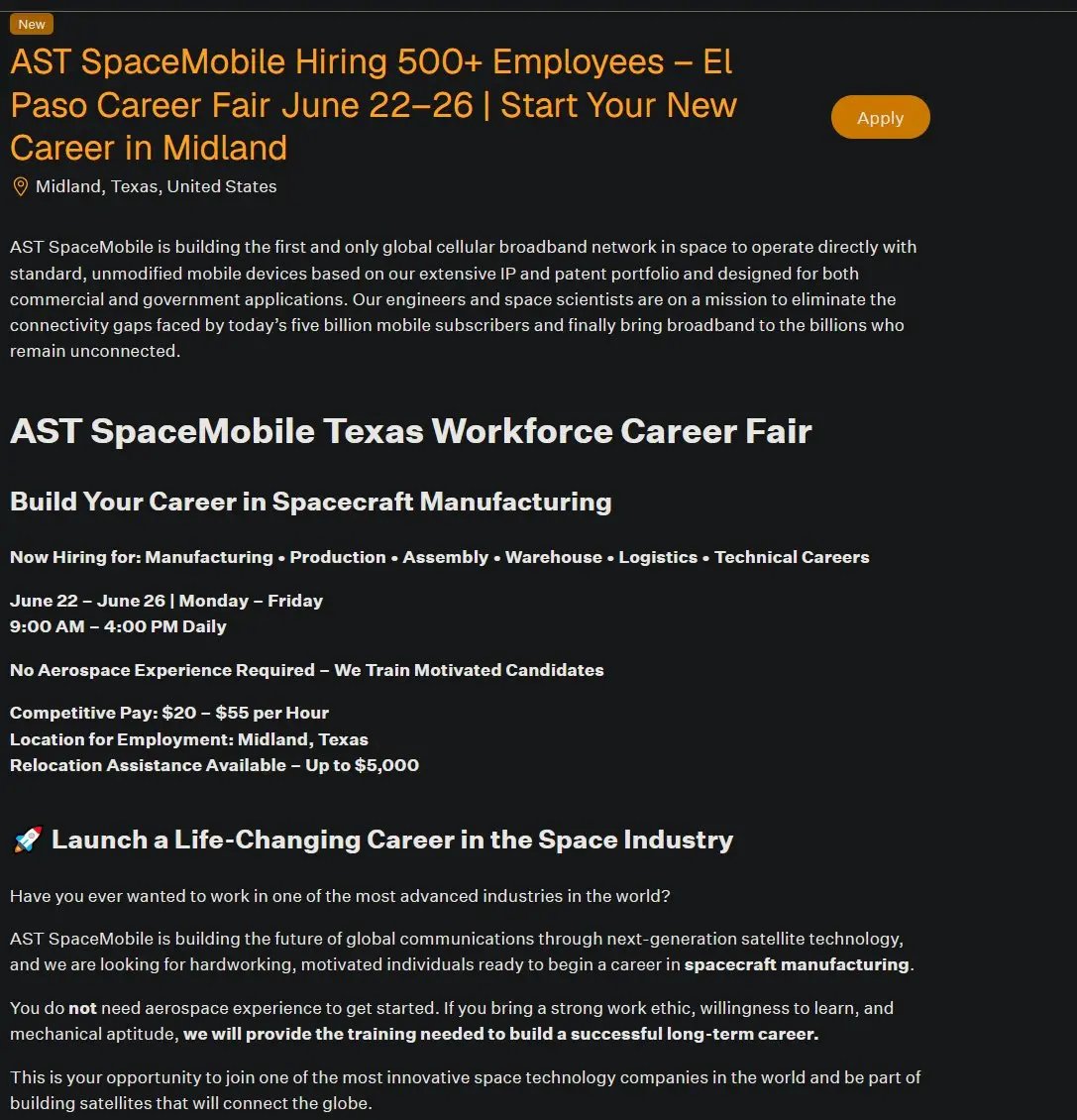

$ASTS - AST has 224 job openings at the moment. They are going to have a job fair seeking 500+ employees.

I'm not implying that the below video of Scott Wisniewski at the JP Morgan conference is related to this, but I’m also not saying it isn't.

Il a répondu dans le webinaire sur les 2 premiers points ensuite le 3e on peut extrapoler en cumulant les réponses de Joe Church datant du 6 Mai 2026 et le document de réponse.

1. 0 due diligence, il l'a fait pour aider Joe qui était client et qui avait un projet intéressant "Buffalo Green Data" avec un expert dans l'IT. Il l'a aidé à trouver des fonds notamment en réalisant les supports, la vidéo de présentation, le contact et la conception avec Lamplighters, c'était un peu le bordel dans l'explication mais en gros c'est ça. Le mec minait de la crypto sur leurs serveurs en 2021 et c'est parti de là... avec un "beau projet". 🤪

2. Il a rigolé sur ce sujet en disant que le CEO était un tueur et qu'il avait lancé une autre société dédiée cotée en bourse "AIB" (BlockchAIn Digital Infrastructure, Inc) qui va aider à financer le projet (je sais pas comment vu les finances de la boite)

3. Ils parlent du dispositif IRA et Joe parle du fait qu'ils ont besoin de terminer la Phase 1 (juillet 2026) puis le début de la Phase 2 (mi-2027, la pyrolyse) pour commencer à prospecter pour financer le déploiement du data center. En gros financement IRA pour la centrale puis financement tier inconnu pour le data center.

4. Vu les finances, non 😂

Concernant 2CRSI :

Tant que 2CRSi ne publie pas le détail des cautions et lettres de crédit reçues de NYGC et Atlas, et la part du CA US réellement encaissée vs facturée vs livrée, pour moi il faut rester à l’écart

Et surtout répondre à 4 questions

1. Quelle due diligence a été menée sur NewYork GreenCloud, dirigée par un vétérinaire sans expérience datacenter ?

2. Quelle est la capacité réelle de paiement d’Atlas Cloud AI (LLC créée en février 2025, sans bilan publié) sur un engagement multi-milliards ?

3. La signature du deal 610 M$ NYGC a-t-elle été conditionnée à un financement tiers identifié, et lequel ?

4. 2CRSi a-t-elle vérifié la solvabilité de Blue Ridge / VCV / Tiger Cloud, dont l’écosystème consolidé déclare 15 265 $ de cash ?

$ASTS “Starlink has built the best hockey stick, meaning fixed broadband for at-home internet, to ever hit the market, miles ahead of its competitors. Starlink is now taking this hockey stick and using it to play a round of golf on the PGA Tour. It’s simply the wrong tool for the job today.”

— CEO, Crossroads Capital Management LLC.

$ASTS - YouTube exclusive video.

Comparing AST SpaceMobile and Starlink - Two satellite companies that couldn't be more different

Make sure to subscribe to the YouTube channel. 🔔

https://t.co/iQnBT9aj1F

$ASTS In 49th JIO annual meeting, they will partnering with leading global sats providers by leasing satellite capacity and build ground stations that will support partner sats while develop their sats.

I think JIO can’t share ground station with Starlink, which is regenerative.

Résumé du communiqué de 2CRSI

1. Un rapport émanant d’un vendeur à découvert

Grizzly détenait une position short nette de 0,89 % du capital (~200 000 actions) déclarée à l’AMF avant publication. L’auteur a donc un intérêt financier direct à la baisse du cours. 2CRSi rappelle que la diffusion d’informations trompeuses pour influencer un cours peut constituer une manipulation de marché (Article 12 du règlement MAR).

2. Réalité de l’activité

2CRSi conçoit et fabrique ses serveurs sur des sites identifiables : Strasbourg, Manchester, Rouses Point (NY), et bientôt Chennai (Inde) via un partenariat avec Valeo. Les comptes sont audités par Ernst & Young. Le conseil d’administration a saisi son Comité d’Audit et des Risques.

3. Revenus et répartition géographique

La “contradiction” pointée par Grizzly n’en est pas une : 71 % en Asie correspond à la répartition par destination de livraison, tandis que ~50 % en Amérique du Nord correspond à la facturation par région. Croissance US tirée par l’IA, le renforcement commercial en Californie, et la redirection de composants Nvidia après les restrictions d’export d’octobre 2022. La remise exceptionnelle critiquée correspondait à une compensation pour retard de livraison (Noël 2024 → février 2025), pratique commerciale standard.

4. Contrat-cadre de 610 M$ et NewYork GreenCloud (NYGC)

•Le contrat de 610 M$ n’a généré aucun revenu sur l’exercice ; la croissance US vient de commandes séparées.

•2CRSi est simple fournisseur de matériel ; déploiement par phases (2026 puis 2027-2028).

•Aucun lien capitalistique entre 2CRSi/Alain Wilmouth et NYGC. Le titre de “Co-Founder” évoqué venait d’un document de levée de fonds de NYGC listant les intervenants du projet, pas des dirigeants.

•2CRSi a facturé à NYGC des services (site web, brochures) pour moins de 100 000 €, au prix du marché.

•Relation commerciale avec Dr. Joseph Church depuis 2021. Politique stricte : livraison conditionnée au paiement.

5. Contrats Allemagne, New York, Canada

Commandes livrées et payées, revenus reconnus. La confidentialité sur certains clients est une pratique commerciale légale et courante.

6. Consortium ÆTHER

Candidature déposée le 20 juin 2025 dans le cadre de l’appel européen EuroHPC pour les futures AI Gigafactories. ÆTHER n’est ni une filiale ni une entité liée à 2CRSi, mais un cadre de coopération industrielle européen. Négociations de site annoncées le 18 février 2026, en phase préliminaire.

7. Sites américains

•Rouses Point : 2CRSi n’a jamais prétendu être propriétaire du bâtiment (redéveloppé par ERS Investors, aménagé par 2CRSi) — déjà précisé dans le communiqué du 17 mai 2021.

•2CRSi Cloud Solutions : ligne d’activité interne, pas une entité juridique distincte.

•Fremont : activité transférée vers San Jose puis Rouses Point. Retirer une référence n’est pas une dissimulation.

https://t.co/Dg6eKGTlPt