$IREN & Anthropic: The Strategic Inevitability of a Partnership — and IREN’s Emerging Pricing Power

A:

According to the latest data, Anthropic’s compute supply is nowhere close to keeping up with its revenue growth. Dario Amodei confirmed that during the first half of 2026, the company experienced an 80x surge in revenue demand. Anthropic’s annualized revenue has now surpassed $30 billion, and the number of enterprise customers spending more than $1 million per year has grown beyond 500 — then doubled to over 1,000 within just two months.

Anthropic is currently paying xAI $15 billion per year for compute capacity under a contract that lasts until May 2029.

At the same time, Anthropic has signed multi-gigawatt TPU agreements with Google and Broadcom, with deployments expected to begin in 2027. Before this, the company had already diversified across AWS, Azure, NVIDIA GPUs, and other hardware platforms, reflecting a strategy of “matching different workloads with the most suitable chips.”

But if you look closely, Anthropic’s compute structure is filled with hidden risks and strategic poison pills.

On the surface, its four major compute supply lines appear “diversified.” In reality, the structure is extremely fragile. Every supplier involved has both the motivation and the ability to weaken — or even seriously damage — Anthropic.

Amazon is Anthropic’s largest shareholder and may provide up to 5GW of AWS compute capacity, while simultaneously competing directly with Claude through Bedrock. Every time Anthropic trains Claude, it is effectively strengthening AWS’s own competitive position.

Google provides multi-gigawatt TPU capacity, yet Gemini is one of Anthropic’s most direct rivals. Training Claude on Google’s TPUs potentially exposes model architecture and data access patterns, creating real strategic intelligence risks.

Microsoft Azure is another major compute provider, but Microsoft is deeply tied to OpenAI — Anthropic’s number one competitor. Training Claude on Azure essentially means subsidizing a rival’s infrastructure ecosystem.

Then there is xAI: both a competitor and a supplier holding a contract that can be terminated at any time. Elon Musk only needs to issue a 90-day notice to cut off the supply.

There is something deeply ironic about this whole situation. Colossus 1 is essentially a stranded asset after Musk shifted his main compute focus toward the Blackwell-powered Colossus 2. Letting Anthropic use part of that capacity is almost like casually giving Dario Amodei a drink of water to ease his desperation.

It makes Dario look like the pitiful bell-ringer Quasimodo — standing under the blazing sun while being whipped — yet still willing to pay $15 billion just to drink that water. The image feels almost humiliating in its desperation.

Put together, these four supply lines lead to one unavoidable conclusion:

Anthropic’s core compute infrastructure is entirely dependent on platforms controlled by direct competitors. This is not “multi-cloud redundancy.” It is a situation where every supply route runs through hostile territory.

B:

Now look at what IREN brings to the table:

5GW of secured global power capacity, with expansion still ongoing

Multiple gigawatt-scale sites powered directly by the grid and supported by green energy

A strategic partnership with NVIDIA to build what may become the world’s premier DSX flagship AI factory

No model business — IREN develops no AI models and does not compete with Anthropic

No strategic investment entanglements — IREN neither owns Anthropic equity nor is owned by Anthropic now.

No public cloud competition — IREN does not operate a hyperscale cloud platform and does not compete with Claude’s API business

A pure infrastructure identity: power + data centers + GPU operations + software orchestration

For Anthropic, IREN is the only truly neutral large-scale compute provider in the market.

There are five major dimensions that make IREN’s advantages almost irresistible to Anthropic — like a highly addictive drug.

Dimension One

Anthropic’s dependence on competitor-controlled compute creates a form of “replacement-cost pricing trap.”

Every unit of compute purchased from rivals comes with hidden costs:

exposure to strategic intelligence risks,

the possibility of service reductions,

weakened leverage during financing negotiations,

and potential regulatory scrutiny over “competitor-controlled training infrastructure.”

These costs may not appear on financial statements, but they are very real.

IREN’s neutral compute infrastructure eliminates these risks. Looking at the extremely expensive deal Anthropic signed with SpaceX/xAI — despite the obvious competitive toxicity — proves that Anthropic is willing to pay enormous premiums for compute access when under pressure.

Dimension Two

At the physical infrastructure level, Sweetwater’s 2GW scale creates a form of real-world irreplaceability.

Globally, there may be only one provider capable of delivering a single-site, gigawatt-scale, liquid-cooled, fully powered, DSX-certified facility by 2027–2028.

Anthropic simply has no credible “we can go elsewhere” bargaining position.

Dimension Three

Anthropic’s growth rate is dramatically faster than the timeline required to build compute infrastructure.

This mismatch between quarterly competitive pressure and multi-year infrastructure construction cycles means Anthropic cannot afford to wait. It must lock in the next 3–5 years of capacity as quickly as possible.

Again, the image of Dario as Quasimodo under the scorching sun feels strangely accurate.

Data centers are his water. Water. Water.

Dimension Four

The pressure from competing with OpenAI is so intense that Anthropic is already willing to accept terms from someone like Elon Musk.

So when a provider like IREN appears — offering enormous, high-quality capacity combined with NVIDIA-backed DSX flagship AI factory architecture — the attraction becomes overwhelming.

And if DSX significantly boosts compute efficiency, then 2GW inside a DSX environment may effectively deliver the output equivalent of 4GW or even 8GW elsewhere.

Dimension Five

IREN’s 5GW global data center pipeline stretches across the United States, Europe, and the Asia-Pacific region:

further expansion at Sweetwater,

new capacity at Kiowa,

the 490MW Nostrum project in Spain with additional gigawatt-scale development reserves,

and future Australian projects.

This physical infrastructure pipeline aligns perfectly with Anthropic’s two most urgent strategic needs over the next three years:

European regulatory compliance

Global expansion

The EU AI Act, GDPR, and data sovereignty requirements are increasingly forcing frontier AI companies to deploy local compute infrastructure inside Europe.

Anthropic can no longer rely entirely on U.S.-based cloud providers for cross-border hosting. It needs trusted, regulated infrastructure physically located within the EU.

Nostrum’s 490MW platform provides an immediate European compliance gateway, while Sweetwater serves as the primary U.S. training hub. Together, they naturally form an integrated cross-regional compute strategy.

Even more importantly, Anthropic’s future expansion into Asia-Pacific will also require local infrastructure nodes, and IREN’s Australian projects provide a future foothold there as well.

In other words, Anthropic’s entire globalization roadmap could potentially be completed through IREN’s infrastructure pipeline alone.

Taking all of this together, the potential partnership between IREN and Anthropic is no longer about “who chooses whom.”

Logically, it increasingly feels inevitable.

In fact, I believe the discussion has already shifted toward a different issue entirely:

Pricing power.

Under these conditions, IREN may gain rare leverage over contract structure negotiations, including:

higher upfront prepayment requirements,

stronger take-or-pay commitments,

dual-index pricing tied to both inflation and chip upgrades,

control over future expansion capacity options,

and even the possibility of exchanging capacity discounts for Anthropic equity participation.

Where does this bargaining power come from?

IREN’s neutrality itself carries enormous premium value for Anthropic.

That neutrality can be systematically priced into contracts.

Time pressure strengthens IREN’s leverage.

Anthropic is simultaneously squeezed by exploding demand and brutal competitive pressure.

IREN holds overwhelming advantages in data center quality, power availability, security, and stability.

IREN can satisfy three strategic needs at once:

U.S. training, European compliance, and future Asia-Pacific expansion.

This dramatically narrows Anthropic’s alternatives.

With a secured 5GW global infrastructure pipeline — and future expansion beyond that — IREN may become Anthropic’s only truly dependable global compute sovereignty provider.

That creates extraordinary leverage over both pricing and contract structure.

Finally, this may also explain why IREN no longer appears interested in signing traditional presale-style agreements like CRWV and NBIS.

With advantages like these, preselling its power capacity too early would effectively mean selling itself cheaply.

So even if IREN and Anthropic do eventually sign a deal, I believe we are likely to see a completely different kind of partnership structure — one that could reshape industry expectations.

This is my first article exploring the potential IREN & Anthropic relationship.

I plan to continue the discussion later when time allows. There are still many important topics worth analyzing, including how such a partnership might actually work in practice, NVIDIA’s potential role, and much more.

Please stay tuned.

And lastly, I’ve been extremely busy recently and haven’t had the energy to reply to everyone’s comments. Thank you for your understanding and support.

There is no larger long-term strategic move than this — NVIDIA joins forces with $IREN to build the flagship AI factory deployment for the DSX architecture

The market will continue to repeatedly reinterpret the deeper intent and long-term objectives behind the partnership between NVIDIA and IREN.

On May 7, 2026, IREN’s CEO reposted NVIDIA’s official announcement on X regarding the partnership between the two companies: NVIDIA and IREN Limited today announced a strategic partnership to accelerate the deployment of next-generation AI infrastructure.

NVIDIA announcement

https://t.co/WW1RJ9ERH3

At the same time, IREN also released another announcement on its own website: IREN signs a US$3.4 billion AI cloud services agreement with NVIDIA.

IREN announcement

https://t.co/f3W6yR90Mq

The two announcements, each emphasizing different aspects of the cooperation, carry extremely significant implications.

First, after careful verification, this is the first time NVIDIA has sought external compute leasing. There are three major turning points in industry development embedded in this move.

A reversal of roles: NVIDIA becomes a “major external compute customer” for the first time

In the past, NVIDIA’s relationship with infrastructure companies was almost always centered around “selling hardware” or “borrowing hyperscaler data centers for DGX Cloud.” But in this US$3.4 billion agreement with IREN, NVIDIA is, for the first time in its history, leasing third-party compute capacity at large scale and on a long-term basis as a customer, for use by its own AI research teams. This kind of “reverse leasing” is unprecedented for NVIDIA in both scale and nature.

The selective external exposure of its most core secrets: this point carries the deepest implications

For a long time, NVIDIA has insisted on keeping its most critical R&D work — chip design, driver optimization, and large-model training — inside its self-built supercomputers such as Selene and Eos, creating a closed loop of “building the shovels and mining with them itself.” But this time, outsourcing a 60MW research workload to an external data center is highly significant. It signals that compute-chip R&D is beginning to transition toward external collaboration.

The first opening of stack management: introducing Mirantis to manage NVIDIA’s internal R&D clusters

Previously, NVIDIA’s internal cluster management was handled entirely by its own engineering teams. But under this agreement, NVIDIA is for the first time allowing third-party management, bringing in Mirantis to participate in cluster orchestration and operations. This also signals a transformation in NVIDIA’s latest compute architecture R&D approach — beginning to “strengthen external collaboration” for lower-level operational work such as server cooling, restarts, and Kubernetes configuration.

As the ability of individual GPU chips to increase computing performance gradually approaches physical and engineering limits, the next phase of AI compute advancement is shifting from “single-chip performance competition” to “system-level scalability competition.” This is NVIDIA’s direction of transformation.

The primary paths for the next stage of AI compute improvement include: GPU clustering, high-speed interconnects, rack-scale computing, and data-center-level coordination. This requires GPU manufacturers (NVIDIA), data center designers/builders/operators (IREN), and supercluster operating systems (Mirantis) to jointly collaborate on development.

What they are developing is precisely the NVIDIA DSX architecture referenced in the NVIDIA-IREN partnership announcement. And IREN’s hyperscale SW site in Texas is becoming the flagship deployment location for NVIDIA’s DSX architecture. This is absolutely not a simple narrative of NVIDIA investing in a company and becoming a shareholder.

For the world’s leading company that holds the core secrets of AI compute chip R&D, this is not a trivial matter.

From NVIDIA’s perspective, there appear to be many potential partners, such as CoreWeave, Nebius, Oracle, Microsoft Azure, Amazon Web Services, and Crusoe, and NVIDIA has already invested in or partnered with these firms before. But why did it choose IREN for this most important transformation?

Because IREN possesses too many things that are uniquely its own:

Multiple GW-scale single sites with secured long-term power supply

Grid interaction capabilities

Vertical integration

Ultra-long-term site planning and abundant land supply

Green energy

Acting as its own design-and-build general contractor

Long-term accumulation of data center operational experience

Advanced design and technical capabilities

Compared with the companies above that NVIDIA has already partnered with, even if IREN temporarily lacked software capabilities, NVIDIA was still willing to wait until IREN acquired a software company before announcing this deep cooperation. Moreover, Mirantis has long been one of the three software companies that have collaborated with NVIDIA for many years. It is highly possible that NVIDIA itself played the role of connector behind IREN’s acquisition.

NVIDIA is transforming toward system-level compute scaling and building an AI factory template. In the future, the products it sells may no longer simply be GPU chips, but complete racks, clusters, or even entire AI factories.

That inevitably requires standardized data centers in order to guarantee performance, compatibility, scalability, and token efficiency.

What NVIDIA needs are facilities with massive long-term secured power supply, land, GW-scale campuses, HPC DNA, rapid construction capability, neutrality, automated scheduling capability, workload routing, GPU virtualization, fault recovery, and cluster operating systems capable of distributed training management.

At present, IREN is the only company that possesses all of these elements simultaneously.

What they are trying to build is the industrial standard for the next phase of the AI industry.

The greatest companies do not merely participate in industries — they define the standards.

From this perspective, there is no larger strategic theme than this one.

Selling compute capacity to hyperscalers, partnering with Anthropic, or developing new sovereign AI businesses are all important, but none compare with this.

The deeper meaning of last week’s announcement will require time for the market to fully interpret and understand. I believe I have already analyzed this trend relatively clearly.

This move by NVIDIA and IREN, once executed successfully, could once again widen the gap between the NVIDIA ecosystem and Google just as Google had begun catching up — and it carries major implications for the entire AI industry.

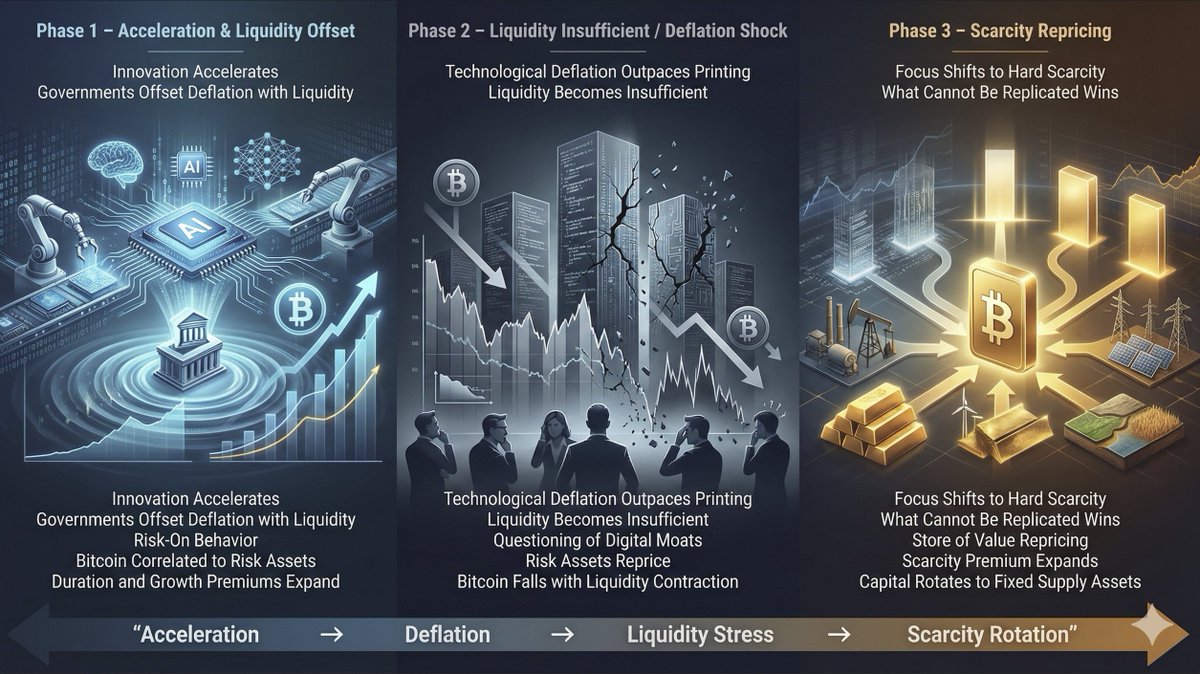

In this week's Sunday video (https://t.co/c9hJBCWFf3) I will begin showing this slide each week to remind everyone where we are in exponential innovation.

As the dispersion in equities continues, we are in phase 2 of the AI acceleration as deflationary intelligence abundance destroys valuations of all digital moats and compresses valuations of long-duration assets.

Phase 3 begins this year as the race to asset scarcity accelerates and now includes digital scarcity.

RIP to the great Dutch Grandmaster Jan Timman. He was the leader of the new Western generation after Fischer. Unlike many, he was a serious analyst and researcher who loved every aspect of the game, including compositions. He was at his powerful peak through the 1980s to 1993, when he lost matches to his peer Karpov and Nigel Short of the new generation. We dueled many times, including his victory in my "heaviest" game ever, where our moves were mirrored by machines moving huge shipping containers as pieces in Rotterdam! We also argued many times, as he also cared deeply about the future of our beloved game. He was my first opponent after I became world champion in 1985, pictured here in Hilversum, NED, before game 5 of our match on Dec 20, I believe.

The only people who think SaaS is dead are coders, who see Claude replacing THEM.

There is a lot more to running a company than writing code.

The biggest function is accepting liability and providing support for critical business functionality.

If I, a business, VibeCode a Docusign replacement and that replacement fucks up my contracts or leaks customer data, I have accepted the legal liability for that fuckup.

If I hire Docusign to do it, that liability rests on them, and they have hundreds of people managing and insuring that liability in various ways. Compliance and security teams, etc.

When you risk-adjust that outcome, the cost savings simply don’t make sense.

A shockingly small part of running a SaaS business is *writing the actual code.*

What will actually happen is that SaaS will become more profitable because a smaller team of elite coders + LLMs will cost less and produce better code than vast teams of entry-level or mediocre coders.

This will play out similarly in other industries. You will need fewer lawyers and doctors, but they will all become more productive and deliver higher quality services using LLMs as tools, so law and healthcare will thrive and utilization will increase - Jevon’s paradox.

🚨 $IREN UPDATE:

Hyperscaler demand is not the constraint. Partnership selectivity is the key!

Using only ~10% of their massive 4.5GW secured power, IREN is on a runway to $3.4B in AI Cloud ARR by EOY 2026 (note $2.3B of this IS ALREADY CONTRACTED).

To all the “wen deal” bears and impatient shareholders out there, just know CEO Dan Roberts DOES NOT NEED TO RUSH!

IREN have to carefully plan and manage the execution of 4.5GW of secured, grid-connected power — one of the largest ‘genuine’ pipelines on the planet! That scale doesn’t just appear overnight. Execution, timing, and quality of partners all matter.

While I’m sure they can sign up the whole 4.5GW tomorrow, they are taking their time and acting in the best interests of the company, and that means striking the best deals with the absolute best counterparties on the best terms.

Hit the REPOST button if you have max conviction like me 💪👊🔥🚀

WE HAVE A REGIME SHIFT AT Nowcast IQ

Our nowcast data is now turning decisively pro cyclical, especially in the US, and it rhymes with the thesis we have laid forward on the CapEx cycle getting an extremely large artificial boost from the one big beautiful bill. The CBO estimates a 0.8% impact on GDP this year, but we dare to say already that it is WAAAY too conservative. At the same time, we are seeing inflation through the floor. We are ranging around 0.15% a month in our nowcasts, which is roughly half of what economists pencil in, so even if some people try to claim that softer inflation is priced in, we beg to differ on that view.

So we have gone from a QE like regime with weakish cyclical growth to strong cyclical growth, and liquidity remains very decent, while inflation is moving down. That is what we call a gung ho regime, and it could not get more textbook upbeat. Many of the rotations seen early this year will likely pause given this, and we should see Tech make a comeback.

Here is the text from our trade scanner, and a few charts to support the thesis. ISM Manufacturing is likely heading to 57 to 60 already before summer.

Best data in the world in my opinion!

What a lot of people don't know how to do is to differentiate a primary dump from a secondary dump.

This is important because primary dumps are structural and bitcoin specific, meaning the selling is driven by a lost of faith in btc, a deliberate exit from btc. In other words, Btc is at the center of their sell decisions. It's the very reason for the selling.

Secondary dumps are different in that most of the sells are forced, and not willful. These sells are forced liquidations but not planned due to a lack of interest or trust in btc. That's what this dump is. Secondary dumps have a tendency to quickly snap back leaving behind Bitcoin's famed, wildly long wicks. Structural dumps do not.

As you can see by the liquidation stats below, the $2.54 billion in damage over the past 24-hours is mostly sh*t coins being completely obliterated. It's not bitcoin, despite bitcoin representing more than 70% of the entire market with Stablecoins removed. Bitcoin's part of this entire liquidation is only 30% ($781M), and most of that is forced by sh*tcoiners being liquidated out of their bitcoin-backed leverage positions on things like ETH, ZEC, SOL, SYN, XRP and now even gold and silver which exploded on CRAP-tocurrency exchanges. Someone one lost $223 million on a single ETH trade. That's just one trade. 🤦🏽♂️

In short, bear markets declines are different than this one on average. This smacks of a sh*t coin driven cascading collapse that is triggering btc collateral wipeouts. These are the declines that serve as great gifts to the asute. They are to be leaned into, not avoided and run away from, like lil' sissies.

Anyway, that's my 2 sats on the matter. Take it or leave it.

Stack harder.