LBE’s will need to surpass 10k Bitcoin Hodl to help them survive the next Bear market.

The next hurdle will be 50k Hodl for them to be a significant player.

>100k Hodl will be their ultimate hurdle for Legacy🔥🫡

$BTC $MSTR $MTPLF $TSWCF $MSTY

Housekeeping: I've renamed a metric

"Drag" is now "Senior Claims %" (Claims % for short)

The number never changed. It's still net senior claims over total BTC. But "drag" implied a feeling and a direction the metric was never meant to carry

It's just the share of the stack that sits ahead of common equity. So it should say that

When the term is the problem, fix the term

This is what I built CEBE for. @metaplanero ran the common ownership breakdown across the big treasuries

The % of the Bitcoin stack that actually reaches common shareholders after senior claims

Metaplanet 84%

Strategy 62%

Strive 56%

It's the comparison BPS can't show

$MSTR | $STRC | $ASST | $SATA:

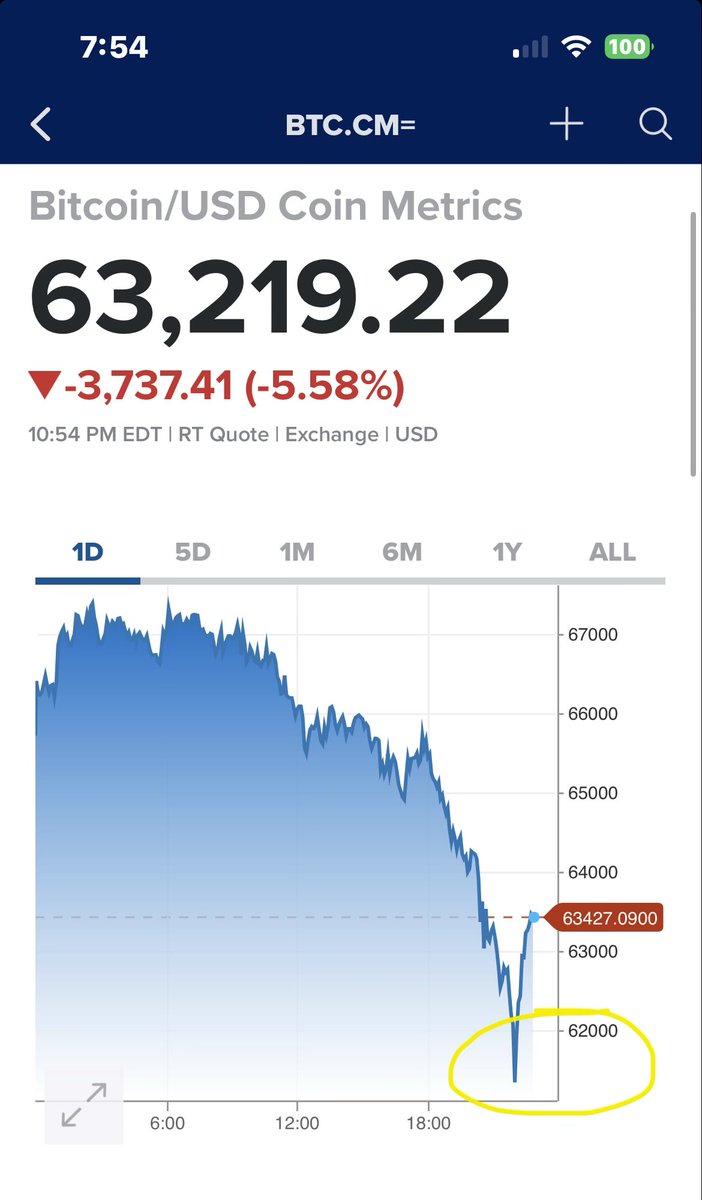

I am seeing a lot of conversation around $STRC | $SATA today, people calling for blow-ups, crashes, etc. everyone needs to relax.

As I said in my earlier post, $STRC | $SATA are perpetual preferred offerings second, $BTC derivatives first. Weakness in $BTC will lead to this kind of price action.

What we are seeing here is sentiment and narrative shift leading to a market (over) reaction in price. Not the other way around. There is no issue with using the 30-Day VWAP as a price benchmark for share issuance, and there is no complex arbitrage that is going to take place between the daily | semi-monthly pay outs.

Algo’s are not looking to perform HFT-Kung-Fu to pocket daily dividends from $SATA or arb moves overnight or rotate between @Strategy prefs. The daily payout from $SATA is tiny, and the monthly (soon to be semi-monthly) payout from $STRC isn't an ideal target.

Why? Because they are all correlated to $BTC and the payout is too small to attract that kind of attention. Due to the beta (correlation) with $BTC moves, any serious quant | algo desk running trading strategies on these names would model $BTC price action as a (if not the) primary variable. (I have asked around, this checks out)

General slippage, spreads, periodic thinner liquidity, and overnight $BTC price action will eat any edge.

@Strive | @Strategy changed payouts to smooth the volatility; not hand out more arbitrage windows. IMO any real algo action around $STRC | $SATA will focus on mean-reversion and “peg trading" instead.

Buy when they dip below the target range (or force a de-peg); then sell moves above par, or right at $100. There might be opportunity to use the dividends as a tailwind, but that is not the focus. The real edge comes from riding, or pushing, those de-pegs below and back to par.

The last thing we want is heavy algo trading on these, that will fight the very price stability the prefs are engineered for, increase the vol, hamper the sharpe ratio, all while the mechanical link to $BTC stays intact and exacerbates the moves.

The important context behind Strategy selling 32 BTC is S&P.

When S&P assigned Strategy a “B minus” credit rating, it cited reliance on capital markets as a weakness, “particularly since the company is reluctant to sell bitcoin it holds as investments.”

This sale directly rebuts that critique.

Rather than showing a change in treasury philosophy, Strategy showed that BTC is not trapped on the balance sheet. It is a liquid reserve asset that can be accessed when management decides it is economically rational.