Phia — the buzzy shopping app co-founded by Bill Gates' daughter, Phoebe — is claiming credit for online sales it didn’t actually drive, a Bloomberg investigation found. Read our exclusive story: https://t.co/KYuWkmkE7D

📷️: Dia Dipasupil/Getty Images

.@sama to CNBC: "There's no connection between any potential OpenAI equity or other companies' equity in a sort of sovereign wealth fund and the right regulatory approach. I think completely separate."

Introducing a new way to reflect on how you use Claude.

Your monthly recap shows when you use Claude most and what you spent that time working on, with options to set quiet hours and nudges to take breaks. Find your dashboard in Settings under Reflect: https://t.co/8QAn47W5rI

We've usually stayed away from model comparisons but 5.6 vs Fable is a unique situation

We've never had a case where the team is so completely convinced on which one is better

Here's the timeline of our experience with it

- We test early versions of 5.6 for a couple of weeks and have a great time, it feels like a step change improvement, enabling new workflows

- We get to try Fable and don't think it's not as good, I personally would take this experience with a grain of salt, there tends to be a bias when trying a new model when you already like another

- Fable and 5.6 are taken away because of the regulatory issues

- Our team is literally depressed that 5.6 is gone, we are looking for anything that could even partly replace it

- Fable comes back, and here's where it gets interesting, you would think Fable would be enough, but no, the team is still depressed that 5.6 isn't available

- Then 5.6 comes back and it's immediately clear that it's just way better than Fable

This situation was unique in that it was the closest we've ever gotten to having an unbiased comparison of two models

We audited SWE-Bench Pro, one of the most widely used AI coding benchmarks, and found it no longer reliably measures frontier coding capability.

We find 30% of SWE-Bench Pro tasks to be broken, and are retracting our previous recommendation that the research community use it as a leading coding eval.

https://t.co/wDdSEjBe4F

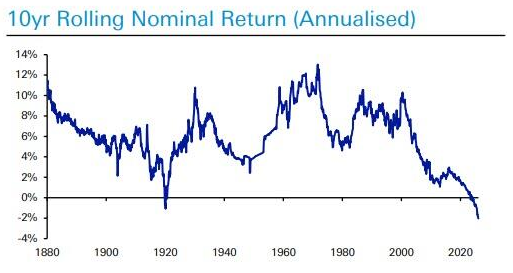

I published a note today that I've been thinking about for months.. About how the US stock market has arguably become too big and too imp to fail.. It's basically America's retirement fund now and poss even the savior of social security which is expected to run out of money in less than 10yrs

-Curr 55% of ppl own stocks, by far most in world. And w/ Trump Accounts bringing in 28 million add'l americans into stock ownership the vast majority of ppl (incl Top 1% (who own HALF of stock mkt), middle class and lower income) will have financial interest in the health of stock mkt and they're all voters = the political pressure to keep stocks out of a prolonged bear market is going to be very powerful.

-As such I think there's good chance the Fed will buy equity ETFs in the next major downturn to support market and it will be common practice going fwd. China and Japan already do this. They may even target certain sectors or Capex cos with the purchases.

-This is a massive variable that I feel like is a blind spot among the experts out there and why the bears get run over time and time again altho I think investors are onto it as evidenced by the persistent flows into ETFs during pullbacks as well as a survey of 1000 ppl showing 3/4 of them are confident the Fed will bail out markets in next crisis.

-This is just one byproduct of the 'Nothing Stops This Train' monetary supply explosion and debt extravaganza sweeping the world but esp in US which at this point feels irreversable.. Thoughts? lol

The OpenAI Deployment Company agrees to acquire Northslope, an applied AI company founded by ex-Palantir employees, its second acquisition after buying Tomoro (@madisonmills22 / Axios)

(Visit Techmeme dot com for the link and full context!)

THE MOST DANGEROUS MARKET IN THE WORLD RIGHT NOW IS JAPAN.

Japan's 10 year and 20 year bond yields just hit 30 year highs.

Both moved to their highest levels in three decades.

The 10 year yield is up 137 basis points over the past 12 months, and up another 9.1 basis points in just the last 4 weeks. The move is accelerating, not slowing down.

1. 10 year JGB yield: 30 year high

2. 20 year JGB yield: 30 year high

3. 10 year yield: +137bps over 12 months, +9.1bps over 4 weeks

4. 20 year auction demand: weakest since the May 2025 rout

5. Yen: trading near 40 year lows

6. Japan debt to GDP: over 200%

7. Japan foreign reserves: over $1 trillion, 2nd largest in the world

Two things are happening on the supply and demand side at the same time.

On supply, Tokyo just announced a plan to mobilize over ¥370 trillion ($2.29 trillion) in public and private investment through fiscal 2040. That means more bond issuance ahead.

On demand, the Bank of Japan is the buyer stepping back. The BOJ is tapering its JGB holdings, targeting a reduction to about ¥480 trillion by March 2027, roughly 17% below its June 2024 level. That's the largest buyer of Japanese debt pulling back exactly when new issuance is rising.

Private banks can't fully absorb the gap.

Japanese megabanks run an average bond duration under 2 years, well short of the 9.5 year average maturity of outstanding JGBs. That mismatch is a structural reason the 20 year auction just saw its weakest demand in over a year.

Less demand at auction plus more supply plus a smaller BOJ bid means yields get pushed higher mechanically, not just sentimentally.

At the same time, the yen near 40 year lows is pushing the BOJ toward higher rates to defend the currency, which conflicts with keeping borrowing costs low for the government's spending plan.

Japan holds the largest foreign reserve stockpile in the world and has funded cheap borrowing globally for years through near zero rates. If Japanese yields keep climbing, capital funded by cheap yen borrowing and parked in higher yielding assets abroad has more reason to come home.

That's the yen carry trade unwinding, and it's one of the direct channels through which Japanese bond stress spreads into global risk assets.