❗️Let's Talk About Something Serious

"What concerns me most is that many of the datasets now being used to call a bottom are largely the same datasets that were previously used to predict last year's market top."

The market continues to move in the direction I have been concerned about.

Bitcoin is barely holding the $60,000 level, but personally, I do not believe this area will hold for very long.

Since last week, I have repeatedly stated that conditions are becoming increasingly serious, and my view has not changed.

Today, I want to discuss two major concerns I have about the current market, as well as some thoughts on how market data should be interpreted in the post-ETF era.

✅Concern #1: Liquidity Conditions Are Extremely Weak

liquidity flows that became especially important after the approval of the Bitcoin ETF continue to deteriorate and are now at some of their weakest levels.

So what about the liquidity indicators that were important before ETF?

Unfortunately, they are not telling a different story.

If market conditions were deteriorating while major players were quietly accumulating positions in the background, the situation would be different.

In that case, one could argue that the classic idea of "buying when others are fearful" was actually being put into practice.

That would be a constructive signal.

However, the data is not showing that behavior.

Objectively speaking, conditions continue to worsen.

✅Concern #2: Investor Psychology Remains Surprisingly Optimistic

The bigger issue is that many retail investors do not seem to view the situation this way.

While liquidity conditions and market data continue to deteriorate, the narrative being repeated across the market remains:

"Bitcoin has already fallen enough."

"Everyone is panicking, so this must be the bottom."

"Every crisis eventually becomes an opportunity."

"This is a buying zone."

I believe this is extremely important.

There is a significant disconnect between actual buying liquidity and what investors expect to happen.

In my experience, during periods of genuine fear, people do not openly talk about buying opportunities.

Instead, confidence disappears.

People become afraid even to discuss the possibility of a bottom.

Yet today, many participants continue to interpret the market through the lens of past experiences.

In other words, many still believe that the market remains within a predictable framework based on previous cycles.

To me, that is precisely what makes the situation more dangerous.

❗️Rethinking Data Interpretation After ETF Approval

✅1. Market Structure Has Changed Since ETF Approval

approval of Bitcoin ETF fundamentally changed trading behavior and market structure.

Those changes have also had a meaningful impact on on-chain data.

I recognized this shift last year and have been developing new datasets and analytical frameworks based on this new environment.

For more details, I recommend reading the ForeDex "Insight Report" referenced above.

The key point is simple:

Many datasets that historically carried a high level of reliability no longer behave the way they did in previous cycles.

Technical cycle indicators, on-chain cycle indicators, and market cycle indicators all produced results that differed significantly from historical expectations.

We saw this very clearly around last year's market top.

✅2. Think Back to Last Year's Market Top

At the time, the market was filled with discussions about the "Banana Zone."

Many investors built detailed plans around various cycle indicators:

"I'll sell when price reaches this level."

"Then I'll rotate into altcoins."

"Then I'll rebalance my portfolio."

These were not vague ideas.

People had specific roadmaps.

But did the market actually follow those expectations?

Not at all.

When I raised concerns about this at the time, the response was mostly criticism and dismissal.

Yet in the end, the market did not behave the way most participants expected.

✅3. If the Framework for Identifying Tops Has Changed

If ETF approval changed the way market tops should be identified, then our approach to interpreting data must also change.

If existing frameworks no longer work, new frameworks are needed.

If existing datasets no longer provide reliable answers, new datasets must be developed.

This is where the real problem begins.

✅4. We Are No Longer Looking for the Top — We Are Looking for the Bottom

Today, market participants are no longer trying to identify a top.

They are trying to identify a bottom.

And numerous arguments are now being presented to support bottom-calling narratives.

But here is the contradiction.

Many of the datasets currently being used to argue that a bottom is forming are largely the same datasets that were previously used to predict last year's market top.

This is what concerns me most.

If those datasets failed when identifying the top, then we must at least consider the possibility that they could also fail when identifying the bottom.

Yet the market largely ignores this possibility.

The assumption seems to be:

"They failed at the top, but they'll work at the bottom."

I believe that assumption is dangerous.

✅Conclusion

Taken together, market conditions continue to deteriorate.

Yet many investors continue building plans around datasets and frameworks that previously provided clear signals but ultimately failed when it mattered most.

That concerns me deeply.

Markets do not move according to our plans.

The same frameworks that failed to identify the top are now being reused to identify the bottom.

As retail investors become smarter, the dominant market participants become even more sophisticated, more strategic, and more capable of exploiting expectations.

The implication is straightforward.

Even if a major price shock occurs, the market is unlikely to unfold the way most participants currently expect.

In fact, when everyone is using similar frameworks and reaching similar conclusions, the probability of a larger shock may actually increase.

And even if the market eventually moves in the expected direction, there will likely be extreme volatility designed to shake investors out of their positions and cloud their judgment along the way.

We do not need to look very far back for evidence.

Even during the April–May period, the market repeatedly created one deception on top of another, constantly manipulating investor psychology.

And it worked.

If investors can be misled so effectively within a structure lasting only a few months, can we really be confident that a multi-year cycle will unfold exactly as the majority expects?

I am not convinced that it will.

The universal restroom symbols were created for the 1964 Tokyo Olympics to help international visitors navigate facilities without needing to read Japanese, using simple, color-coded male and female silhouettes that quickly became a global standard.

A 2009 study by Shinji Kitagami found that Japanese participants were uniquely likely to misinterpret restroom signs when the standard color coding was flipped, such as a blue female figure or a pink male figure. Because Japanese signage strongly depends on established color conventions, many participants unconsciously used color as a key cue alongside the shapes themselves.

In contrast, participants from other countries showed little confusion, suggesting they relied more on the pictograms’ forms rather than their colors. The findings highlight how even widely recognized “universal” symbols can be interpreted differently depending on cultural experience and visual expectations.

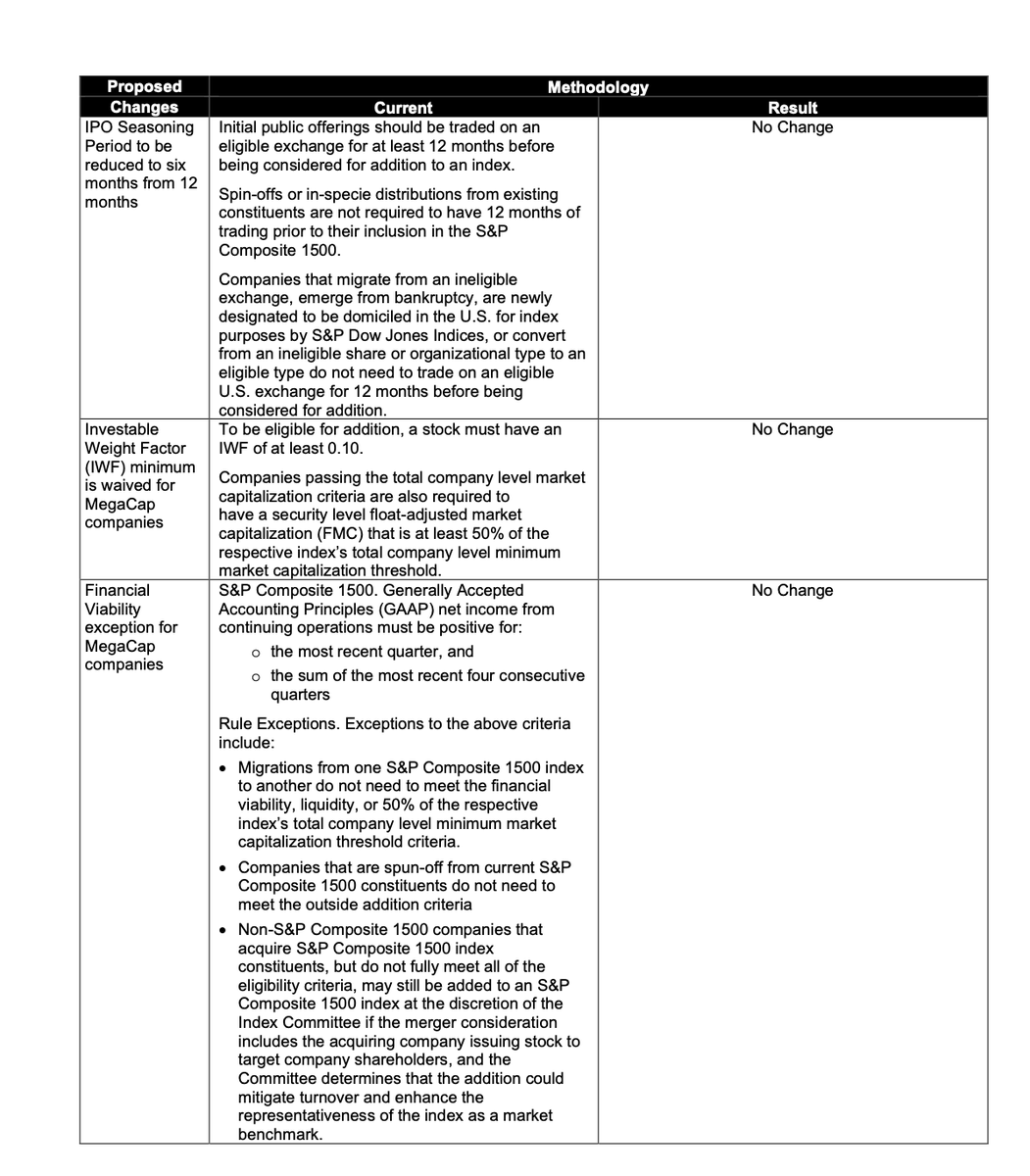

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

⚫ L'artiste franco-iranienne Marjane Satrapi, autrice de la BD autobiographique à l'immense succès "Persepolis", est morte, a-t-on appris ce jeudi par son entourage ➡️ https://t.co/T5xZN2Cz8H

긴 이별 (The Long Goodbye 1973) 히피 시대 캘리포니아를 배경으로 시대에 뒤떨어진 고지식한 사립 탐정이 주변의 모든 사람, 심지어 그가 키우는 고양이에게 까지 이용당하고 휘둘리는 영화. 마침내 진실을 깨닭고 사건 해결에 도달하지만 마무리는 씁쓸하다.

로버트 알트만의 장르 문법 파괴 영화.

Quentin Tarantino slams Hollywood as a "flavorless sausage factory" where miscast actors and "audience pandering" are ruining new movies.

“Flaws, implausibilities, audience pandering, miscast performers or just plain stupid s*it usually torpedoes every new movie coming out of the flavorless sausage factory that used to call itself Hollywood. These days, the entire concept of what is a movie is more inclined to inspire contempt in me than generosity... I’ve seen movies I liked since – ‘West Side Story’ (2021); ‘Horizon: An American Saga’ Chapter 1 and 2 (both 2024), a few others, but nothing that really held me in its grip and swept me away to the magical land of enjoyment that I use to visit regularly and was the reason I loved movies above all other artforms. These days I’d rather read a book." (via Sight & Sound)

https://t.co/Kslpbd4uoN

민주당 상상할 수 있는 최악의 선거를 치렀네 ㅋ 서울은 가져올줄 알았는데. 이재명이 부동산 가지고 겁줘서 그런거지 뭐. 평택을도 사채업자랑 역겨운새끼 둘다 나가리라 다행. 유의동은 어부가 지려버렸구만 ㅋㅋ 이진숙에 한동훈까지... 정청래도 이제 그만해. 김민석 등판 애보 민주 ㄱㄱ