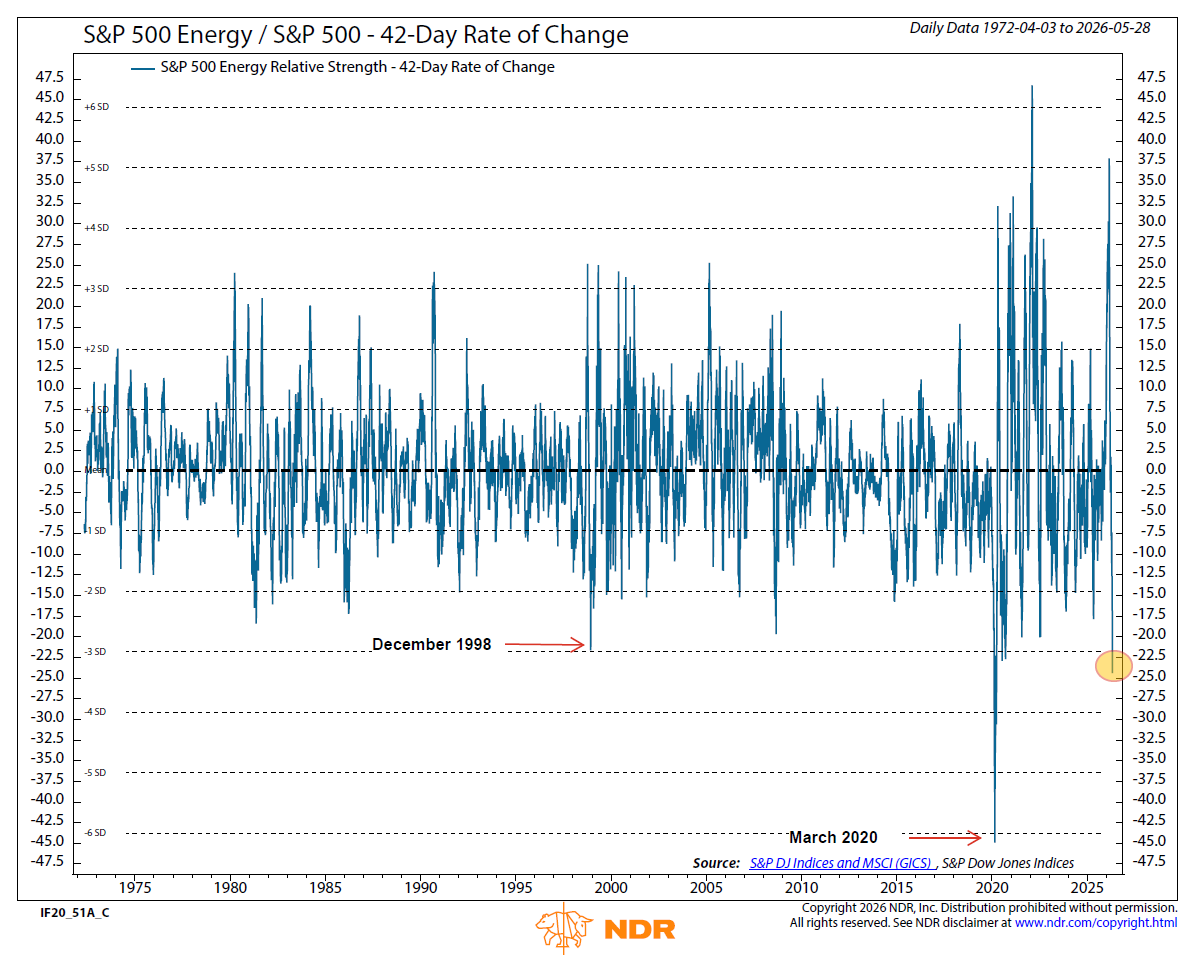

85% downside day following Warsh's debut as Fed Chair.

Clearly, the blue tie was the wrong choice.

In all seriousness, bad spot for realized correlations to pick up. Luckily, semis were able to avoid the worst of it, which has been the key contributor to the rally since April.

People asking what kinds of deals NJ was holding up?

How about a partnership with $AMCR (largest packager in North America) selling $PCT product across its product lines.

$PCT product will flow to $AMCR customers $KO, $CL, $DEO, $JNJ, $LOR.NE , MARS, $NSTL.NE , $PEP and more. NJ is just the start btw (and highlighted because of recent news), but these regulations apply to 20% of the US population and growing.

I understand the emotions of a stock down 40% on a poorly timed financing but at the end of the day we sit at 8 bucks post NJ approval, with deliveries starting, balance sheet fixed and an ever growing customer list. Will be interesting to see how the ramp catches people by surprise - I was a buyer this week.

$PCT ramp beginning as guided last Q. Massive pick up starting basically now but accelerating in 3Q and 4Q - as guided. I am very excited for where the company will be in six months.

My thoughts on the deal:

$PCT convert needed to be dealt with before EOM, I am sure there was lots of back and forth on options but the company decided to end the BS drama once and for all. Ofc an 8.20 price is rough but, as @UrbanKaoboy eloquently explained, when you have convert refi dynamics and are selling a 100 vol stock basically exclusively to hedge funds there will be a discount. Don't hate the deal, don't love the price, that's show business.

Two more things:

1. I’m hearing is that there was a privately negotiated “make-whole” to induce old convert holders to get called early. If that’s the case, the make-whole premium could’ve been in cash or stock and could’ve been on sweetheart terms better than stipulated in the original make-whole matrix. I’ve executed many a private “flush out” transaction in the past to allow companies to equities their debt. Certainly, if the make-whole was from additional shares, that could explain some of the earlier selling in the week.

2. Because $PCT is very difficult to borrow, bookrunners sometimes line up a term borrow facility and offer the synethic delta hedge as part of a “Happy Meal” to arbs. I don’t know for certain, but it would not surprise me if this was part of the deal especially since the additional share issuance would help unwind the synthetic short in short order.

Either or both of these possibilities would explain a lot of the price action from the prior days but also would bolster my belief that whatever hedging needed to be done has already been done.

$PCT Convert Arb 101, 6/11/26:

After speaking with some of my old convert arb coverage today (I did convert arb for over two decades in a former life), here’s my 2c on the new convert deal and share offering.

Old convert was on 100% delta, except for Sylebra’s $50 mm outright position. Net delta shares “to cover”: ~13.5 mm

New convert also sold on 100% delta, net of $36 mm over allotment (“shoe”) and net of Sylebra rolling into $50 mm of new bonds. Net delta shares to short: ~21.9 mm.

Theoretical net amount to short: 7.8 mm

New share issuance of 17.7 mm shares was placed at least 80% into “strong hands”/LT holders, which leaves only 3.5 mm sh up for churn. Between the 7.8 mm “to short” and the 3.5 mm up for churn that’s 11.3 mm shares potentially for sale.

Total dilution is about 14%. Sh out was 180 mm before today, and after today, it’s about 206.3 mm. Between that and today’s massive “volume” of 37 mm shares and stock decline, situation looks heavy right?

It’s the OPPOSITE, and here’s why:

Having been in this market for almost 25 years, I can tell you that these offerings are almost always preceded by folks “in the know” pre-positioning. Stock declined from $14 over the last several days to be priced at $8.21 today. You think that was a surprise to the arbs? I wouldn’t count on it.

Of the 11.3 mm shares “for sale” I am willing to bet that 50-75% of that was hedged in the prior couple days. Arbs likely OVER-hedged into today and net COVERED today.

Why was the volume so heavy? That’s another thing outsiders don’t get. When convert deals are sold “on swap” to arbs, the volume is double counted — buyers buy with a delta hedge and the sellers sell with a delta hedge. Today’s deal also involved an old deal getting unwound “on swap,” so the volume could have been artificially 4x’ed just based on these swap transactions.

The upshot of this is that I think the technicals are very asymmetric to the upside, and contrary to what it looks like, I think there is little to no overhang from this. I bought risk reversals today and effectively doubled my delta exposure today.

Finally, prior to today, my biggest fundamental concern for this company was their funding gap next year, and it made me queasy that they seemed to be counting on warrant exercise to close that gap. Today, they closed that gap, and even though I think they could have executed better, I think the fundamental story just got a lot more compelling as well.

The market’s freaking out over dilution on this $PCT move — but they’re missing the real story.

This isn’t desperation. It’s a smart balance sheet cleanup.

They’re using the new notes to repurchase 7.25% Green Convertibles due 2030. That’s expensive debt. Replacing it likely at a lower coupon in today’s market + their improved setup. This slashes the annual interest load and extends maturity out to 2032. More breathing room, less cash bleeding out every year.

On top of that, extra proceeds go to working capital and scaling the business — not just plugging holes, but actually funding growth.

Classic knee-jerk selloff to dilution.

Zooming out: lower interest expense, stronger liquidity, longer runway. This leaves PCT with a healthier balance sheet, not a weaker one.

Where were the signs? $PCT comes to market with Innovia for BOPP film, focus on snack/candy wrappers 🤔

Innovia is the largest BOPP film producer in the western world and has a specialty in high value/high performance wraps.

No one else in the world can offer a 40% PCR film, good luck complying with NJ, CA and 6 other states minimum PCR mandates without going to $PCT and Innovia.

https://t.co/OcmJvapO93

Russia is nearing implementation of a diesel and aviation fuel (kerosene) export ban after Ukrainian drone strikes disabled refining assets representing about 25% of the country’s diesel output and 30% of gasoline production

🚨The global oil market is racing toward a major shock. Inventories are collapsing while the Strait of Hormuz remains closed. Supermajor executives are issuing blunt warnings that prices could surge dramatically in the coming weeks.

•@exxonmobil SVP Neil Chapman: “We’re approaching unheard of inventory levels... really, really low levels... Once you get to that point, then you’ll see price shoot up.” He sees Brent potentially hitting $150–$160 per barrel.

•@Chevron CEO Mike Wirth: “The buffers and the shock absorbers are being steadily drawn down... the ability for the market to absorb this imbalance is drastically diminished.” He expects more upward pressure into July.

•Global inventories have plunged by a record 8.7 million barrels per day in May alone.

•The largest supply disruption in history - 12-13 million bpd offline - has exhausted strategic reserves and commercial stocks. We’re rapidly approaching the operational floor where physical shortages become unavoidable.

•This isn’t speculation. It’s the cold reality of the physical market overriding hopeful paper trading and diplomatic optimism. A spike to $150+ oil would hammer consumers, spike inflation, disrupt supply chains, and risk pushing vulnerable economies into recession.

•The crisis exposes years of fragile “just-in-time” inventory practices and over-reliance on chokepoints. Energy security demands better: diversified supplies, adequate reserves, and responsible domestic production.

•Markets will eventually balance through painful demand destruction, but the transition will be costly. Policymakers and leaders ignore these warnings at their peril.

•The bill for neglecting energy reality is about to arrive, and it will be measured in triple-digit prices and widespread economic pain.

Bottom line: If there really is a deal to be made to end this lingering war, President Trump would be well advised to make it ASAP. This isn’t a game – global markets do not care about your diplomatic protocols.

AI energy, materials and water needs might be the catalyst for the 4th turning kicking into high gear. Might turn out that human workers will be cheaper than AI, given resource limitations.

Imagine that!

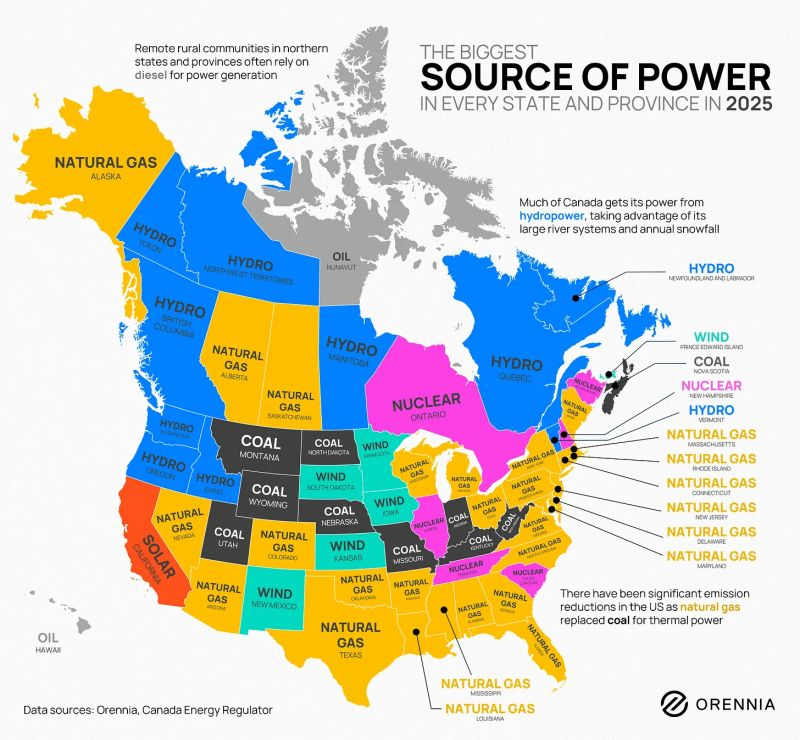

🇺🇸+🇨🇦 POWER REALITY CHECK

💥NATURAL GAS STILL RUNS NORTH AMERICA

Forget the narratives.

Look at the grid.

In 2025, the biggest source of power across most US states and Canadian provinces is still fossil based.

⚡ Natural Gas dominates the US

• Largest power source in 30+ US states

• Backbone of the US emissions decline, coal → gas switch

• Critical for reliability as power demand surges (AI, data centers, reshoring)

Another data point for the trade I covered my latest article, the link for it is in the below comments👇

Lot of interesting tid bits from the legendary $PCT head of IR Eric DeNatale (and lots of good answers to tech and commercial questions I see frequently as well.)

1) confirm P&G and L’Oreal are customers

2) Looking to get something out with Mars soon

3) PRICING. Brands are buying ISCC+ credits for .75/LB, conversations are STARTING at virgin plus .75 - that would put pricing around 1.40+/LB. Put that in your model and see what happens….

Big couple weeks, months then years ahead!

https://t.co/bKp153UIGB