Ptos a monitorar: 1. haverá algum rebalanceamento global de volta para commodities (“Halo” trade em algum grau de volta)? 2.

Haverá algum rebalanceamento análogo dentro de EM: de Coréia/Taiwan para Bz e outros em Latam?

Bz esta sobrevendido e com PE 12m fwd de volta pra ~8x (-1DP vs media).

For the record.

The Market Has Already Moved On

A leadership change is already

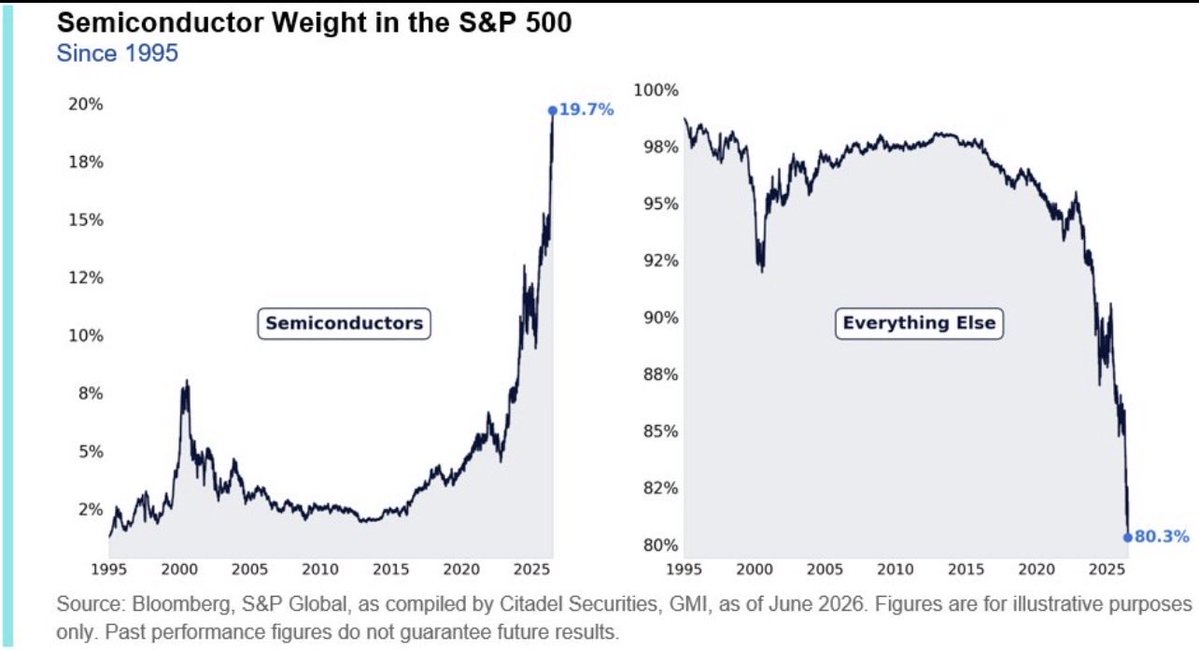

underway, but most investors are still clinging to the last trade. Everyone is crowded into semiconductors and memory, propped up by passive flows and a sell-side still extrapolating an era of outsized earnings surprises that is now behind us. The big earnings revision cycle in semiconductors and AI power is over.

The bottleneck trade is crowded and over-owned, and that playbook is exhausted. Semis now represent 20% of the S&P 500. A period of digestion is needed.

The market is broadening. Beneath the surface, the median stock is delivering double-digit earnings growth, with second-quarter earnings tracking toward 25% year-over-year. This is a rolling recovery, not a narrow AI story.

The AI cycle is not over, but it is evolving. Hyperscalers may be near a bottom and are beginning to convert capex into revenue, extending the cycle. But the bottleneck trade, owning semiconductors and AI Power, is no longer sufficient.

The era of massive upside earnings surprises is over IMHO

These stocks are crowded, expectations are elevated, and future earnings beats are unlikely to surprise as they have.

Leadership is rotating. Equal-weight indices, small caps, and domestic cyclicals are gaining traction, supported by improving earnings and still-muted positioning. Policy is reinforcing the shift, with a more Hamiltonian focus on domestic investment and productive capital.

Liquidity is also changing. Credit creation is moving from the Fed to the private sector, with bank deregulation playing a key role.

This is a more selective regime.

Investors can wait, or adapt. The market has already decided.

Bank of America’s research shows that elevated long-term earnings growth expectations have historically been associated with weaker subsequent equity returns, suggesting today’s exceptionally optimistic forecasts may leave the market vulnerable to disappointment.

This is it.

OpenAI is now considering drastic price cuts to win users from Anthropic, who will likely cut right back. Two companies losing billions, about to compete each other's margins to zero.

Buffett's worst kind of business: one that grows rapidly, devours capital, and earns nothing. He meant airlines. The most important industry of its age, where the customer wins and the shareholder bleeds.

Revolutionary technology and a good investment have never been the same thing.

The internet was real too. Most of the companies building it still went to zero.

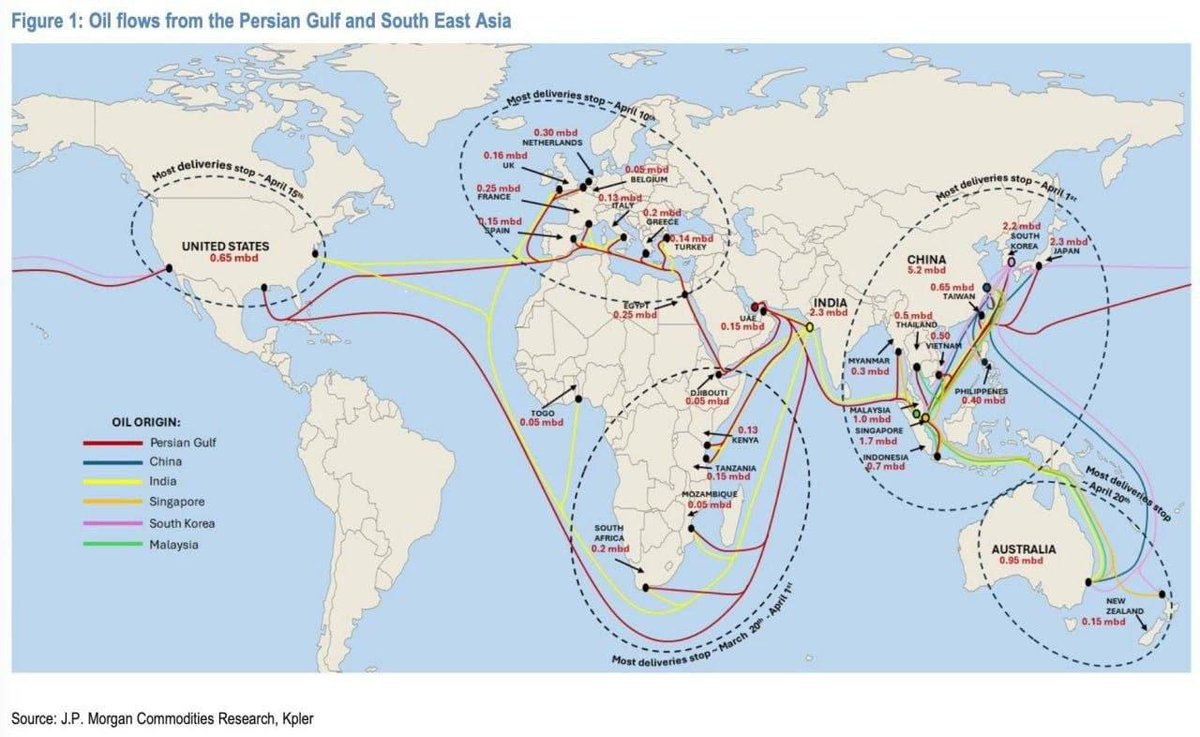

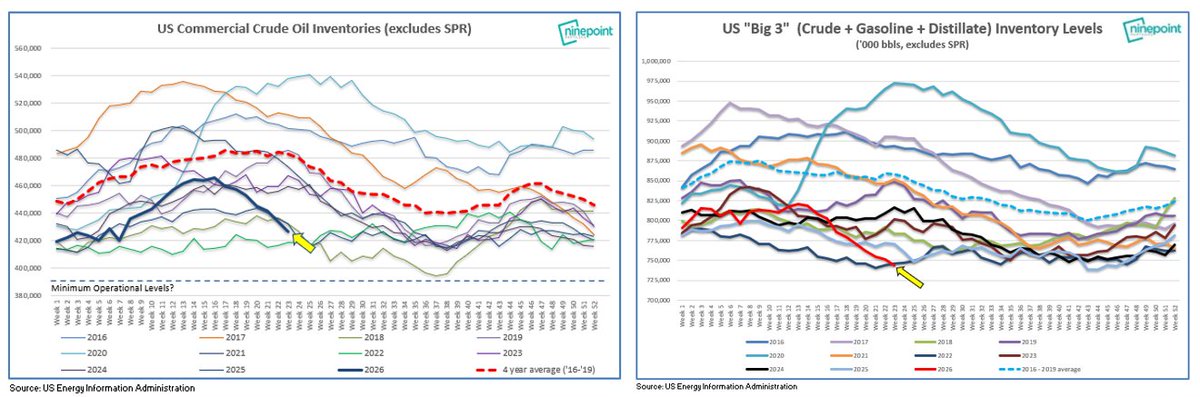

Oil strategists keep raising alarms over shrinking oil reserves. Carlyle's Jeff Currie: "It is robbing Peter to pay Paul -liquidating the buffer built over decades to suppress the very price signal that would trigger the investment response the mkt needs" https://t.co/tXF2pWyUo6

The "battle for the barrel"™️continues with US Big 3 inventory levels hitting their lowest seasonal levels in modern history. Tank bottoms and US SPR minimum operational levels both to be reached in July.

A história Ambipar/Master é a maior engenharia financeira da história do Brasil

Ação da Ambipar saiu de R$ 8,80 pra R$ 76. Alta de 863%. Compras coordenadas de três fundos ligados ao Banco Master

O esquema: Tércio Borlenghi (dono da Ambipar), Nelson Tanure e Daniel Vorcaro (Master) inflaram a ação com compras cruzadas entre Texas I FIA, Esna FIP e Kyra

As ações infladas viraram garantia pra Tanure comprar a privatização da Emae por R$ 1 bilhão. A XP exigiu R$ 760 milhões em colateral. Sem inflar a Ambipar, não tinha como fechar

A CVM chamou de "troca de favores"

Resultado: Ambipar desabou 99,46%. De R$ 76 pra R$ 0,41. Em um único dia caiu 61%

Quem tomou o prejuízo? Fundos de pensão. Rioprevidência (RJ) colocou R$ 150 milhões no fundo Texas. Amprev (Amapá) colocou R$ 30 milhões 10 dias antes da ação começar a cair

Vorcaro está preso desde março. Master foi liquidado. Ambipar em recuperação judicial. Tanure perdeu a Emae

Thank you to @zerohedge for inviting me on to join @AshBennington and @ArjunNMurti for a great discussion on US oil reserves and where we are headed.

Long before Iran, we were already seeing the consequences of years of underinvestment across global energy and commodity supply chains. Spare capacity has become increasingly concentrated, inventories remain tight and physical markets are far less resilient than many assume.

The Iran War didn’t create these conditions, it exposed and accelerated them.

Este é um tema q venho trazendo para os estrategistas. Mas ainda não recebi resposta clara. Na verdade a maioria não pensou nisto ainda, o q já é um sinal preocupante. Estamos com a cautela devida para este risco.

THIS IS HOW AI BUBBLE ENDS.

SpaceX, OpenAI, and Anthropic are all racing to IPO at the same time.

The market needs to come up with $200 BILLION in fresh capital to absorb them.

That money has to come from somewhere.

Large funds will start selling their biggest tech positions to free up cash.

NVIDIA, Microsoft, Google will be the first to get sold.

The problem is, those three names are carrying the entire S&P 500.

When they drop, everything drops.

This exact setup played out during the COVID-era IPO wave.

Rivian, Coinbase, Robinhood all went public at absurd valuations.

When the Fed tightened and liquidity disappeared, every single one crashed over 80%.

AI and tech are already stretched thin.

A $200B capital drain on top of that creates a forced liquidation event.

If you've been following me, you already caught the $16k bottom and the $126k top.

Missed those calls? The next one is coming.

Follow me and turn notifications on.

🚨 SOMETHING VERY BAD IS HAPPENING

The stock market keeps trying to push higher.

OpenAI and Anthropic are now worth $2.1T.

That is 10% of the entire Nasdaq.

Look at the math:

– $450B burned per year

– $50B in actual revenue

The entire AI bull case depends on one assumption:

Inference gets cheaper.

That is how funds justify the math.

Spend massively today, scale later, margins explode when inference costs collapse.

But that assumption is breaking:

- Memory is getting expensive.

- Compute is not getting cheap fast enough.

- Inference is not falling the way everyone modeled.

And if inference does not get dramatically cheaper, the whole AI margin story starts to crack.

The loop is obvious:

– Big players fund each other

– Partnerships look perfect on paper

– Revenue moves around inside the same system

Everyone calls it growth.

I call it the final stage of mania.

In 2000, companies added “.com” to the name and valuations exploded:

– Small profits

– Massive valuations

– Perfect stories

Then reality hit.

Nasdaq collapsed 80%.

Now companies add “AI” to the name and reprice instantly:

– Small profits

– Massive valuations

– Perfect AI stories

This is the dot-com bubble with better AI branding.

And bubbles do not warn you before they break.

They break when everyone thinks the story is untouchable.

The next move won’t wait for you.

Follow and turn notifications on.

EXPECTED TERMS IN "FINAL DRAFT" OF US-IRAN AGREEMENT:

1. Immediate and comprehensive ceasefire on all fronts

2. All parties mutually agree to refrain from targeting infrastructure

3. Freedom of navigation in the Persian Gulf and the Strait of Hormuz is guaranteed under a "joint monitoring mechanism"

4. Sanctions will be "gradually lifted" in exchange for Iran's compliance with the terms of the deal

5. Negotiations on outstanding issues will begin within a maximum of 7 days

6. Iran's President Pezeshkian is leading efforts to restrain the IRGC from overstepping on political and diplomatic policy-making

The agreement is expected to be announced within the next "few hours."

Turn on our post notifications @KobeissiLetter, we will be bringing it to you first.

Pakistani officials are reportedly brokering the deal.

‼️Foreign investors are DUMPING South Korean stocks at a record pace:

Overseas funds have sold a net ~$48 billion of South Korean equities so far in 2026, on course for the largest annual outflow on record.

Foreign investors have posted net sales of $11.5 billion in May alone, putting this month on track for the 3rd-largest monthly outflow on record.

This comes as the 2 largest monthly outflows on record both occurred earlier this year, in February and March 2026.

To put this into perspective, year-to-date outflows are more than DOUBLE the sales seen in Indian equities over the same period.

This comes despite a +87% rally in the Kospi this year, the strongest performance of any major global market tracked by Bloomberg.

Foreign capital is exiting one of the world's best-performing markets at an unprecedented pace.

Markets in Taiwan and South Korea are making history:

The total market cap of Taiwan's stock market is up to a record $4.5 trillion, surpassing Canada’s $4.4 trillion for the first time.

Taiwan’s stock market value has also exceeded that of the UK for the first time 2 weeks ago.

This comes as Taiwan’s market cap has surged by +$2.7 trillion or +150% over the last 12 months.

At this pace, Taiwan could overtake India and become the 5th largest world market as soon as next month.

Meanwhile, South Korea's stock market cap is up to a record $4.1 trillion, having overtaken the UK last week, and on track to surpass Canada this month.

Collectively, the two markets have added +$4.6 trillion in market value over the last 12 months, driven by AI-related stocks.

AI is transforming Taiwan and South Korea into a global economic power.

🛢️ Oil up 45%📈

So why is Exxon losing money while BP is up 20%?

Think of it like 2 traders during a storm.

@bp_America doesn't own much of the infrastructure that got damaged its oil production isn't heavily tied to Hormuz or Qatar.

But it has one of the best oil trading desks in the world. When prices go haywire, BP's traders make money on the volatility itself buying cheap, selling expensive, profiting from the chaos without being stuck in the middle of it.

Q1 trading result: "exceptional"📈

@exxonmobil is the opposite. It has roughly 5 times more Gulf production affected than @Chevron . Its Qatar LNG stakes some of the highest-margin barrels in its portfolio are trapped behind Hormuz.

Higher prices help, but Exxon has real operational damage at the same time.

The 2 numbers Bloomberg confirms:

BP: +20% since the war started

Exxon: −1 to −2%

Brent crude: +45%

Other European majors are outperforming US peers broadly, but BP is the clear standout cheaper valuation going in, trading machine built for exactly this kind of dislocation, and limited direct exposure to the region where the damage is concentrated.

Same crisis. Completely different outcomes depending on where you sat when the Strait closed.

the next trade that is making winners and loser is in the below comments

Totvs segue radioativa no mercado, mesmo com o pick up recente de US software (dados são PE 12m fwd). Múltiplo voltou para a mínima da década de 10, qdo a empresa estava cheia de problemas. Seguimos observando e tirando as lições. Não dá para comprar com tanta incerteza. Água turva precisa decantar...

“Brazil, the new gold?” is the title of the latest report published by Bank of America.

It’s been a while since I’ve seen something like this - probably not since the early 2000s.

$EWZ

Importante mapeamento de nossas fontes de suprimento de fertilizantes. Mais um choque duro para nosso agro. Alta de grãos está contratada. E com seus impactos a inflação.

Segunda começará com nova rodada de aumento de prêmio de risco global e provável nova alta do pretróleo. Mas o Bz é um dos portos seguros dentre os EM em petróleo.

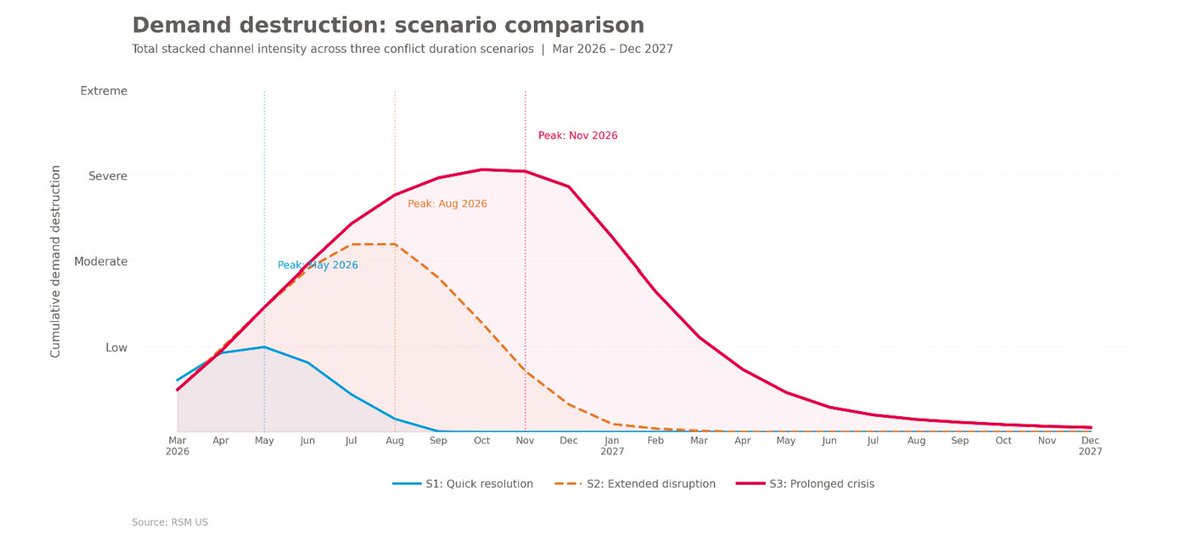

How does demand destruction work?

First, when oil prices spike, it acts like a tax on every household and business in the country. Americans collectively spend hundreds of billions of dollars more per year on gasoline and energy—and that’s money they’re not spending on other things. Economists call this the "purchasing power drain." But the damage doesn’t stop there. It triggers a chain reaction.

Second, confidence falls. People see gas prices rising, hear bad news about the economy, and start to worry. They cut back on discretionary spending—dining out, travel, shopping. Historically, consumer confidence has dropped 20% to 30% within two to three months of every major oil shock.

Then, big purchases freeze. Cars and homes are the most sensitive categories. When people are worried about the economy and paying more for gas, they put off buying a new vehicle or signing a mortgage. Hamilton (2009) showed that falling auto sales were a significant cause of the 2008 recession, separate from the financial crisis.

Next, businesses feel the squeeze. Diesel above $5 per gallon raises the cost of shipping everything. Companies respond by delaying investments, freezing hiring and eventually cutting staff—especially in transportation, manufacturing and agriculture.

Then the Fed gets involved. If oil-driven inflation forces the Federal Reserve to raise interest rates—or even just to hold them higher for longer—it makes borrowing more expensive for everyone, deepening the slowdown.

But if the Fed does nothing, inflation could spiral. This is the classic stagflation dilemma, and there’s no clean answer. If the situation becomes more severe, the Fed will act. But we think more likely than not that the Fed remains patient and when it does act it will be behind the curve, adding further pressure on demand before cutting aggressively.

Finally, if prices stay high long enough, people change their behavior permanently. They buy electric vehicles, lock in work-from-home arrangements, invest in energy efficiency. After the 1979 oil shock, U.S. oil consumption took nearly a decade to return to pre-crisis levels. This kind of demand destruction doesn’t reverse when prices come back down.

On top of all this, the commodity channels—food prices rising because fertilizer is scarce, chip production slowing because helium is unavailable, industrial costs climbing because sulfur and natural gas are disrupted—add another layer of pressure that standard oil-GDP models completely miss. These channels also have the longest tail: Even after shipping through the Strait of Hormuz resumes, the physical damage to gas plants, refineries and fertilizer facilities takes months or years to repair.