Merry Christmas! Here are my top investment ideas for 2026. $EOSE $LMND $TSLA $INV $OPEN $PATH $IREN $AMD $MAIA $COIN. Ordered largest planned allocation to smallest. Might change my mind at any moment. NFA DYOR.

$INV @AccelsiusATX

Datacenter operators are realizing they need to appeal to the public via not using water and paying for all their own power. This is a huge tailwind for Accelsius as 2 phase cooling uses no water and saves a lot on energy costs.

This is bigger than most people have understood it to be. The long term idea is that your “home is your bank and your bank is your home” is coming true. @betrmortgage is creating a frictionless interface to access your home equity in a programmable way that works across all commerce interfaces, while capturing transaction costs and rebating that to the consumer, for us and all our Tinman platform partners. $BETR

Today at the 4th Annual Liquid Cooling Workshop at Data Center World DC, our CEO Josh Claman joined industry experts to discuss building smarter and scaling for future chip demands.

Two-phase direct-to-chip (2P D2C): Better today. Required tomorrow.

$inv ticks every box:

✅Large and Growing Total Addressable Market (TAM): The opportunity must be massive and expanding, ideally in the tens or hundreds of billions.

✅Physics-Changing Technology: The innovation must fundamentally disrupt the industry-superior performance, cost advantages, or new capabilities.

✅Glow-in-the-Dark Management Team: Exceptional, battle-tested leadership with proven execution

✅No Entrenched Dominant Competitor: The space should lack a clear leader, giving the company room to capture share

✅Well Capitalized: Strong balance sheet to fund scaling without excessive dilution

✅Experienced Board of Directors (BOD): Seasoned advisors who provide strategic guidance

Full credit to @joceyreyes209, originator of the SuccessCriteria™️

$INV is currently my largest position. This very thorough report makes the case for what I consider the best risk/reward investment opportunity right now.

We are overstimulated and we don't even notice. Netflix while eating. Reels in the bathroom. Music while cooking. Podcasts on walks. We consume by default, not by intention. You keep filling every gap, then wonder why you feel foggy and unmotivated. Boredom and silence are the real growth drivers. They give you space to think and create. That's when solutions show up for problems that have been stuck for months. Leave some room.

$INV

Still wrapping my head around how cheap Accelsius is potentially trading.

Giving me very early $eose sub 1$ vibes. Very small downside with no lid on potential upside

Accelsius CEO Josh Claman quote from the start of this year “If 2025 was the year of proof, 2026 will be the year of scale. The industry is crossing the chasm from pilot to production. Hyperscalers and Neoclouds are no longer asking whether two-phase cooling works—they’re asking how quickly it can be deployed across global portfolios”

First off some figures, comments and assumptions

-Pipeline $1b, +400m QoQ

-Pipeline is 8x the 2026 revenue plan. Implies upper bound of $125m for revenue. 50% haircut say 60-70m revenue for 2026

-INV ownership in Accelsius ~43% (https://t.co/JfKclEd8x1)

- Opex est is in the $35-40m range. (Based off an annualised Q3 number and my model)

- Cash Flow positive in 2026 (https://t.co/rFsnr3oKLq)

- Potenitally full funded (https://t.co/rFsnr3oKLq)

I can’t imagine fixed costs are much higher than 2025 were. Don’t see a large increase Employee cost and R&D costs into this year which are the biggest drivers

If Accelsius books 1 or more significant orders this year and starts to convert pipeline to backlog in 2026 then can start to price in some 2027 revenue

What I am playing for - 2027 EBITDA of $200m

2026 EBITDA positive with fixed costs of $35-40m and revenues of potentially $70m-125m

But really it's when you start pricing in 2027 things start getting spicy.

I think there is a path to upwards of $4-500m in 2027

With Gross margins in the 45% ish range and opex of ~$45m

2027 Base case EBITDA of $100m with a 30x multiple =$3b EV for Accelsius.

2027 Bull case EBITDA of $200m with a 30x multiple

=$6b EV for Accelsius.

2026 Base case target is $15/share for INV

Write the other 2 companies at 0 for INV and the market is pricing Accelsius at $600m. Reality is the current market valuation is even less than this if you ascribe some value to the other 2 companies in the INV portfolio (AeroFlexx and Refinity)

So currently priced at 2-3x nexts years cash flow. CHEAP!

2026 is about orders - product validation

Innventure management addressed some of the immediate risks around parent level dilution and corp governance here: https://t.co/SOQi6rPxDO

Essential they are aligned and see the same huge potential in Accelsius too.

$INV ACCELSIUS

These are the key catalysts I see that will unlock value at Accelsius

Catalyst 1 (Most Critical): A Named, Large-Scale Production Win.

The single most powerful near-term catalyst is a publicly announced, sizeable production deployment from a hyperscalers/neocloud or reputable name

Catalyst 2: JCI/Legrand Commercial Revenue Begins Flowing.

It was deliberately structured as a commercial partnership. These are the two largest global players in data center infrastructure services: JCI dominates North America, Legrand dominates Europe. Management explicitly said to expect "commercial activity and commercial rollouts in conjunction with JCI and other partners over the course of the next few quarters"

Catalyst 3: Cash Flow Positivity at Accelsius

Based on the latest PR from INV Accelsius is projected to be cash flow positive by YE 2026.

"Accelsius is well capitalized and potentially fully funded"

Catalyst 4: The "Technology Skip" Moment

CEO made a bold and insightful observation: with ~80% of North American data centres still air-cooled, the market may skip single-phase water entirely and jump straight to 2P DTC cooling.

Some early adopters of single-phase water are now experiencing poor results (leaks, high flow rates, thermal headroom issues with next-gen chips)

The Eos Trilogy - A three-part story about vision, hype, and reality.

Act I: The Dream

The grid needs storage.

Not 2-hour lithium packs.

Multi-hour, grid-scale storage that can support renewables.

Eos shows up with something different:

Zinc batteries.

No lithium.

No cobalt.

Non-flammable chemistry.

A bold pitch:

Build the backbone battery for the future electric grid.

Investors loved it.

The stock ripped.

⸻

Act II: The Hype

Then came the projections.

Factories would ramp quickly.

Margins would inflect soon.

Revenue would explode.

Every quarter the future looked brighter.

Until reality arrived.

Hardware companies don’t scale on PowerPoint.

Manufacturing is brutal.

Ramps take longer.

Costs come down slower.

Execution matters.

Expectations broke.

The stock collapsed.

⸻

Act III: The Facts

Now ignore the promises.

Just look at what actually happened.

Revenue:

2024: ~$15M

2025: ~$115M

2026 guide: ~$300M

That’s 20x growth in two years.

Factories are running.

Product is shipping.

The market exists.

The irony?

If management had simply said less…

The market might be celebrating this growth story instead of punishing it.

⸻

The real problem

Eos doesn’t have a technology problem.

It has a credibility problem.

But credibility can be rebuilt.

Factories.

Margins.

Execution.

Those are louder than any earnings call.

And if the ramp continues…

The final act of the trilogy might still surprise people.

Coming to your local theaters in 2027

$EOSE

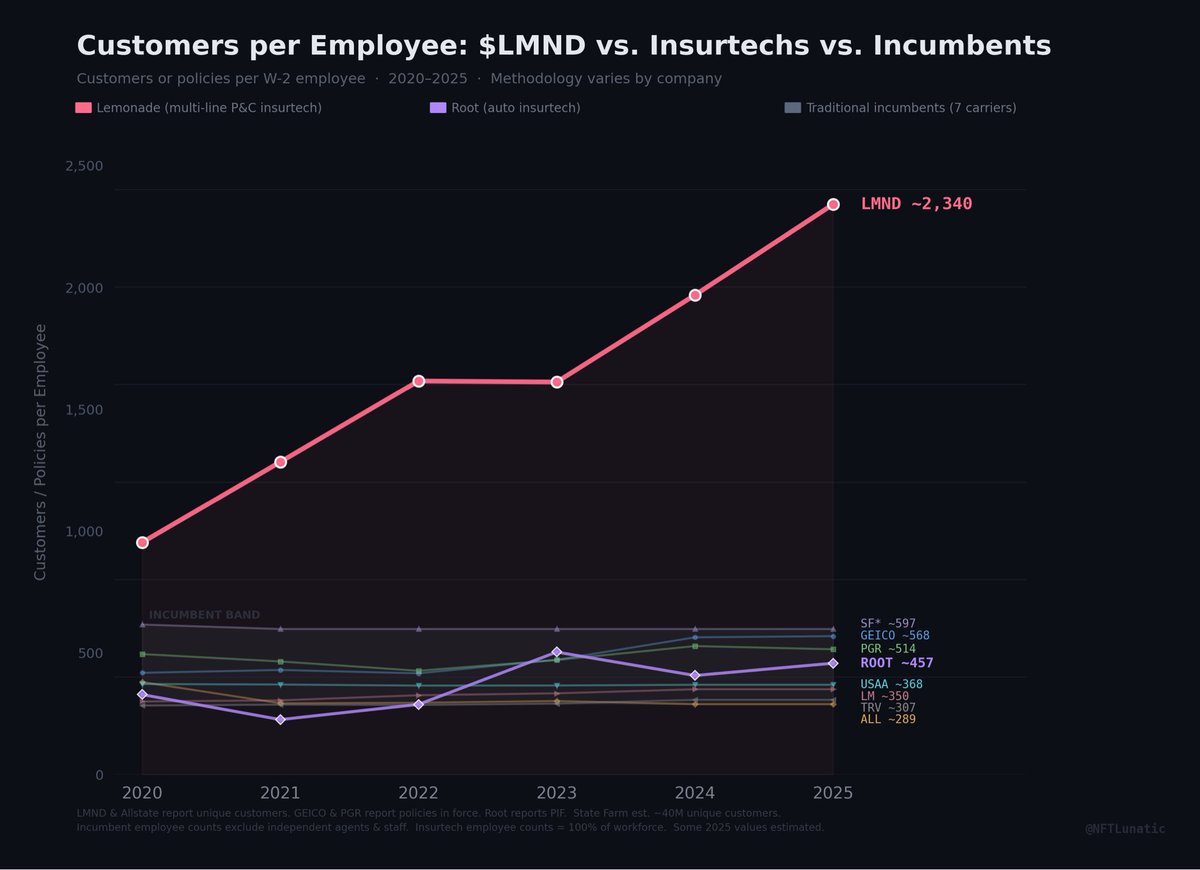

"Isn't $LMND just another insurtech?"

This chart can lay that argument to rest.

Customers per employee, 2020–2025:

$LMND vs. $ROOT vs. 7 major incumbents.

$ROOT is the perfect test case. Same era. Same "insurtech" label. Same direct-to-consumer P&C model. Public company with clean data.

$ROOT at 457 customers per employee.

GEICO at 568.

Progressive at 514.

Root IS the incumbent band.

Why? $ROOT innovation was telematics — better pricing through driving data. That helped them reach profitability. But it didn't change how many humans they need to operate.

Root hired 341 people last year to add 73K policies. $LMND hired 47 to add 570K.

That's not a difference of degree. It's a difference of kind.

$LMND didn't just digitize the front end. AI Maya underwrites. AI Jim handles claims. The marginal customer costs almost nothing to serve.

$ROOT used tech to price better. $LMND used AI to run the company.

That's why one curve compounds and the other flatlines.

This also kills the bear argument that competitors will "just copy $LMND playbook."

$ROOT has been trying for 9 years. Backed by $1.2B+ in funding. Public since 2020. Building technology from scratch with no legacy constraints.

And they still ended up in the incumbent band.

If a well-funded, tech-native insurtech with zero legacy baggage can't replicate this efficiency curve, what makes anyone think State Farm or Allstate will?

$LMND AI-first architecture isn't a feature. It's a compound advantage that gets harder to replicate every quarter — because every new customer, claim, and interaction feeds the models that make the next one cheaper to serve.

The moat isn’t JUST the AI operating system running the company. It’s 3 million customers (and growing) training the AI.

Okay, this is really simple.

It feels like a gut punch to have the stock climbing and then dramatically fall.

Emotionally/psychologically it hurts.

BUT,

If you zoom out, it's very simple where we're at.

$LMND just posted their best quarter ever.

They can invest dollars into growth and get a 3 to 4x return on those dollars.

This means they can invest in growing the top line 30%+ while keeping all other expenses growing near flat or in single digits.

This means extrapolate this out a few years in the giant insurance market that they're in and discount it back today and they are worth $150 to $250 today.

All while we are at a time of transformational AI being introduced and improved day by day, week by week.

All while Lemonade is protected against start ups and legacy insurers through regulation, their 10-year-head start, AI/Digital-first culture and infrastructure, capital needs secured and data flywheel turning.

All while the market will sell us shares at less than half of the lower fair value.

So what does this all mean ... where are we at?

We are at accumulation time.

We are at a time to take advantage of this buying opportunity.

My mindset is to buy as many shares as I can over the coming months until we see another rerating upwards.

I've absorbed the gut punch and this is just psychologically how I am thinking about the OPPORTUNITY.

This is not financial advice. Do your own due diligence.

Presenting @Lemonade_Inc’s Q4 2025: our strongest quarter ever!

Recommended: Play this while reading- https://t.co/jHFp0vsNcn

Highlights (Y/Y)

🚀 9th consecutive quarter of accelerating growth

💵 $1.24 billion top line (+31%)

🔥 Revenue: up 53%

🔥 Gross profit: up 73%

🔥 Cash flow: generated $37m (adj. FCF)

🔥 ~3m customers

🔥 Adj. EBITDA loss improved 81%, now just -$5m

Car and Autonomous

✅ Lemonade Car grew 53%, now at $187m

✅ Loss ratio: 70% (TTM, down 23 points)

✅ Launched Autonomous Car Insurance for @tesla FSD (Supervised)

Europe

✅ Grew 150%

✅ 10th consecutive quarter of triple digit growth

✅ Loss ratio: 64%

AI Spotlight

✅ In the last 13 quarters- headcount shrunk 6%, while adding 1.2m customers

✅ 68% reduction in Pet cost-per-claim: from $44 in 2021, to $14 now

✅ Claims LAE at a record 6% (vs. 9% industry avg.)

More...

✅ Record breaking LMND gross loss ratio: now at 52%

✅ Growing cash (and investments) in the bank: $1.12B

Up next

⬆️ Guiding to 32% IFP growth in 2026

⬆️ 60%+ revenue growth

⬆️ Q4 2026 first positive adj. EBITDA quarter, 2027 - full positive year

⬆️ Announcing our upcoming investor day @ NYC, Nov ‘26.

Full details + financials: https://t.co/gDgJGSVuac