@Brian_Stoffel_ I own the stock too but man do I worry about valutaion. I like the optionalities and all the growth vectors. But those are somewhat priced in too.

I like Tobi and Harley too, +2 points!

Adobe บอกว่าเพิ่มผู้ใช้งานเป็นเกือบพันล้านคน ผมเป็นหนึ่งในผู้ใช้งานนั้น เพราะผมสร้างรูปทีมในแอป Fantasy Premier League ที่บังคับใช้ Adobe AI Gen รูปให้ (เจนได้กากมาก 555)

หวังว่า Active User อื่นจะไม่ใช่แบบผมนะ

$ADBE CFO Dan Durn at yesterday's investor update: "Adobe, we're operating at scale, and we're doing it from a position of strength. We've got over $26 billion of ARR, and we're delivering double-digit customer group subscription revenue growth.

But at the same time, we're seeing strong momentum from our AI-first solutions, with ending ARR more than tripling year over year.

And if you take a step back and look at the demand signals, the signals are clear. We're seeing growth across our user base. We've got over 850 million monthly active users, and that's growing 17% year over year.

Just think about that. But over 850 million monthly active users, we're touching greater than 1 in 10 people on the planet each and every month in the Adobe ecosystem. And that's growing greater than 17% year over year. That's a significant addressable market.

But engagement, engagement's increasing, credit consumption, credit consumption's increasing. And that's the clearest signal that you see of customers who are embedding AI into their creativity and productivity workflows.

And that's translating directly to growth of the Firefly family of solutions.

And in the enterprise, we're helping their customers. We're helping our customers transform how they operate in the era of AI. And we have three solutions now. Each of them is greater than a billion dollars.

And in the aggregate, those three billion dollar businesses are growing greater than 20% year over year. That is incredible growth at that scale.

And I think it illustrates and underscores both the importance and differentiation of our content supply chain solutions, our customer engagement, and our brand visibility."

Thanks for the post! Do you think they will face more pressure in the future? There is https://t.co/on1yjfR0ke and airwallex and others adjacent which could encroach into Adyey’s territory. They are growing much faster and taking incremental share of payment volume.

Also does approval uplift has a ceiling? once the tech got good enough/commoditized enough, their uplift is not significantly higher than competitors? Thanks!

I don't see this get discussed much..

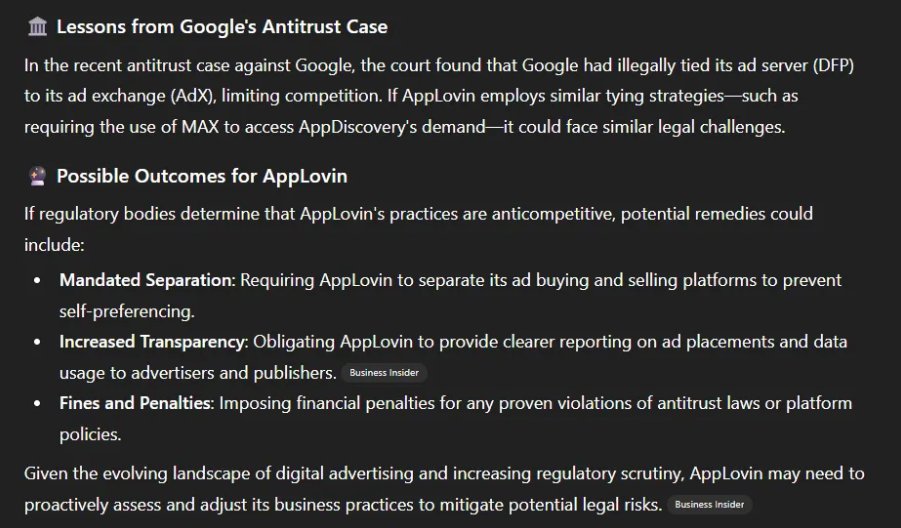

Can $APP be sued for favoring it’s own product that cause unfair advantage in the competition by waiving Publishers who uses both Max and Appdiscover 5% in mediation fee (small, but decisive as every % compound the monetization flywheel)?

Although game publishers still have the choice to user other mediation though. ChatGPT though told me that this practice could be illegal if the company is deemed as a monopoly in a “defined” market. Now this depends on how you define this. If you are talking about the whole digital ad space, then APP is just <5% of total ad spend. But if you talk about gaming only, then the number flipped to >50%. Anyway, if deemed illegal, any kind of mandate from the court will destroy the company’s moat. I don’t see this risk get mentioned in the public much though.

Anyone have any ideas? thanks!

Extreme bureaucratic regulatory oppression and wealth confiscation (moving capital allocation from highly competent entrepreneurs to incompetent government) is why Europe has been economically slowly strangled over the past few decades!

Fools like this guy do not understand that they are the cause of Europe’s pain.

There no wealth to reallocate when they prevent it from being created in the first place.

@peter_mantas@rebound_capital Can CSU deploy this agent? If not, is it becaue thier team is not good enough at AI or cluade dominate evey aspect? Or they can but at price so low because of more competition?

A finance team just sent us this. They ran a full budget vs. actuals analysis in under 5 minutes.

Uploaded their budget P&L and 10 months of GL actuals. Ramp Sheets matched every line item, calculated variances, and flagged problem areas.

This used to take half a day.

Anthropic uses Workday. OpenAI uses Slack. It’s incredibly clear to anyone with half a brain that nobody is vibe-coding critical infrastructure. It is genuinely the lowest EV activity you can do. That bear case is dead (to I think most sensible investors).

BUT, there are others. Here’s my remaining set of bear cases for SaaS, stack ranked. If you’re going to invest in SaaS you should be aware of all these and have a very strong POV on how impactful they are and the timeline on which you think they will (or won’t) play out

1. Platform differentiation trends toward zero, hurting CAC as each customer/upsell becomes a knife fight with multiple competitors. We were already trending toward every platform offering every app, AI just made it easier

2. Value will accrue to the agentic layer sitting on top of the system of record (SOR). Even with all their context, a SOR still lives in a silo

3. Investor sentiment becomes a structural headwind as revenue quality/business model is de-rated

4 . AI-native startups will deliver tremendous value at better prices, eating the incremental LTV of incumbent customers

5. As Agents do more work, seat-based revenue will decline.

6. Legacy SaaS will struggle to transition from seats to outcomes

7. Diminished pricing power due to decreased differentiation and lock-in takes away yet another growth lever

8. Gross margins will deteriorate because AI revenue is structurally more expensive which hurts the value prop of the business model

9. Decreased organic traffic due to LLM adoption increases CAC

10. Competition for scarce AI talent increases SBC/opex faster than revenue as incumbents fight to keep A talent from AI-native companies

@MikeLongTerm@Meta Except from lacking capacity and pricing elsewhere, why would one go with meta cloud instead of more established clouds with all the tools?