Great @iancassel piece on letting your losers get smaller. One thing I'd add: shrinking a loser is the right default — but it's a default, not a law.

The Verdun trap Cassel describes — sunk cost, ego, wanting to be right more than wanting to make money — is what happens when you add to a loser on feeling. The cure isn't "never add." It's being brutally honest about whether you're acting on fresh conviction or defending an old decision. You earn the right to override the default only through rigorous research into the company. Sentiment, partial information, and "it should be working by now" don't count.

Two examples from my own book, pulling in opposite directions:

$VEEV: the market wanted to treat it as AI roadkill. My work said the opposite — not a company being disrupted by AI, but one positioned to benefit from it. The financials and independent expert coverage confirmed it. So I added. That's a legitimate override: I wasn't adding to be right, I was adding because the research said the thesis was getting stronger as the price fell.

$SPWR: I had genuine conviction here, anchored in TJ Rodgers' track record of building real businesses. But a deep look at the capital structure — plus conversations with investors I respect — told me to sell at a loss. That doesn't mean $SPWR fails. I just don't believe it works soon, and "eventually" carries an opportunity cost I'm not willing to pay.

The discipline cuts both ways. Sometimes the research tells you to add to the "loser." Sometimes it tells you to exit a name you still believe in. The one input that should never drive the decision is the price you paid.

Let your losers get smaller — unless you've done the work to earn the right not to.

New Article - Letting Your Losers Get Smaller

It takes just as much discipline to hold a winner as it does to not add to a loser.

https://t.co/WHouaF6rJu

@StoryTrading@SpaceX I am a big fan of your work! I was wrestling with the same idea over last few weeks, you may want to check my thoughts summarized here https://t.co/t53IcuryBA

D-BOX $DBOXF $DBO.TO just reported a milestone year 🎬

The company that makes motion-synced theater seats finally hit escape velocity. Revenue up 35%, profitability up 100%+, and the high-margin royalty stream is growing 5x faster than the underlying box office. The writing is on the wall - they're winning share, not just riding a tide.

I'm focused on this latest print since the broader story is already well-covered by independent analysts like @BreakoutInvestr and @WolfOfOakville, so I am pointing you there for the full thesis.

The balance sheet doubled to C$17.6M cash (~US$13M) cash with virtually no debt. At ~11x EV/EBITDA, you're paying a perfectly ordinary multiple for a business in operating-leverage inflection.

The strategic tell: management is openly positioning to bankroll D-BOX installations at cash-strapped chains like AMC and Regal. 7 of the top 10 North American exhibitors are still untapped. That's the runway.

Risks worth owning: half the installed base sits at one customer (Cinemark), the slate cycle is real (last two quarters showed it), and liquidity is thin. The deferred tax recognition flatters reported earnings - normalize for it.

I'm long, sized small, and watching the next two prints.

Not investment advice. I hold a position and may add or trim without notice. Microcaps cut both ways — please do your own work.

$SIVE

This stock is being pumped heavily by accounts that do nothing but pump stocks. The below press release does not reflect any revenue commitments but is basically just a PR piece coming from a firm that's understandably engaging in a money grab off the back of being pumped relentlessly. Buyer beware!

Everyone says space stocks are a bubble. After three weekends rebuilding the models, I think most people are wrong about which ones.

It's not one bubble. It's two completely different things wearing the same costume:

🚀Rocket Lab is a real company priced for near-flawless execution.

🛰️AST SpaceMobile is the purest scarcity bubble in the group - a gorgeous idea that doesn't fully exist yet.

Most of the rest is just expensive growth that normalizes once you do the work. (Quantum stocks at 700x sales are far crazier than anything in space.)

A few things that surprised me:

🌕 Intuitive Machines screens "cheap." But the cheap was bought, not earned — the revenue came attached to an acquisition.

🌌 Sidus Space loses money on its revenue before paying a single salary. Negative gross profit. I literally couldn't plot it on the chart.

✅The kicker: at its rumored ~$1.75T price, @SpaceX would list cheaper - on sales - than @RocketLab, and a fraction of AST. The best house on the block, priced below the fixer-uppers.

That's the whole catalyst. Once you can finally buy the real thing, why keep paying up for the stand-ins?

History rhymes here too. Glencore, Rivian, Coinbase all rang the bell when the category king went public. But it's a pattern, not a law, and I lay out exactly what would prove me wrong.

I also walk through how a careful person would actually play this. Hint: not by shorting these naked into a squeeze but with the real option structures, the borrow data, and the charts.

Full breakdown, free to read:

https://t.co/X9O1k7PO3e

$AVEX call on IPO day + post-earnings re-entry is just another masterclass from @MoneyMarkStocks.

Beyond the excellent picks and insane track record, what really stands out is the FREE financial education and professional-level analysis you consistently share.

Real value that actually helps people become better investors. Thank you for donating your time and expertise. 🙏💸

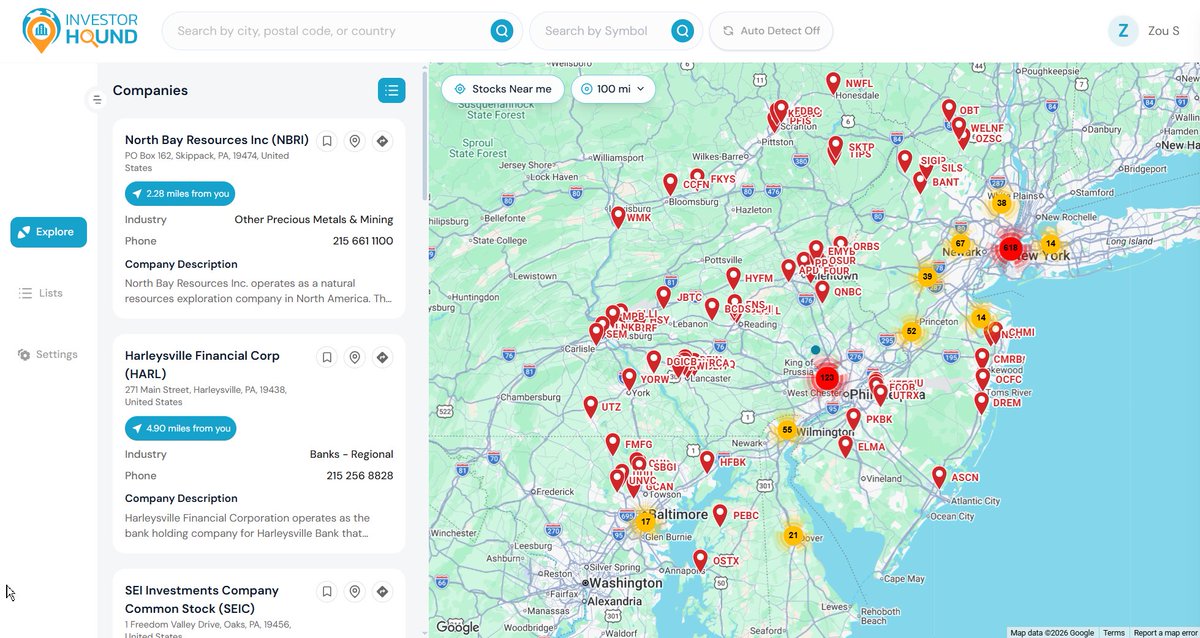

@MicroCapHound just showed there are 1,775+ public companies within 100 miles of him.

That’s an insane edge for site visits and real-world microcap research.

This is free and an absolute must for aspiring microcap investors. The kind of practical tool serious investors actually need.

https://t.co/M7CVi8BmLp

Well done🚀 InvestorHound is straight fire.

You have more public companies around you than you realize. I'm sure of it. https://t.co/mMKsJpdxOs.

At least 1,775 within 100 miles of me. You going to be in an area? Pick your site visits. Make a list.

Adding features, looking for feedback.

$TOYO ☀️Co-hosting with @GeoInvesting this Wednesday 11:15 A.M. EST Skull Session on $TOYO!

Solar manufacturer with a real tariff moat (operations in Ethiopia + Vietnam + Houston plant planned). Revenue exploded +142% in FY25 and another +177% in Q1 with big margin expansion and profitability swing.

Management just reaffirmed strong FY26 guidance.

Join us for the deep dive. Details in @GeoInvesting ’s post.

Macro dictates the playground, but microcap is where the mispricing lives, especially in Energy and Infrastructure.

Most investors ignore this space because it requires actual digging. As a Ph.D. economist with 20 years in global macro, digging is what I do. First deep dive drops soon. 📉⚡️🏗️