Warren Buffett: "[Charlie Munger] has been the person, subsequent to my dad, that I didn't want to disappoint. It's good to have somebody in your life you don't want to disappoint. It's enormously important. It makes you a better person."

1.1. Question 28: What happened 1973 and 1974 when your investment firm lost over half?

Charlie: Oh, that’s very simple. That’s very easy. That’s a good lesson. That’s a good question. What happened is the value of my partnership where I was running, went down by 50% in one year. Now the market went down by 40% or something. It was a once in 30 year recession. I mean monopoly newspapers are selling at 3 or 4 times earnings. At the bottom tick, I was down from the peak, 50%. You’re right about that. That has happened to me 3 times in my Berkshire stock.

so I regard it as part of manhood. If you’re going to be in this game for the long pull, which is the way to do it, you better be able to handle a 50% decline without fussing too much about it. And so my lesson to all of you is conduct your life so that you can handle the 50% decline with aplomb and grace. Don’t try to avoid it. (applause) It will come. In fact I would say if it doesn’t come, you’re not being aggressive enough.

1.2.

“I regard it as a part of manhood. If you’re going to be in this game for the long haul which is the way to do it. You better be able to handle a 50% decline without fussing too much. Conduct your life so you can handle a 50% decline with aplomb and grace. Don’t try to avoid it. It will come. And if it doesn’t come I’d say your not being aggressive enough”.

@BrownMarubozu Thanks for sharing! Still not obvious to me just because insurance subsidiaries have cash would mean the notes proceeds are for buyback… I hope they buyback too!

@BrownMarubozu Could you explain why does it matter whether the cash sits at holdco vs subsidiaries? Do you mean the notes proceeds can’t be channeled toward investments in the subsidiaries? That would be very odd to me.

Btw also noted they had redeeme C$450m notes at 4.7% recently too

Speculative growth appetite is back near bubble-era peak levels.

Valuation dispersion is wide again. Historically, some of the best future relative returns for profitable small- and mid-cap value stocks have emerged when investors become most enthusiastic about unprofitable growth.

What is the difference between a patient investor and a stubborn one?

A patient investor is in scientist mode. His position is a thesis, and he actively seeks out disconfirming data.

A stubborn investor is not just trying to be right. He is obsessed with not being wrong. He is sticking to the decision because he made it, because it is his.

A patient investor's process is a living organism, in a constant state of betterment. A stubborn investor's process is rigid, rarely updated, and completely cemented on outcome.

Here is the uncomfortable part: from the outside, the two are hard to tell apart. Who you are as an investor is only for you (and maybe your psychologist) to know.

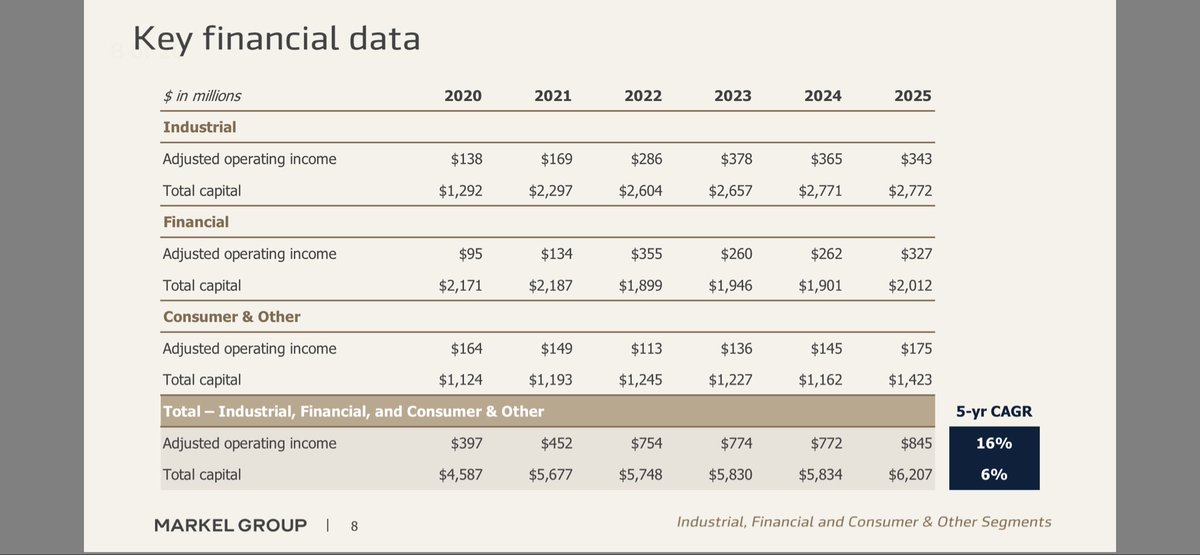

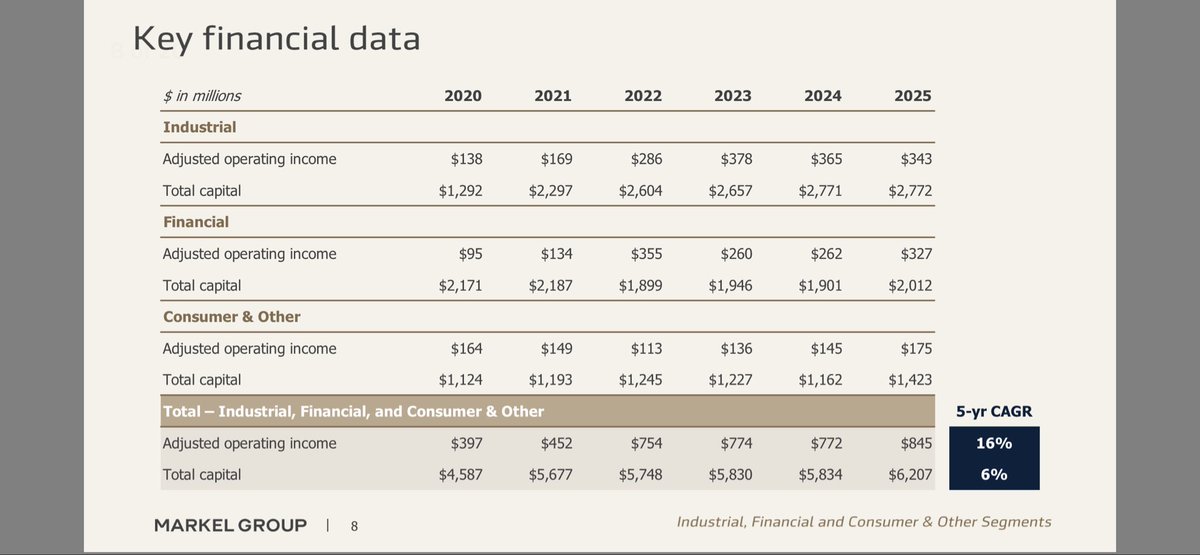

@MichaelGielkens They showed adj op income and total capital in the main presentation? The appendix serves to explain the underlying economics of the businesses

@QualityCap0@MichaelGielkens In the main slides they already showed adj op income and total capital of 13-14% which reflect their capital allocation return. I think the appendix serves to illustrate the underlying economics of the businesses.

Every investor would love to find the next Mark Leonard.

Imagine it is May 2006 and, to provide liquidity for institutional investors, Constellation Software is going public. You hear about its genius CEO and invest, compounding your investment at more than 30% for the next 20 years. That single decision makes you a fortune.

Because we know how the story ends, we revise history. We look at Mark Leonard today, a legendary, towering CEO, and think, “I would have written that check.”

But let’s be honest: you wouldn't have. Almost no one would have.

Because the Mark Leonard of 2006 looked nothing like the man we know today.

There was no track record, just a former gravedigger and venture capitalist with an unconventional idea to buy dozens of obscure vertical market software companies. Wall Street was skeptical. The consensus view said these were dying businesses and the model would not scale.

Leonard himself was a ghost. There were few articles written about him. He didn’t give guidance or host earnings calls. The annual meeting was a small, formal affair. Few investors knew what he looked like; Google searches came up empty. Constellation’s website was terrible.

To many investors, not participating in these rituals was suspicious. It was easy to come to the conclusion that Leonard was hiding something.

But Leonard liked it this way. He was confident and understood companies get the shareholders they deserve. Without being promotional, he provided enough information so that investors could make up their own minds about Constellation’s stock.

The irony is that when searching for the 'next' Mark Leonard, we look for what he looks like today, not what he looked like then.

We search for billionaires with impeccable track records and clean reputations. We like it when they grace magazine covers. We seek validation from others on Twitter - it will always be Twitter to me - and at cocktail parties.

But we should be looking for what they looked like then: eccentric but rational, and ignored by the masses.

It is hard to overstate how uncomfortable this is. It means looking foolish for years before you are proven right. And that is exactly why so few people ever find them.

My notes from the $CSU.TO $TOI.V $LMN.V 2026 AGM! It should serve as some good long-weekend reading!

Includes stuff that neither the financials nor the meeting recording will tell you!

I got a chance to speak with Mr. Jeff Bender, Mr. Bernie Anzarouth, Mr. Jamal Baksh, Mr. Daan Dijkhuizen, Mr. Robin van Poelje and shared what I remember!

I think the 4+ hour AGM is well worth your time but the 3-4 minutes of direct quotes get you 90% there!

YouTube link (with timestamps): https://t.co/X6BGy7scdW

Official link: https://t.co/UFzMxDqAvO

Random $CSU.TO AGM tidbits:

- Harris employees mentioned $CSU.TO has it's own inference hardware (capex), has access to it's own hosted models

- DeepSeek does provide good performance for 1/10th the price but more if on own HW

- AI early days, no "correct" yet

1/

The way a company reports earnings is an important tell. Here is how my latest investment does it:

•No advance notice of date

•Matter-of-fact earnings release

•No guidance

•No conference call

•Questions sent by email, answers posted on website

A traditional investor may think this reflects a lack of transparency.

I see something else: management focused on running the business, not managing Wall Street’s expectations.

This says a lot about what is happening behind the curtain.

Warren Buffett: "If you feel you have to invest every day, you're going to make a lot of mistakes. It just isn't that kind of a business. You have to wait until you get the fat pitch."