Clocks to Blocks:

Today's thread is based on the brilliant findings of @dpuellARK & @_Checkmatey_ - introducing a novel time based analytical approach.

Thread 🧵

https://t.co/qHikase8hJ

Bitcoin is the canary in the coal mine.

Since the October 10 peak, the Risk Index and VIX have moved in synchronization.

When market volatility rises, selling pressure accelerates inside Bitcoin. Why?

Because $BTC remains one of the most liquidity-sensitive assets in the market.

When liquidity deteriorates, Bitcoin often reacts first.

The February–early March phase was the harshest example:

→ Risk pinned at Capitulation

→ VIX spiking

→ BTC in free fall

But the key signal was not Risk reaching 100.

It was Risk peaking and then beginning to ease.

That was the first clue that liquidity was returning, selling pressure was being absorbed, and market stress was starting to fade.

Today, Risk is back at 100. The VIX has also reacted and briefly entered the Fear Zone.

The question now is whether both the Risk Index and VIX are warning of an extended period of volatility and downside pressure.

In other words: Is this just another stress spike?

Or is the broader market environment starting to crack again?

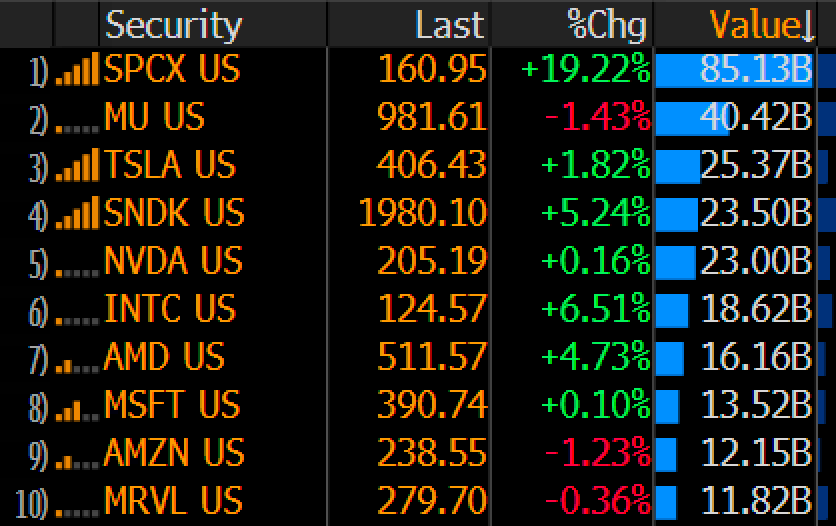

$SPCX ended up doing $85b in volume. Gargantuan number. Easily a record for an IPO and in the Top 10 all time for any stock on any day. For context, it's more volume than Apple has ever done in 40yrs. Nice job @StevenUhey he guessed the closest of anyone in my replies with $69b.

Citadel Securities just put institutional weight behind what the AI bulls won't say out loud.

In a new macro note titled "Tokenomics," Citadel makes the argument plainly: even the most powerful technology on earth still has to pass through the boring discipline of cost curves, capacity limits, and marginal returns.

The evidence is piling up:

– Amazon removed its token usage leaderboard

– Microsoft cancelled Claude Code subscriptions

– Multiple companies reporting unexpectedly massive token bills

Their conclusion is the part that matters.

Adoption is no longer about what AI can do in principle. It's becoming about the price and scarcity of the inputs needed to run it at scale. Compute. Power. Cooling. Memory bandwidth. Inference budgets. All real, all binding constraints.

And here's the kicker from the chart.

The Silicon Data LLM Token Expenditure Index, a benchmark for how much the market is actually spending on AI tokens, has started rolling over. Citadel reads it as a shift toward cheaper models. Companies substituting away from expensive frontier AI toward "good enough" alternatives.

That's economics 101 doing what it always does. When the price of something rises, people use less of it, or find a cheaper version.

Citadel sees a bifurcation forming. Frontier AI concentrated among a few firms with the balance sheets to absorb the cost. Everyone else quietly downgrading to simpler, cheaper models.

This is the part of every technology revolution the early narrative ignores.

The technology being real was never the question.

The question was always whether the economics could carry the valuations.

When one of the most sophisticated trading firms on earth starts writing about AI in the language of cost curves and rationing instead of limitless demand, the conversation has quietly changed.

The hype was about what AI could do.

The reckoning is about what it costs.

Stealing from the future 101. This 101 will attempt to describe facts. It is not political except to say that the outcome was entirely bipartisan. It spans 46 years of a wide variety of political alignments.

The big takeaway is every single member of society has benefitted

@HansCashFlow Thoughts on NBIX?

@HansCashFlow

IBIT has a good R/R right now, sent a LEAP order. Y low IV rank, well protected downside / > Pessimism. Scaling in on IBIT.

I recently read a quote by Soren Kierkegaard that stayed with me:

“Marry, and you will regret it.

Do not marry, and you will also regret it.”

At first, I thought it sounded pessimistic.

But the more I thought about it, the more I realized he was describing something deeply human.

The mind always imagines that happiness exists in the life we did not choose.

If you marry,

you may one day miss freedom.

If you stay single,

you may one day miss intimacy.

Every path gives something,

and every path takes something.

Maybe peace comes when we stop searching for a perfect life with no sacrifice.

@ZeeContrarian1 Very important point. Whilst volatility can create fragility, it can also create opportunity. So capping everything inversely to risk dilutes alpha. I do think discretionary traders like yourself benefit the most from this. When a story unfolds, the re-rating is powerful.

@ZeeContrarian1 I had to add a section in my trading journal called Z.

Every trade in the top 10 is now a Z trade for 25/26 lol.

Bless your soul for putting out such monumental content, helping both my trading journey and my families financial journey. Cant thank you enough sir. 🙏

@HansCashFlow For LEAPS, would you reccomend buying longer dated call spreads to reduce cost for smaller accounts?Diagonals / PMCC seem like a great choice, but when financing the short end, you risk vol expansion, which is why we bought LEAPS to begin with ? @HansCashFlow

@AahanPrometheus Perhaps the intelligence of LLMS has yet to exceed the top performers

in their subdiscipline, but I gotta say it does a great job decoding the likely path that got them there, algebraically. It doesn't have the magic formula, just the pebbles that guide you there.

Food for thought.

Trump, Hormuz and the End of the Free Ride

For half a century, Western strategists have known that the Strait of Hormuz is the acute point where energy, sea power and political will intersect. That knowledge is not in dispute. What is new in this war with Iran is that the United States, under Donald Trump, has chosen not to rush to “solve” the problem. In Hegelian terms, he is refusing an easy synthesis in order to force the underlying contradiction to the surface.

The old thesis was simple: the US guarantees open sea lanes in the Gulf, and everyone else structures their economies and politics around that free insurance. Europe and the UK embraced ambitious green policies, ran down hard‑power capabilities and lectured Washington on multilateral virtue, secure in the assumption that American carriers would always appear off Hormuz. The political class behaved as if the American security guarantee were a law of nature, not a contingent choice. Their conduct today is closer to Chamberlain than Churchill: temporising, issuing statements, hoping the storm will pass without a fundamental reordering of their responsibilities.

Trump’s antithesis is to withhold the automatic guarantee at the moment of maximum stress. Militarily, the US can break Iran’s residual ability to contest the Strait; that is not the binding constraint. The point is to delay that act. By allowing a closure or semi‑closure to bite, Trump ensures that the immediate pain is concentrated in exactly the jurisdictions that have most conspicuously free‑ridden on US power: the EU and the UK. Their industries, consumers and energy‑transition assumptions are exposed.

In that context, his reported blunt message to European and British leaders, you need the oil out of the Strait more than we do; why don’t you go and take it? Is not a throwaway line. It is the verbalisation of the antithesis. It openly reverses the traditional presumption that America will carry the burden while its allies emote from the sidelines.

In this dialectic, the prize is not simply the reopening of a chokepoint. The prize is a reordered system in which the United States effectively arbitrages and controls the global flow of oil. A world in which US‑aligned production in the Americas plus a discretionary capability to secure,or not secure, Hormuz places Washington at the centre of the hydrocarbon chessboard. For that strategic end, a rapid restoration of the old status quo would be counterproductive.

A quick, surgical “fix” of Hormuz would short‑circuit the dialectic. If Trump rapidly crushed Iran’s remaining coastal capabilities, swept the mines and escorted tankers back through the Strait, Europe and the UK would heave a sigh of relief and return to business as usual: underfunded militaries, maximalist green posturing and performative disdain for US power, all underwritten by that same power. The contradiction between their dependence and their posture would remain latent.

By declining to supply the synthesis on demand, and by explicitly telling London and Brussels to “go and take it” themselves, Trump forces a reckoning. European and British leaders must confront the fact that their energy systems, their industrial bases and their geopolitical sermons all rest on an American hard‑power foundation they neither finance nor politically respect. The longer the contradiction is allowed to unfold, the stronger the eventual synthesis can be: a new order in which access to secure flows, Hormuz, Venezuela and beyond, is explicitly conditional on real contributions, not assumed as a right.

In that sense, the delay in “taking” the Strait, and the challenge issued to US allies to do it themselves, is not indecision. It is the negative moment Hegel insisted was necessary for history to move. Only by withholding the old guarantee, and by saying so out loud to those who depended on it, can Trump hope to end the free ride.