The Tape Is Now Telling the Story $ASPS

Six months ago this was a thesis built on policy mechanics, bucket aging, and the COVID extend and pretend sunset.

Three months ago it was an entrenchment story confirmed by the seriously delinquent data.

One month ago it was a pipeline not clearing story confirmed by the loss mitigation bounce.

Now is when the data turns into a conversion story:

1) foreclosure w/claim events at a new high

2) the 6+ late bucket fully loaded and still growing

3) Hubzu inventory at multi-year peaks

The cycle is no longer prospective; it is being processed. The remaining variable is delivery, and the company's Q1 earnings show the first quarter of that delivery has begun.

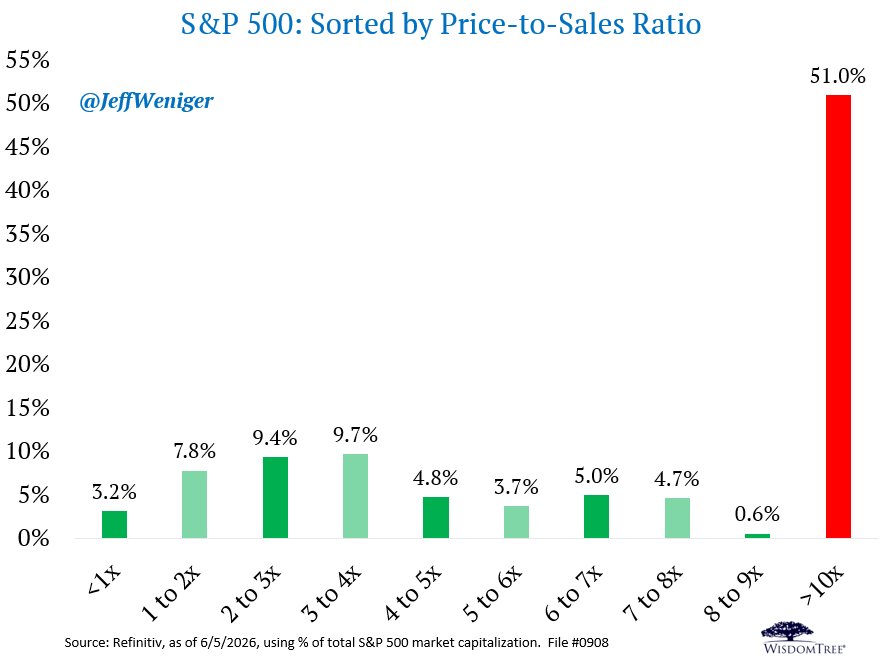

More than half the S&P 500's total value is now in stocks priced above 10x sales. This was once considered an outlandish valuation, as it leaves little room for error. The list includes Nvidia, Apple, GOOG, MSFT, Broadcom, Tesla, Micron, Eli Lilly, AMD, Oracle and 57 more.

When I was with the St. Louis Cardinals, we had a team meeting about hitting with two strikes.

Albert Pujols was leading it.

At the time, he was hitting something ridiculous with two strikes.

I want to say it was around .265.

Naturally, everyone wanted to know how.

So somebody asked:

"What's your two-strike approach?"

Albert's answer surprised me.

He said:

"I think fastball inside and hit it back through the middle."

That was it.

No complicated mechanics.

No secret formula.

Just:

Fastball inside.

Back through the middle.

I remember sitting there thinking:

"Why would you think fastball inside with two strikes?"

So somebody asked him.

And Albert said something I'll never forget.

He said:

"If I can hit a fastball inside back through the middle..."

"I can hit the fastball away."

"I can stay on the changeup."

"I can stay on the slider."

"I can stay on the curveball."

Then he paused.

And said:

"The ball gets deeper."

That's when it clicked for me.

He wasn't trying to pull the inside fastball.

He was using one thought to cover everything.

The more I thought about it...

The more it made sense.

So I started trying it.

And it changed the way I thought about hitting with two strikes.

Instead of worrying about every pitch...

I focused on one.

Fastball inside.

Back through the middle.

See it DEEP.

If you're struggling with two strikes, here's what I'd do tonight:

Round 1: Short Box

(Set the distance somewhere between front toss and batting practice.)

Have a coach throw only fastballs inside.

Your only thought:

"Fastball inside."

Drive the ball back through the middle.

10 swings.

Round 2: Mix Speeds

Now the coach mixes:

- Fastballs

- Changeups

- Breaking balls

- Sliders

But your thought never changes.

You're still looking:

"Fastball inside."

10 swings.

Round 3: Two-Strike BP

Every pitch starts 0-2.

Compete.

Battle.

Use the same approach.

"Fastball inside."

Back through the middle.

10 swings.

That's it.

30 focused swings.

One thought.

One approach.

One goal.

Drive the baseball back through the middle.

One thing I've learned:

Most hitters get worse with two strikes because they add thoughts.

Albert got better because he removed them.

With two strikes, simplicity is a weapon.

Thank you for reading,

Jermaine Curtis

P.S. - If you enjoyed this and thought it was helpful, please share it.

(When you share it, it tells me you want more content like this.)

This is the most sober and sobering analysis of AI investing that I have seen. The cannibalizing the passive flows in idices has been buzzing in my head for weeks now...

https://t.co/DNHnWSUUsr

Remember in college, when you just learned about the 1637 Dutch Tulip Bubble?

You sat in your dorm room and said to your roommates, "man, I wish I could live through just ONE of those. Do you know how many brazillions of dollars I'd make?"

And then you spent the rest of that 6 pack fantasizing about how you'd spend it all.

I'm not shorting it, because I have no fucking clue when the music stops, but you've waited your whole adult life for this.

S&P average single-stock 1m put-call skew has now collapsed to the lowest level in Goldman Sachs entire dataset.

Translation: Everyone is a bull.

Source: Goldman Sachs

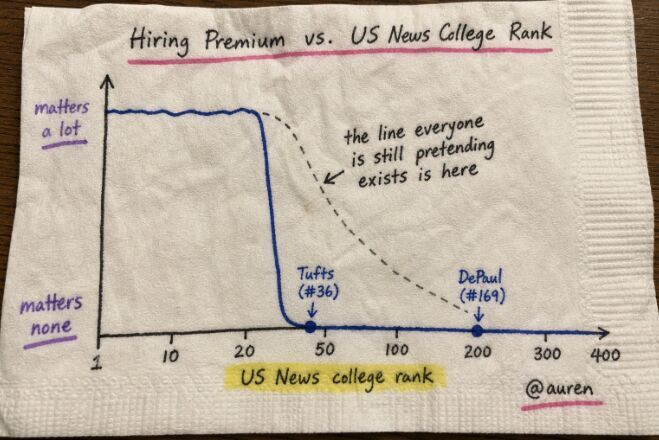

"Unless it's a top university, go to the cheapest one that you like."

This is the right advice for those deciding on which college to attend when thinking about future employment

Going to Boston University or Oberlin just won't matter

h/t @auren

BREAKING: Micron, $MU, extends gains to rise above $1,000/share for the first time in history, now worth nearly $1.2 trillion.

This stock was worth $60 billion just 13 months ago.

I worked as a Big 4 auditor for a decade, here’s my take on the Burry “Fugazi” thread

The transaction is real and the figures check out. Apollo led a $3.5bn capital solution for Valor Compute Infrastructure to fund a $5.4bn purchase of GB200 GPUs leased to xAI on a triple-net structure. Nvidia went in as an anchor LP. All publicly disclosed

But the accounting isn’t prima facie erroneous, and the thread oversells two things

On Nvidia’s revenue. Selling to an SPV is fine. The question under ASC 606 (US revenue standard) is whether control actually transferred. If VCI bears the risks and rewards, Nvidia books the sale legitimately

The REAL issue is the $1.9bn Nvidia ploughs back into VCI as an LP. That’s the round-trip. Net, Nvidia took in roughly $3.5bn of outside cash but booked $5.4bn of revenue

If part of your “sale” is funded by capital you re-injected, that portion isn’t a sale. The honest treatment is either net the $1.9bn off the transaction price, or run a “variable interest entity” (VIE) analysis and consolidate VCI. Recognising gross revenue on round-tripped capital is the potential weak apot

On “legally invisible.” This is rhetoric. The chips sit on VCI’s balance sheet, xAI carries an ROU asset and lease liability under ASC 842 (US leasing accounting standard). Nothing vanishes. It’s held by an entity nobody consolidates, and whether that non-consolidation is correct is the VIE question above

On Level 3 (fair value measurement tier). “No outside party can verify what they’re worth” is wrong. Level 3 means no observable inputs for that specific asset, NOT unverifiable

We typically ALWAYS brought in valuation specialists particularly for high risk material txs, you use observable comps and secondary GPU prices as model inputs, and auditors treat it as a critical audit matter. It gets more scrutiny, not less

The legitimate concern is smaller than this post lets on. Level 3 marks are management estimates exposed to optimistic bias, 34.7% concentration is high for retail annuity backing, and that sits on top of 16.6x leverage and a Bermuda captive outside US statutory oversight. Stack GPU residual-value risk on a multi-year lease and that’s the main concern

Burry’s substance is defensible. The “retirees unknowingly carry invisible risk” packaging is sensationalised. Policyholders hold fixed contractual claims, their exposure is to Athene’s solvency, not directly to GPU residuals

TLDR: auditors need to test whether the sale is overstated by the $1.9bn round-trip, and apply extra scrutiny to the unobservable Level 3 inputs

I’d hate to be the Audit partner signing these transactions off particularly given the public interest and frequency of similar transactions

Arthur Anderson Déjà vu?

People who don't follow cancer research often ask me why we haven't cured cancer. That perception masks a wonderful reality: We make amazing, stepwise progress every year, and the result is that many people live much longer today than they would have previously.

Right now we're in the thick of the annual meeting of the American Society of Clinical Oncology, the biggest research meeting on new cancer medicines, and this morning a bunch of really important studies dropped. I'm going to review them here.

This first image is the result for daraxonrasib, a treatment for pancreatic cancer that is generating consdirable excitement. The green line is the probability of living for patients who got the new drug; the gray one is the chemo control group.

If you follow cancer drugs, a chart like this will make your breath hitch a little. I'm going to review these and some other data here.

@Redfin Redfin data center has removed access to all county-level data, as far as I can tell? Now all that is available is "metro" data, which is not nearly fine-grain enough to be useful. This is a real downgrade of the usefulness of the data. Maybe Zillow is better? @m3_melody comment?

A PARENT’S JOURNEY THROUGH YOUTH SPORTS:

Age 5: “He’s got a cannon.”

Age 6: “He’s the fastest kid out there. Coach said so.”

Age 7: “Rec ball isn’t challenging him anymore.”

Age 8: “We tried out for select. Obviously made it.”

Age 9: “$2,800 for the season. Plus uniforms. Plus tournaments. Plus hotels.”

Age 10: “Cooperstown is basically a family vacation, right?”

Age 11: “He needs a hitting guy. And a pitching guy. And probably a mental performance coach.”

Age 12: “I’m not a crazy sports parent. The OTHER parents are crazy.”

Age 13: “We changed schools. For academics. (And also baseball.)”

Age 14: “Showcases are a requirement at this age.”

Age 15: “Ya his ranking just ticked up. We’re cooking.”

Age 16: “He just needs to get seen by the right school.”

Age 17: “The D1 schools want him to walk on. He’ll earn a spot by sophomore year.”

Age 18: “Okay, D2 is actually really competitive.”

Age 19: “He’s redshirting. Strategic.”

Age 20: “He’s focusing on school now.”

Age 21: “You know what? He’s so much happier.”

Roughly 7% of high schoolers play in college.

About 1.5% of those get drafted.

Less than half of draftees ever play one day in the big leagues.

The odds of our kids going pro are somewhere between “struck by lightning” and “find a $100 in old shorts.”

I love youth sports (all my kids play a bunch of them) just keep a good perspective my friends. ✌️

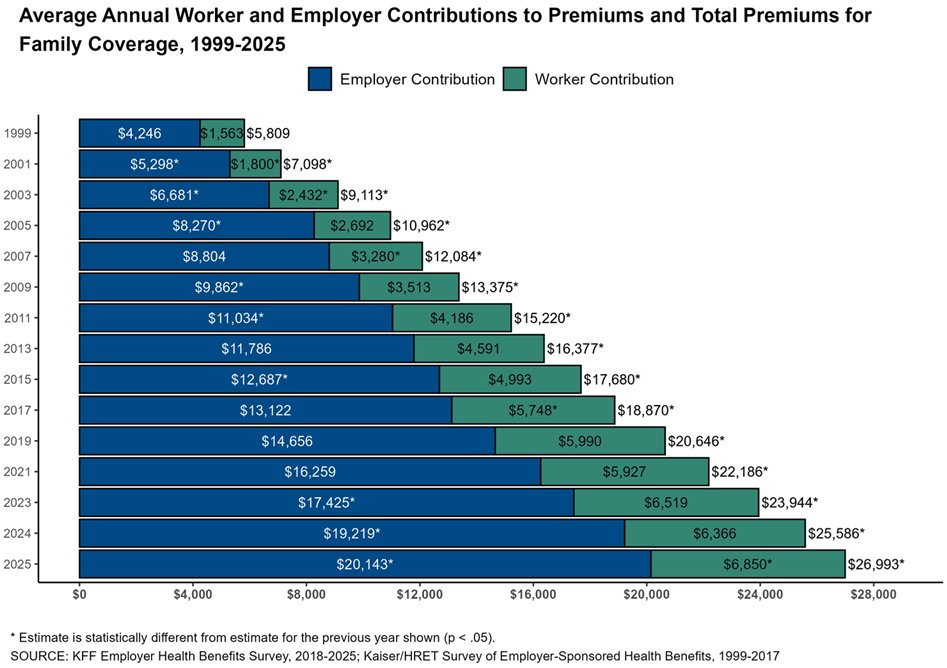

Nearly $27,000 a year for family health insurance premiums, up from $6,000 in 1999.

And that’s before deductibles, copays, and surprise bills.

The system is fundamentally broken.