@olensrud@MichaelGielkens Fully agree! Lots of complexity that make it difficult to assess externally. From a quick glance, I think the acquisitions are from a steady-state basis not less attractive than their own stock. Question remains more on why they suddenly feel the need to do this

@unborn_investor Skepticism to GB acquisition, '26 guidance reset, fund flows, short interest and concerns regarding debt & organic growth.

The whole sector has simultaneously been punished the last few years.

I think with patience great rewards will come, but it's tough and painful now.

$FOUR down 67% from highs while fundamentals hold and the inflection point draws closer.

Bond market assigns limited credit risk and valuation at GFC levels.

Mr. Market offering a gift. Happy to keep receiving it!

@rodrigoaan@AndOnlyJA@CurryorNothing@tlaubers Thanks for spreading the truth! His total position actually increased with 50% between the end of March '26 and the filing on June 5th :)

@tembelvitesi Maybe they should re-release their stablecoins platform announcement from December for the stock to turn green...

Market is a joke but I'm welcoming this gift with open arms!

$FOUR CFO on JPM conference today:

"When I look at the fundamentals of the payments industry, you're talking about a valuation paradigm that we haven't seen since like the GFC."

Don't let flows manipulate you, it's time to fish 🎣

@FromValue Classic "we're investing for the future so margins will be a bit lower for a while" and the market just taking the stock to the shed 🩸

Given $MELI history, I wouldn't bet against them here... A nice opportunity for those with a long-term mindset!

Alright guys, the response is in, and it came directly from @tlaubers - replied to the email himself.

First off, I have to admit I was wrong to expect evasive PR answers. I have a lot of respect for Taylor being this accessible and responsive. It’s great to see him carrying on the tradition of transparency that @rookisaacman built.

I’m sharing his answers below exactly as I received them, without any of my own commentary.

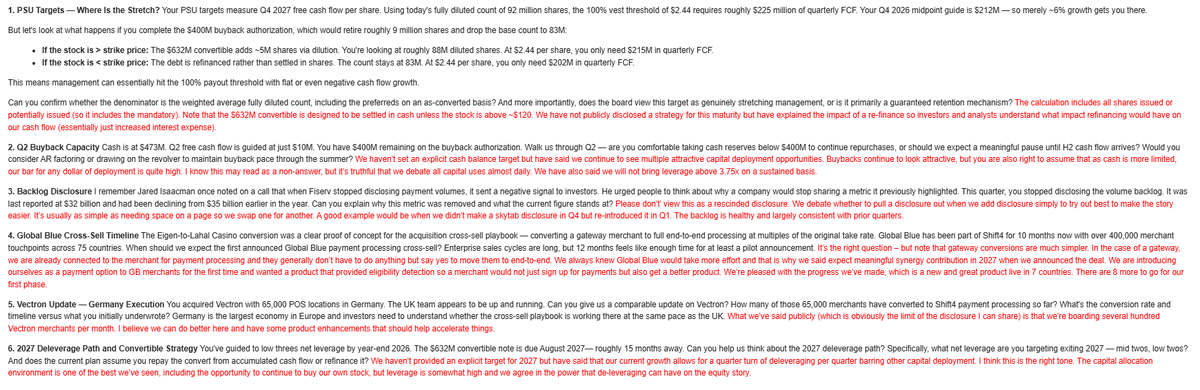

1. PSU Targets — Where Is the Stretch?

The calculation includes all shares issued or potentially issued (so it includes the mandatory). Note that the $632M convertible is designed to be settled in cash unless the stock is above ~$120. We have not publicly disclosed a strategy for this maturity but have explained the impact of a re-finance so investors and analysts understand what impact refinancing would have on our cash flow (essentially just increased interest expense).

2. Q2 Buyback Capacity

We haven’t set an explicit cash balance target but have said we continue to see multiple attractive capital deployment opportunities. Buybacks continue to look attractive, but you are also right to assume that as cash is more limited, our bar for any dollar of deployment is quite high. I know this may read as a non-answer, but it’s truthful that we debate all capital uses almost daily. We have also said we will not bring leverage above 3.75x on a sustained basis.

3. Backlog Disclosure

Please don’t’ view this as a rescinded disclosure. We debate whether to pull a disclosure out when we add disclosure simply to try out best to make the story easier. It’s usually as simple as needing space on a page so we swap one for another. A good example would be when we didn’t make a skytab disclosure in Q4 but re-introduced it in Q1. The backlog is healthy and largely consistent with prior quarters.

4. Global Blue Cross-Sell Timeline

It’s the right question – but note that gateway conversions are much simpler. In the case of a gateway, we are already connected to the merchant for payment processing and they generally don’t have to do anything but say yes to move them to end-to-end. We always knew Global Blue would take more effort and that is why we said expect meaningful synergy contribution in 2027 when we announced the deal. We are introducing ourselves as a payment option to GB merchants for the first time and wanted a product that provided eligibility detection so a merchant would not just sign up for payments but also get a better product. We’re pleased with the progress we’ve made, which is a new and great product live in 7 countries. There are 8 more to go for our first phase.

5. Vectron Update — Germany Execution

What we’ve said publicly (which is obviously the limit of the disclosure I can share) is that we’re boarding several hundred Vectron merchants per month. I believe we can do better here and have some product enhancements that should help accelerate things.

6. 2027 Deleverage Path and Convertible Strategy

We haven’t provided an explicit target for 2027 but have said that our current growth allows for a quarter turn of deleveraging per quarter barring other capital deployment. I think this is the right tone. The capital allocation environment is one of the best we’ve seen, including the opportunity to continue to buy our own stock, but leverage is somewhat high and we agree in the power that de-leveraging can have on the equity story.

$FOUR