@evandi13579b@Automoto415792 Has the launch business ever made a profit? Will Starlink displace cellular networks? Just because Musk throws out a TAM and a market cap figure does not make it real. Investors need to do their own second-level thinking or they are likely to get fleeced.

@EnerTuition Very smart move by S&P. If the SpaceX IPO crashes and Burns after it is included in the NASDAQ index, that will tarnish NASDAQ ‘s reputation for a very long time. S&P will be the beneficiary.

@EnerTuition Very smart move by S&P. If the SpaceX IPO crashes and Burns after it is included in the NASDAQ index, that will tarnish NASDAQ ‘s reputation for a very long time. S&P will be the beneficiary.

@Gfilche IDK. Seems like robots would be harder than unsupervised FSD. I think it will be the same as that timeline: "next year for sure" for the the next ten years. Fool me once, shame on you. Fool me a hundred times, shame on me.

Even though Tesla is now incorporated in Texas, the timeline for Tesla to merge with SpaceX would be quite long. Here is the detail from CoPilot:

Here is the full, end‑to‑end timeline for a Tesla–SpaceX merger assuming SpaceX remains private and is merged into Tesla. This is the realistic regulatory‑critical‑path timeline, not the optimistic one. It reflects how long each agency actually takes in comparable large, sensitive, multi‑agency mergers.

🧭 Realistic Timeline for a Tesla–SpaceX Merger (SpaceX stays private)

Total duration: 18–36 months

Earliest plausible completion: mid‑2028

Most realistic completion: late‑2028 to mid‑2029

Phase 0 — Pre‑Merger Preconditions (Valuation, Board Setup)

Duration: 3–6 months

Even if SpaceX stays private, Tesla must still obtain:

Independent fairness opinions

Private‑company valuation audits

A special committee of independent directors

Conflict‑of‑interest mitigation structures

This is slower because SpaceX is private and its financials must be disclosed to Tesla shareholders.

Estimated window: Q4 2026 – Q1 2027

Phase 1 — Drafting the Plan of Merger (Texas Corporate Law)

Duration: 2–4 months

Tesla’s board must:

Approve the Plan of Merger

Document fiduciary‑duty compliance

Prepare disclosures for shareholders

Estimated window: Q1 – Q2 2027

Phase 2 — Tesla Shareholder Vote

Duration: 2–3 months

This includes:

SEC review of the proxy

Mailing period

Shareholder meeting scheduling

Texas law requires a majority of outstanding shares, not just votes cast.

Estimated window: Q2 – Q3 2027

Phase 3 — SEC Related‑Party Transaction Review

Duration: 3–6 months (overlaps with Phase 2)

Because Musk controls both companies, the SEC treats this as a high‑risk related‑party transaction.

This is one of the longest steps.

Estimated window: Q2 – Q4 2027

Phase 4 — FTC/DOJ Antitrust Review (HSR)

Duration: 6–12 months

Even though Tesla and SpaceX are in different industries, regulators will examine:

Vertical integration (AI + robotics + satellite)

Data concentration

Potential foreclosure of competitors

This is a guaranteed Second Request.

Estimated window: Q3 2027 – Q3 2028

Phase 5 — CFIUS National‑Security Review

Duration: 3–9 months (can overlap with antitrust)

SpaceX’s classified missions and military contracts guarantee a CFIUS review.

CFIUS can:

Impose conditions

Delay

Block the merger

Estimated window: Q4 2027 – Q3 2028

Phase 6 — NASA & DoD Contract Novation (FAR)

Duration: 6–12 months

SpaceX’s NASA/DoD contracts cannot automatically transfer.

NASA and DoD must approve novation, evaluating:

Governance

Mission assurance

Cybersecurity

Financial stability

This is a unique bottleneck.

Estimated window: Q1 2028 – Q1 2029

Phase 7 — Final State Filings & Closing

Duration: 1–2 months

After all federal approvals:

Texas accepts the merger filing

Tesla updates securities filings

SpaceX corporate structure is dissolved into Tesla

Government contract novations finalize

Estimated window: Q2 2029

🧮 Full Timeline Summary

PhaseDurationEstimated Window Preconditions3–6 moQ4 2026 – Q1 2027 Merger Plan2–4 moQ1 – Q2 2027 Shareholder Vote2–3 moQ2 – Q3 2027 SEC Review3–6 moQ2 – Q4 2027 Antitrust6–12 moQ3 2027 – Q3 2028 CFIUS3–9 moQ4 2027 – Q3 2028 NASA/DoD Novation6–12 moQ1 2028 – Q1 2029 Final Filings1–2 moQ2 2029

🎯 Final Completion Date (Realistic)

Late 2028 to mid‑2029

This assumes:

No litigation delays

No CFIUS mitigation complications

No antitrust structural remedies

No NASA/DoD mission‑assurance objections

If any of those occur, the timeline extends further.

If you want next, I can map out:

Critical path dependencies

A Gantt‑style timeline

Deal structures that minimize regulatory risk

Which one do you want to explore?

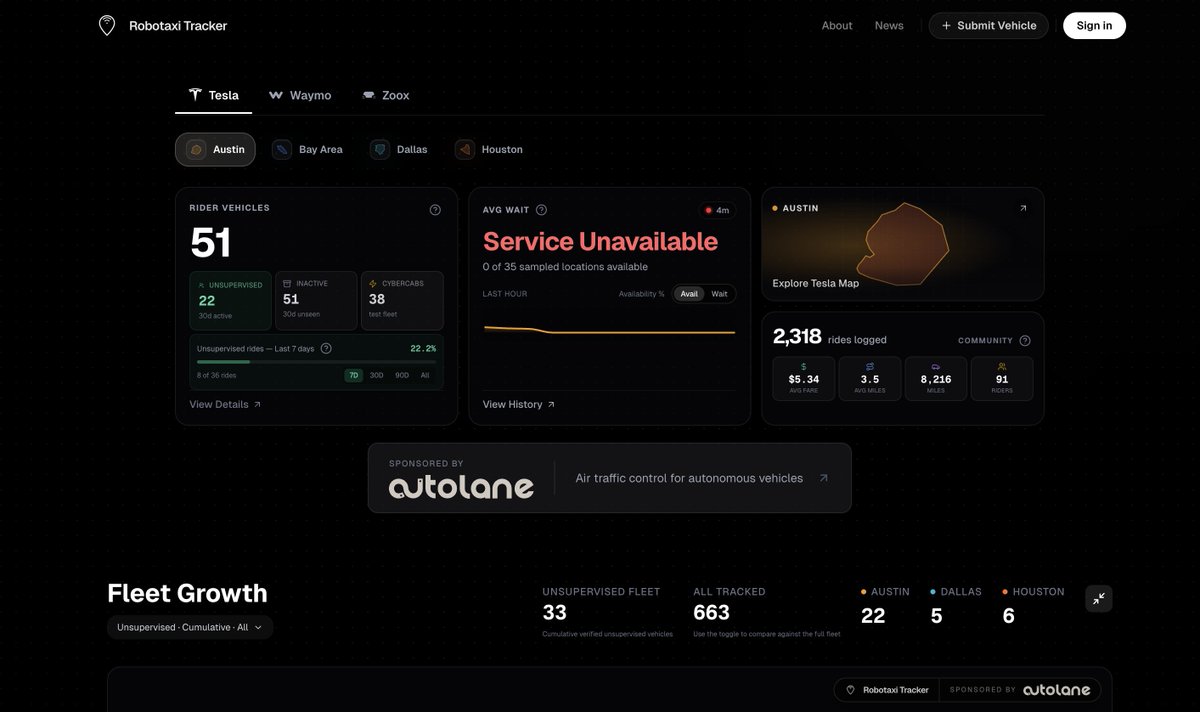

@ethanmckanna So they are cosmetically adding a bunch of vehicles that probably are not generating rides. That's the only explanation I can come up with for this chart (from 2 minutes ago):

Cathie Wood always makes the assumption that Tesla has an insurmountable technology lead. There is no reason to believe that is the case for autonomous driving. Companies that utilize cameras plus other sensors are way ahead of Tesla currently and there are formidable technology companies researching and developing AV technology with all manner of sensor configurations. It's obvious at this point that the real world data collection from FSD is insufficient to solve all of the edge cases involved in Level 4 autonomous driving with camera-only technology. As a result, the competitive structure in this industry will NOT lead to a "winner take all" scenario, and therefore the profits available will not be sufficient to justify Wood's return expectations for Tesla.

BTW, a 30% drop in the Nasdaq would take that index down to a level last seen just ONE YEAR AGO! What would be the catalyst? Here's one: the AI providers (Anthropic, OpenAI, Gemini) have been offering compute at a significant discount to what their actual costs are. Eventually those subsidies will have to end, and we are starting to see that already. We will then see what the true demand is at the prices necessary to fund the huge compute capex planned by the hyperscalers. Today's WSJ article highlighting that OpenAI is not meeting its internal goals for revenue is an ominous sign that the end market isn't large enough or mature enough to support all of the expansion plans of the hyperscalers. Almost all of the earnings growth in the major indices has been driven by the AI boom. Any pullback in expectations there will have a very widespread impact on the entire food chain of AI companies and stock prices. Semiconductor stocks are probably the most sensitive to this dynamic, given how much they have run up and the typical double-ordering that takes place during periods of high demand in the industry. The fact that they are faltering today could be the canary in the coal mine. Be careful out there!

For those holders of TSLA stock who actually are interested in understanding the risk of their position, TSLA has a beta of 2.09. This implies that if the market were to decline by 30%, TSLA would decline by 63%. This would be without any negative developments for the company, of which there would be plenty. For instance, the capital markets window for raising capital would close. Tesla would likely be unable to raise any fresh capital to continue to fund its huge investment plans. The SpaceX IPO would be postponed indefinitely, which would eliminate the potential backstop of a SpaceX acquisition of Tesla with SpaceX's hideously overvalued stock as currency. My guess is that TSLA would fall to $50, an 86% drop from $370. Is your TSLA position sized appropriately for this risk?