난 게임을 즐겨하지 않는데 이런건 진짜 유익함

만원으로 데이터 센터의 복잡한 구조와 컴퓨터 인프라를 이해하는 스팀게임 : Data Center

빈 방에서 시작해서

랙 구매 → 서버 장착 → 모든 케이블을 직접 손으로 하나하나 연결해야함

실제 데이터 센터처럼 고객 트래픽을 처리하는 시뮬레이션 게임

출시 48시간 만에 180개가 넘는 리뷰가 달렸고, 플레이어들은 “최근 본 시뮬레이션 게임 중 가장 몰입감 있다”, “컴퓨팅 인프라를 이해하는 데 최고”라는 평가를 하고 있습니다.

i'm obsessed with AI DIY projects.

my favorite one right now is this broccoli farmer in hokkaido, japan using Codex to run his 100-hectare farm

this guy never studied agriculture, never inherited land, started out as a civil servant.

but he wanted his farm to run better, and instead of paying an engineering firm he couldn't afford, he just built the tools himself.

here's what he's built on his own:

> remote control of his greenhouse vents from a chat app, wired up with an esp32 board, a motor driver, and cloudflare workers

> a bot that checks each greenhouse's temperature and opens the vents when it gets too hot

> satellite crop-health data laid over a map of his own fields

> an airtable base linking his plots, tasks, materials, and sensors

> wiring diagrams of his electrical panels, generated from a photo

stuff like this used to be locked behind machinery and engineers only the big agribusinesses could pay for.

but this legend just breezed past all of it with a laptop and Codex lol

Today I added to my $POWI (Power Integrations) position, planting my flag in what I believe will be a massive Capex wave transforming the entire power semi space

Currently, $NVTS is getting all the love which is fair, however...

With the release of the specs for the upcoming architecture of the 800V Data center for VR200 it is quite clear that there will be a huge demand for high voltage GaN rather than high speed integration GaN in which NVTS provides

The server rack will be scaling from 120 kW to 600 kW (!)

The core issue isn't going to be how fast a chip can switch, it will be about how much raw voltage can actually survive

Navitas flagship GaN tech (GaNFast and GaNSafe) maxes out at 650V

It was originally designed for high speed switching in consumer electronics and lower volt apps not not megawatt scale AI infrastructure

A 800V data center will instantly destroy a lone 650v chip. To participate, NVTS has to combine lower voltage components in a highly complex stacked build which creates clunky workarounds, wastes physical space, and introduces severe points of failure

POWI's chips doesn't require these unnecessary workarounds

Their InnoMux-2 is the ONLY chip on earth that features a 1700v switch on a single piece of silicon

When NVDA starts to roll out these high power racks, a single PowiGaN chip will be able to handle it natively with an integrated safety buffer to spare

Which is IMPORTANT because in the case of power spikes, POWI's voltage leaves a 900v buffer that is built to handle the power spikes without creating a power failure

Let me put this into context for you guys

If NVDA said F it let's skip 800v and go straight to 1200v DC POWI's 1700v chips are still able to handle the power consumption TODAY still with a SAFETY BUFFER

Here is why $POWI is still undervalued:

They didn't build the 1700v chip for AI

They originally built it to handle unstable power grids in developing markets and heavy electric vehicle architectures

When $NVDA shifted the Vera Rubin architecture to an 800V DC baseline, their engineers realized they needed a battle tested SINGLE chip solution to safely drive the background cooling infrastructure (fans, liquid pumps, and logic controllers)

POWI was the only company in the world that had spent decades perfecting single chip high volt integration.

That deep reliability is why they are co-designing power blueprints alongside NVIDIA TODAY

If you track the projected power infrastructure spend per AI rack, the metrics are going vertical:

Current (GB200): $36,000 per rack

2026 (Vera Rubin): $76,000 per rack

2027 (Vera Rubin Ultra / Kyber): >10x increase (Over $360,000 to $398,000+ per rack)

POWI's TAM is literally multiplying right before our eyes

Currently, their entire business is still being dragged down by legacy

When you look at $POWI at surface level, you see flat YoY revenue, lower GAAP margins, and a high P/E ratio

but don't be fooled, their PowiGaN product division is growing at over 40% annually and will continue to accelerate as the VR is deployed

In February 2026, POWI even did a 7% workforce reduction to reallocate that money toward scaling DC revenue

You are essentially paying a cyclical multiple for a boring legacy appliance business, and getting a structurally protected, high voltage AI pure play for free even after the initial move

From a TA perspective, just look how coiled it is. Currently trading under it's HTF downtrend line while simultaneously allowing moving averages to play catch up

It's only a matter of when not if imo this breaks out

NFA. Research purposes only.

Loved the theme posting by @KawzInvests and @ParadisLabs (follow them)

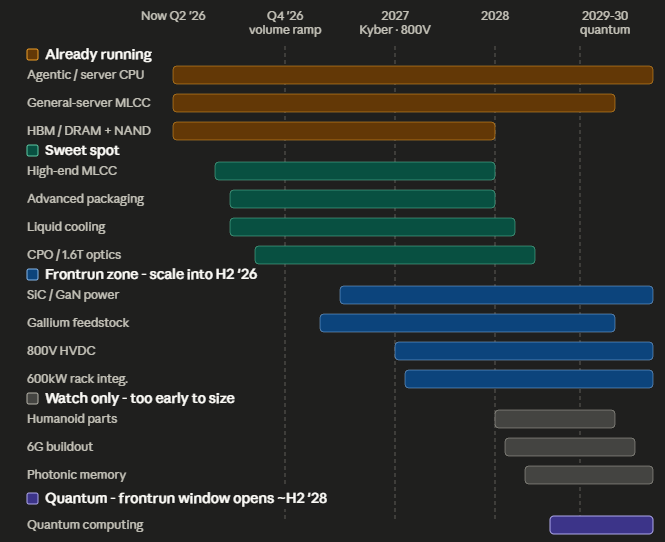

So I decided to follow this up and go one step further by mapping out the timeline of all these themes and their ramp dates.

RUNNING NOW (Still biddable, but easy money gone)

> agentic AI flipped the CPU:GPU ratio from 1:8 to 1:4 already, server CPU prices up 20% with 6 month lead times

> general server MLCC rides the same CPU revival, already inflecting not waiting

> memory is the real bottleneck, DRAM revenue +303% in 26 and NAND +208%, squeeze runs into 27-28

SWEET SPOT (Inflection point)

> high end MLCC at 20+ week lead times, Murata order inquiries at 2x supply capacity, OEM price hikes land next quarter

> advanced packaging scales with the HBM4 and Rubin ramp

> liquid cooling is not a sleeper, Rubin mandates full liquid so it inflects with the GPUs, not after

> CPO and 1.6T optics scale hard with Rubin, Foxconn already shipping CPO switch from Q3, 10k units in 26

FRONTRUN (scale into H2 26)

> SiC and GaN power ride the 800V push, autos already matured the cost curve

> gallium is the GaN feedstock, upstream of the entire power buildout

> 800V HVDC hits mass deployment with Kyber in 27, supply chain gears up through H2 26 (Vertiv launches H2 26)

> 600kW racks arrive with Kyber in 27, the whole power chain rerates ahead of it

WATCH ONLY (too early to size)

> humanoids are a future demand pool, not a 26-27 trade

> 6G is a late decade story

> photonic memory still early stage

> quantum prototypes in 27, IBM fault tolerance target 29, Foxconn commercialization around 30, so the frontrun window is H2 28 to H1 29

Do not become dilution for Quantum. If you want a 1hr rundown on the future of Quantum I'd recommend you watch the @MartinShkreli and @StockSavvyShay debate.

Anthropic just paid millions to hire Andrej Karpathy.

He gave you the same knowledge for $0 the same week.

Co-founder of OpenAI. Former head of AI at Tesla. The man who coined vibe coding.

No recruitment fee. No exclusive access. Just a link and 29 minutes.

LLMs are ghosts not animals.

Vibe coding is dead.

Software 3.0 is here.

Watch it.

Then read this.

Because Karpathy tells you what Software 3.0 is.

This shows you how to build one - a software factory with Claude Code that ships features while you sleep.

The full build guide is below.

I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

https://t.co/Z5M3TvHH2B

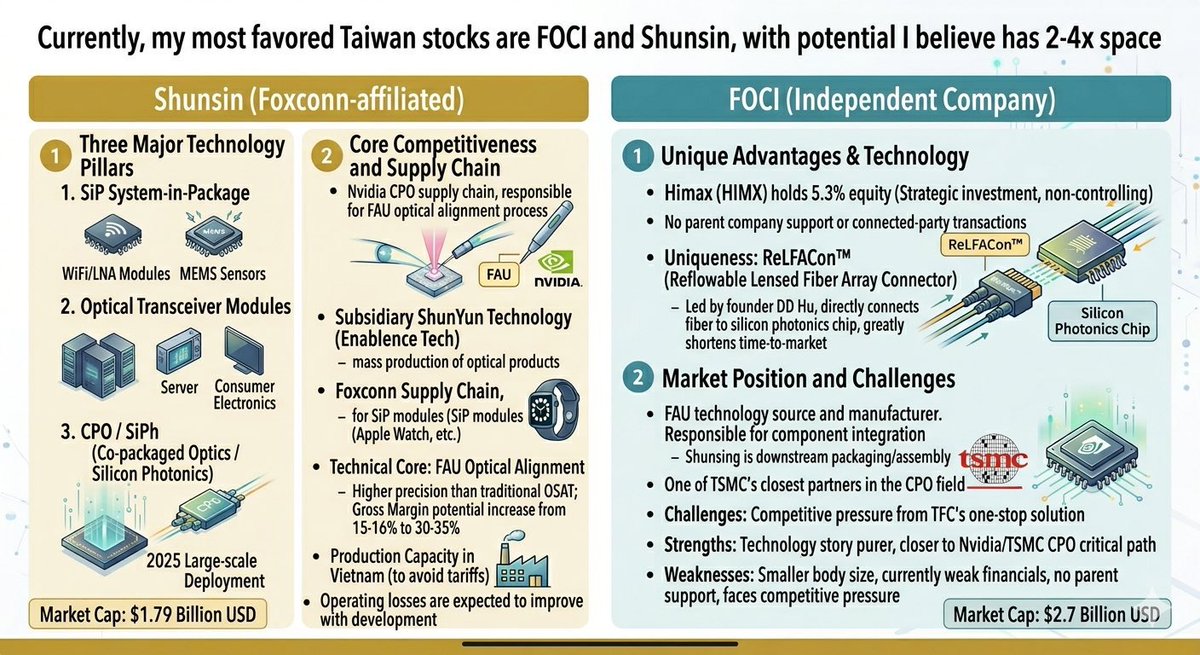

Here is a great explanation as to why FOCI and Shunsin are two of my biggest plays in the Taiwanese ecosystem.

FOCI is my main Taiwanese position.

FOCI (3363.TWO) -- $2.7B market cap. Independent. No parent company. No related-party dealings. Just technology.

FOCI is the originator and manufacturer of FAU -- Fiber Array Units. This is the precision component that connects fiber arrays directly to silicon photonic chips. Their patented ReLFACon technology eliminates design customization, shortens time to market, and is extremely hard to replicate. Led by founder DD Hu, this is not a me-too product. This is the source.

FOCI is one of TSMC's closest partners in the CPO field. Confirmed sole supplier of FAU for the COUPE optical engine -- the platform inside NVIDIA's Vera Rubin generation. Gen 1 and Gen 2 are locked.

The weaknesses are real and I will not hide them. Financials are currently weak. No parent company support. Chinese competitors are closing in. TFC's one-stop solution is competitive pressure worth watching. But the technology narrative is the purest of any name in the CPO supply chain right now.

2+2=4. I am waiting for the market to do the math.

Shunsin is my second biggest position.

Shunsin (https://t.co/YrGDyMnvB6) -- $1.79B market cap. Foxconn-affiliated. Three business pillars: SiP System-in-Package, Optical Transceiver Modules, and CPO/SiPh.

The CPO angle is the one that matters most right now. Shunsin handles the FAU optical alignment process in NVIDIA's CPO supply chain -- a higher-precision step than traditional OSAT packaging. Gross margins on CPO and 1.6T products could expand from the traditional OSAT range of 15-16% up to 30-35%. That margin expansion is the valuation rebuild story.

Subsidiary ShunYun Technology signed a mass-production OSAT agreement with Enablence Technologies in March 2026 to supply optical products for the AI data center market. Vietnam production capacity helps avoid tariffs. Foxconn supply chain relationships give it access to Apple Watch SiP modules on the consumer side -- diversification that pure CPO plays do not have.

FOCI is the technology originator. Shunsin is the downstream packaging and assembly layer. They are not competitors. They are sequential steps in the same supply chain.

Both are early. Both are small. Both are the kind of names that re-rate violently when the theme gets crowded.

Bullish FOCI. Bullish Shunsin.

Great job to @cherryPayment on this infographic.

$TKR - (The Timken Co.)

Actuators account for 40%-60% of the entire BOM for a humanoid robot. This is the single largest cost structure in the humanoid/robotics industry. Humanoids have not started scaling yet, but when/if they do, actuators will open up a huge market for hardware suppliers imo. The bet here is scaling of the TAM. Actuators for humanoids and most robots need electric motors and precision gearboxes, $TKR provides the latter.

Specialized and niche precision gearboxes (Harmonic Drives) are an integral part in humanoids' rotary joints—the shoulders, elbows, wrists, and hips—to allow movement. There is a huge shortage of supply for these Harmonic Drives, there's a tall ladder when trying to bring on additional supply capacity with high lead times in tools needed like Multi-axis CNC, High-Rigidity Precision Grinding Machines, material procurement takes 12-16 weeks, and quality assurance taking anywhere from 45 mins- 1 hour per unit. I'm personally betting that there will be a huge increase in demand for harmonic drives as the humanoid industry scales. Currently most of Harmonic drive suppliers are foreign (Harmonic Drive SE/Japan, Nabtesco/Japan) and private/smaller U.S. firms focus more on worm/planetary/slew but not strain-wave harmonic at scale. There is currently only one U.S. based supplier of Harmonic Drives, $TKR. Historically known as a heavy industrial bearing manufacturer, Timken has spent the last several years aggressively acquiring its way into the exact precision motion control niches causing this manufacturing bottleneck. Through its Industrial Motion segment, Timken owns the complete mechanical stack for robotics:

Cone Drive

$TKR acquired this European business in 2018. This is Timken’s direct asset for the bottleneck and why I'm interested in them. Cone Drive manufactures harmonic strain wave gearing (specifically targeting humanoid robotic joints like hips, knees, and wrists) out of U.S.-based manufacturing facilities. Acquiring them makes $TKR effectively the only U.S.-based public supplier of harmonic drives.

SPINEA (Acquired 2022)

Produces cycloidal reduction gears, which provide the high-load rigidity and torque needed for a robot's heavier structural axes (waist and shoulders).

CGI Inc. (Acquired 2024)

Specializes in high-precision, miniaturized gearheads and sub-assemblies historically utilized in surgical robotics and medical devices.

By rolling up Cone Drive, SPINEA, and CGI, Timken operates as a "one-stop shop" capable of supplying precision gear systems across all six axes of a robotic or humanoid actuator. What makes them even more interesting is that the high-growth robotics harmonic drive business is consolidated inside a massive legacy industrial business. Timken operates under two primary reportable segments:

Engineered Bearings (~66% of FY '25 sales): This includes tapered roller bearings, spherical/ cylindrical roller bearings, ball bearings, and related components. Serves diverse end-markets including automotive, off-highway, rail, aerospace, wind energy, and general industrial. Revenue has been relatively stable/flat in recent years, with growth from pricing/mix and select markets (e.g., renewables) offset by softer demand in others. Q4 2025 sales +0.9% YoY; full-year adjusted EBITDA margin ~18.9–20.0%.

Industrial Motion (~34% of FY '25 sales): This includes precision gearboxes and gears (via brands like Cone Drive, Spinea, and CGI), drives, breathers, seals, automatic lubrication systems, linear motion products, chain, belts, couplings, and industrial clutches and brakes. This segment has shown stronger growth: +8.4% YoY in Q4 2025 (driven by demand, pricing, FX, and acquisitions) and has delivered double-digit internal CAGR in the automation/robotics end-market since 2018. Adjusted EBITDA margin improved to ~19–21% recently (21.0% in Q4 2025).

Peer Comparison

Bearings-heavy peers trade in the 8–12x EV/EBITDA range (e.g., SKF, NTN analogs, or diversified industrials like RRX in power transmission). Precision/aerospace-focused names like RBC Bearings command modest premiums but still align with cyclical industrial multiples rather than secular growth. TKR’s current ~12x EV/EBITDA and ~2.1x EV/Sales reflect its diversified but mature end-markets (auto, off-highway, rail, wind) and perceived cyclicality — not the high-growth robotics optionality.

In contrast, robotics/humanoids/automation peers Timken trades at a discount. $RRX trades around 15.5x EV/EBITDA, while $MOG.A commands a much higher multiple of 21.3x EV/EBITDA. Timken sits comfortably in the middle. I believe TKR’s humanoid exposure (via the faster-growing Industrial Motion segment) is not yet fully priced in by the market.

In the Q1 2026 earnings call, CEO Lucian Boldea highlighted automation/robotics as a strategic priority where Timken has “doubled down,” delivering double-digit CAGR since 2018. Humanoids are explicitly called out as a high-potential subset addressing labor gaps: "Cone Drive and Spinea provide harmonic/cycloidal drives for joints; Rollon for 7th-axis linear; CGI for medical robotics; Timken bearings and Cone Drive harmonics already present in humanoids/exoskeletons. We are nicely positioned to benefit… We will have our newly appointed Chief Technology Officer talk more at Investor Day about the opportunity.” The company participates in humanoid summits and frames harmonic solutions as core to scaling these platforms. With Industrial Motion already outgrowing the legacy bearings segment and backlog momentum building, the humanoid/robotics tailwind represents asymmetric upside that justifies a valuation re-rating above legacy auto/aerospace multiples — toward robotics/automation peers (15–20x+ EV/EBITDA) as revenue contribution scales.

This is my thesis for $TKR not financial advise. I'm simply jotting down my notes and sharing with you all so maybe you can have a new perspective on the industry or even find critics in the thesis yo may not agree with.

I really like $MTSI for the upcoming parabolic CPO growth in 2027+

TLDR:

Demand for the components they make/design will only intensify w/ CPO.

E.g. their SiPh drivers + CW lasers.

With management confirming:

-> "Our future products are increasingly optimized for CPO"

-> "We think that the CPO transition is a benefit to MACOM"

This sits on top of 800G/1.6T volume tailwinds that they're already enjoying:

- data center revenue keeps growing each quarter

- backlog is huge

- DC guidance keeps getting raised

With 3 (unnamed) hyperscalers already using Macom's chipset for pluggables/LPO.

I don't personally look too deep into financials for smaller MC names e.g. $SIVE etc.

But when you get to $MTSI's scale, that becomes important:

They're net cash positive + strong op. cash flow.

Plus GM expansion to ~58% w/ mix shift towards DC/CPO relevant products.

With Q3 quidance implying further expansion to ~60%.

Not to mention that 3.2T roadmap is being previewed currently, so you'd get further top line growth on top once rolled out eventually.

Green ticks all round.

Not to mention the £45M investment into $IQE which secures them InP capacity for lasers used in CPO/pluggables.

Which de-risks supply significantly (+ boosting IQE outlook in the process).

Fairly safe compounder imo, even at current premium valuations.

the engineer who built Claude Code just dropped a 28-minute video on how to write prompts that actually work

I've seen $300 courses that don't cover what he shows in the first 10 minutes

CLAUDE.md files, memory shortcuts, parallel sessions, prompting patterns

all in one video and completely free

works whether you're a developer, a beginner, or someone who's been using Claude for months

based on this, I put together 18 things you can copy and use in Claude today

full guide in the article below