$ROOT has and continues to be my top stock pick that, despite today's market, is presenting one of the greatest opportunities.

$ROOT is reshaping auto insurance by embedding real-time, personalized coverage directly into the vehicle purchasing experience through partners like $CVNA. Instead of customers shopping separately for insurance, $ROOT integrates instant underwriting and binding into checkout, compressing what is normally a multi-step, high friction process into a few clicks. "Carvana Insurance Built With Root" has now surpassed 200,000 policies sold.

They have also scaled aggressively into the Independent Agent space, now partnering with more than 15,000 agents across 5,000 agencies nationwide - including a recent launch with Freeway Insurance, the largest personal lines insurance distributor in the country. Their 24-hour appointment flow, where an agent can get appointed and start writing with $ROOT in as little as 24 hours, is compressing what is often a multi-week onboarding process at legacy carriers. $ROOT can scale this channel without needing armies of sales agents - automation handles what legacy carriers staff entire departments to manage.

Both of these channels operate alongside their Direct to Consumer model, where customers get insurance through their app and $ROOT uses telematics directly on customers' phones to price policies based on how they actually drive, not demographics. The safer you drive, the more you save. This is powered by $ROOT's proprietary algorithms trained on over 36 billion miles of driving data.

Bad drivers are identified and exited quickly, so good policyholders aren't subsidizing bad ones. This allows $ROOT to reward safe drivers with better rates, driving higher customer lifetime value and a flywheel effect between data accuracy, pricing precision, and growth. As Alex Timm described on the Q1 2026 earnings call: data, pricing models, and distribution have a mutually symbiotic relationship - more data produces better pricing, better pricing drives distribution growth, and distribution growth generates more data. That flywheel is spinning faster every quarter.

This risk modeling allows $ROOT to pass savings onto their embedded and independent agent customers as their predictive models continue to improve with every mile collected, and the next frontier is already in motion: with roughly 90% of new vehicle sales now equipped with built-in data connectivity, $ROOT has positioned itself as the partner of choice for OEMs wanting to leverage that data - with Toyota and Hyundai partnerships already live. Connected vehicle data will make their pricing advantage even harder to replicate.

$ROOT's model lowers customer acquisition costs and improves loss ratio control through data-driven pricing - delivering an industry-leading gross accident period loss ratio of 58.8% and a net combined ratio of 91.4% in Q1 2026, improving 4.2 points YoY.

However, what truly separates $ROOT is where they are going: As Alex Timm stated in the Q1 2026 shareholder letter: "We are on the way to building an entirely automated insurance carrier. From our next generation risk brain in pricing, to our modern, AI-native claims architecture, $ROOT is increasingly becoming a closed loop system capable of rapid decision making and continuous learning."

The vision is a fully automated, AI-based closed-loop insurance platform spanning acquisition, underwriting, pricing, and claims - where each component reinforces the others and the system compounds in value over time. Improvements in claims accuracy enhance pricing precision. Stronger underwriting reduces fraud and loss volatility. The result is a faster, more adaptive, more efficiently priced business with every passing quarter.

What makes this moat durable? Alex said it on the earnings call: "It's very difficult to see and understand and appreciate the value of a 10x platform in insurance, whether that's our data science platform, our telematics platform or our claims platform, or most importantly, the fact they're all a single platform and integrated inside one company. That is incredibly difficult to sort of see clearly from the outside. From the inside, that is our most valuable asset." Replicating this requires not just advanced technology, but deep data assets, regulatory infrastructure, and operational scale built over years. Legacy carriers averaging 104 years old cannot simply migrate into this.

All of this while $ROOT has been at the forefront of technology advancements in the industry:

- First US auto insurance carrier built entirely around a mobile app

- First to make the default pricing engine based primarily on actual driving behavior, not demographics

- First to underwrite out the riskiest drivers using telematics data

- First to successfully offer embedded insurance solutions at the point of digital vehicle purchase

Net premiums written have grown at a 41% CAGR since 2020, reaching ~$1.5B gross written premium on a TTM basis - yet $ROOT still holds only ~0.5% market share. With multiple states still untapped - targeting all contiguous US states by end of 2027 - tens of thousands of agents left to onboard, and new embedded partners added every year, the runway is significant across every channel.

$ROOT's goal is to "be the largest and most profitable personal lines insurance provider in the US." They delivered record net income of $36M in Q1 2026, nearly doubling YoY, with a 47% annualized ROE. They have strengthened their balance sheet, refinanced debt at significantly lower rates, and authorized a $75 mil share repurchase program - reflecting confidence in the durability of the business.

$ROOT's float is only ~13.9 mil shares. There are millions of investors who will want a piece of this company as it becomes a dominant force in personal lines insurance. At a market cap that still dramatically undervalues what is being built underneath, the window to own this ahead of the crowd is now.

Don't sleep on the name. The thesis is real, the execution is there, and the market hasn't fully priced what this company is building.

@KabraxFX so key - insurance is wild because the cost to collect the data to properly train models is both time and money (paying claims). $root is approaching 1M claims that has taken almost 10 years to collect and cost ~$3B in payouts. new insurtechs cant skip this step

@Yochana42437421@Neil_X10 true - also cant LLM your way to brand, owning massive claims datasets to train on, and being licensed across 50 separate regulation entities. $root $lmnd

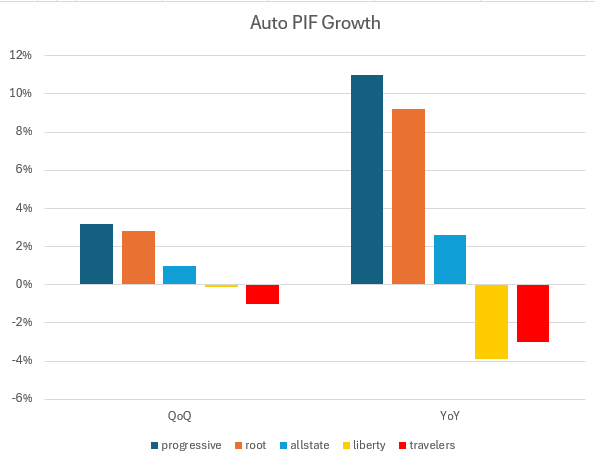

Even with $root pulling back on growth as the market softens, they're still growing faster than the industry due to their growing advantage in partnership channel.

Once the market cycle turns, they'll turn back on direct and grow faster than almost anyone anticipates

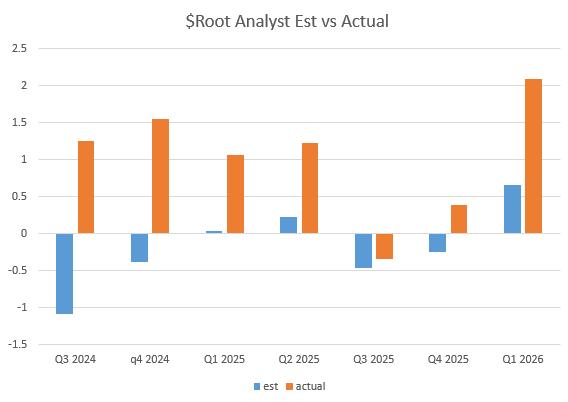

WS doesnt seem to grip what $root is doing. Over last 7 Q's their estimates are >700% low on average.

On the calls leadership has to explain over and over that they dont operate the same cookie cutter approach as legacy insurers who optimize for quarterly results/consistency

@KabraxFX@AnthonyKantola haha i felt the same way - but if it gives them an opportunity to share more about the company ill take whatever i can get. hopefully it remains a quarterly staple

$root is trading at a Q1 annualized PE of 6!

as a reminder, they are growing PIF faster than anyone in the industry based on their tech and distribution advantages

Probably nothing:

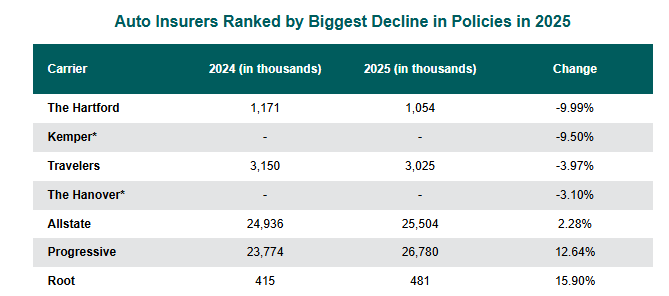

- highest PIF growth

-cheapest valuation

-built on modern tech

-largest runway (not even in all 50 states, only with 10% of IA's)

-embedding with OEM's faster than any competitor

Dont understand how people are missing this. $root

interesting that $lmnd seems to be changing their tune regarding IA's. meanwhile $root has been focused on this for a while and already has 15k IA's and ~$400M IFP which just tripled YoY

@Ironic_Ape im focused on IFP growth and margin which are essentially used to derive NI.

and for me the goal is financial freedom in the next few years so im not really playing the 15-20 year time horizon game like i used to. if i went out that far id likely own more $lmnd

@Ironic_Ape im looking apples to apples - TTM Gross Loss and LAE for $lmnd was 70% and root was 65%. Making up that 5 pts in ER is possible but asking a lot. Add that with the need for 78% IFP growth and ill take $root all day long for a 5 year look out.

@Ironic_Ape how do you propose we estimate margins? $lmnd LR target is 70%, $root is 60-65% so lets say 62.5%. Perhaps $lmnd could have lower ER eventually, but will it be 7.5 pts lower? Keep in mind $root is also operating on modern tech stack and will have efficiencies of their own.

@Ironic_Ape Point 3 is fair and but cvna is becoming smaller part of their book as other channels grow.

The key piece many miss is valuation. I love $lmnd as a company, was a very happy shareholder, but if $root grows 15% /year, $Lmnd has to grow IFP 78% per year for 5 years to match P/IFP

@Ironic_Ape i enjoy the dialogue as it forces us to refine our thesis.

my take:

point 1 is almost entirely irrelevant to me unless it accounts for the risk. segmentation is key, not absolute price.

point 4, better KPI imo is multi year look at IFP gained/$ spent.