Imagine analyzing and valuing Berkshire Hathaway back in the 1990’s by only looking at underwriting profit and the insurance cycle. And ignoring investments and capital allocation. That is what CIBC is doing with Fairfax today. Good luck with that type of analysis. $FFH.TO $BRK

🧵 1/10 Everyone’s talking about turnaround stories in athletic apparel — $NKE resetting, $ADI.NE grinding higher.

But one name trades at a fraction of the multiple with its founder back in the CEO seat executing a brutal reset.

$UAA (~$6, ~$2.5B market cap) on ~$5B revenue.

Here’s why the risk/reward looks heavily skewed right now.

There is a perception that Fairfax is not very good at investing. Of course, the facts tell the opposite story - over the past 5 years Fairfax has been consistently hitting the ball out of the ballpark. Importantly, enormous "hidden value" has been building. $FFH.TO $FRFHF

Today we do deep dive into one of the classics: The Outsiders - by William Thorndike. It is a quest in search of the great CEO, company and stock. What are the lessons? Capital allocation matters.. a lot. Click the link for more. $FFH.TO $FRFHF $BRK

https://t.co/ywQ8k5HVYE

Fairfax has already bought back an enormous number of shares in recent years at very low prices. Like Singleton, the strength of its business model is greatly under-appreciated and undervalued. As a result, aggressive stock buybacks will likely continue. Crazy but true. $FFH.TO

$FFH.TO picked up the pace on buybacks in May as expected. They bought back ~165k and cancelled ~160k. These are great prices. I hope they continue in June. I estimate they have $2.4b to spend on buybacks while still growing net premiums 5%.

One of Fairfax’s great strengths is they are very opportunistic. Their stock is - once again - wicked cheap. They know it. What to do? Back up the truck with buybacks. Time for another dutch auction? Or do they simply max out the NCIB. It is fun to speculate… $FFH.TO $FRFHF

Fairfax Financial stock $FFH / $FRFHF is down 20% from all-time highs…

Meanwhile, the BUSINESS continues its outstanding track record and create value for shareholders.

This may be one of the best opportunities right now 🤔

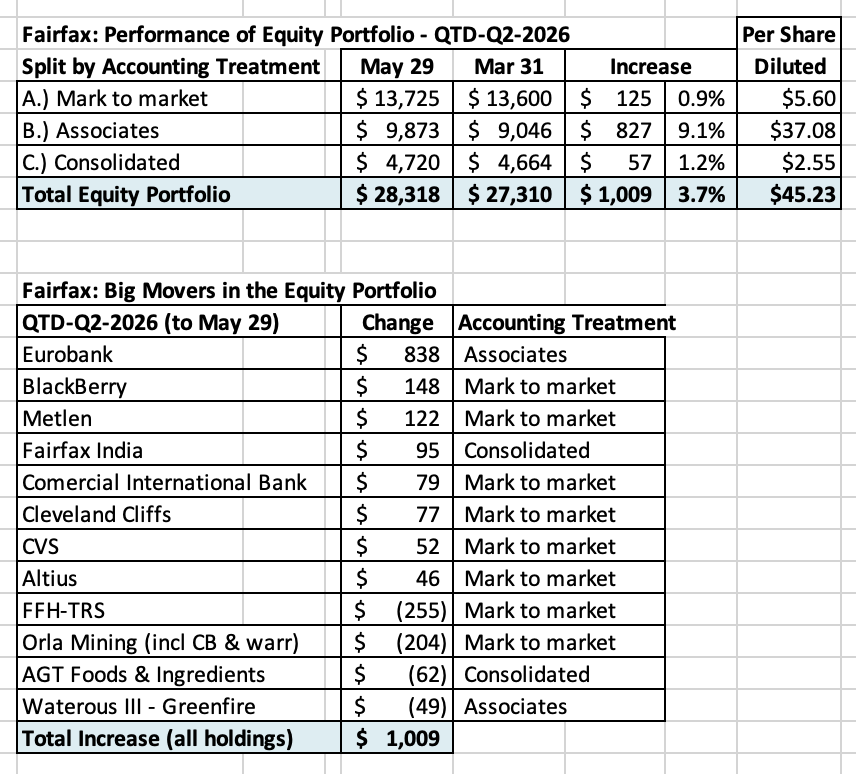

How are Fairfax's equity holdings performing so far in Q2? They are up about ~$1B or $45 per $FFH.TO share. Solid results. Eurobank continues to shine, up ~$840M. FFH-TRS is down ~$255M and looks like a coiled spring (poised to be a big driver of future results). $FRFHF $EUROB.AT

$FFH.TO closed on sale of Poseidon stake as expected. BVPS probably going to potentially come in around $1,300 or perhaps a little higher at end of Q2. The Eurolife transaction closes in Q3. Would not be surprising to see $1,400 book value at year end. At current prices that’s about 1.2x book at quarter end and 1.1x book at year end.

If you look at adjusted book for just the excess of fair value over book value in investments, could easily be over $1,550 at year end depending on how market positions perform.

Not a mystery why they are buying back so much stock right now. The stock is as cheap as it’s been since it was a huge gift several years ago.

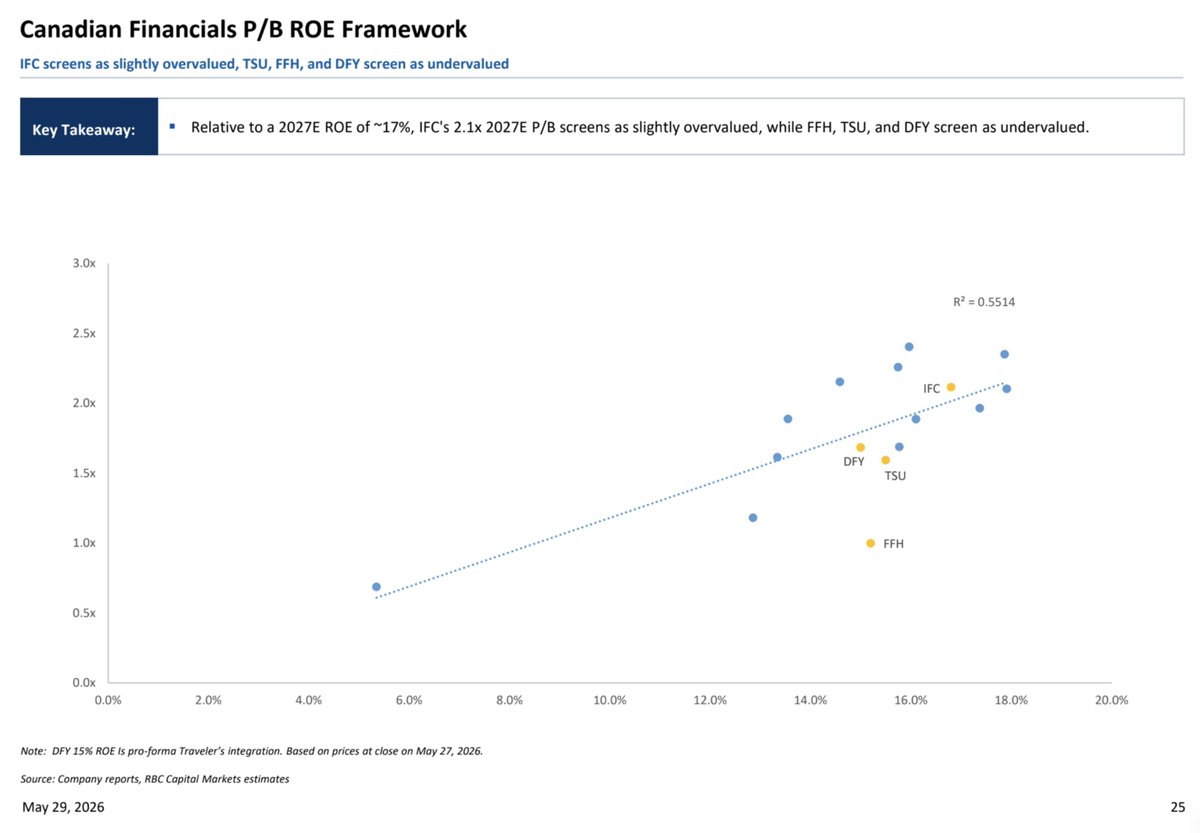

I think $FFH.TO is down in sympathy with $IFC.TO today. The market structure these days seems to ignore relative valuation. Most investors focus on historical valuation instead and ignoring expected ROE which are similar for these companies.

@LafontaineBrice@bsilly3@BrownMarubozu@VikingVan100 The company had issues during those 20 years - poor insurance CR in the 2000s, inflation hedges and shorts in the 2010s which went badly. Neither is the case today, so yes this time is pretty damn different.

My take on the Fairfaix $ffh Q1 2026 results. Apparently, Mr. Market and I are in strong disagreement about what this business should be worth. What am I missing? Looking for some pushback on the X machine that can prevent me from making this already sizable position even bigger.

Almost 3 years later, @BillBrewsterTBB invited @cfrischer1 and I back on to discuss $FFH.TO $FRFHF $FFH.

Since July 2023, I have more than doubled my position and added further on the weakness yesterday post results. Feedback is welcome and encouraged.

https://t.co/TaBCwRlqYz

@nh4y9hh7r7 Fairfax shareholders with a long term focus should be hoping for a lower share price. The stock is already cheap. Fairfax is buying back lots of stock - a lower price will let them buy back even more shares. Solid capital allocation - high certainty, solid return. $FFH.TO $FRFHF

Another earnings report being over-reacted to with $FFH.TO today. Underwriting was still strong at 94% CR and they bought back a lot of stock (no surprise at all), ~$630 million, decreasing S/O by 1.1%.

With the sell-off this morning, trading back to 1.31x book value and that doesn't include the now nearly $4 billion excess of fair value over carrying value embedded in investment portfolio, or about $190 per share.

Fairfax just deliver another solid quarter. EPS = $31. Increase in excess of FV over CV = $29/share. Increase in shareholder value in Q1 ~$60/share. Set up for Q2 is also very strong: sales of Poseidon and Eurolife will deliver $1.2B in pre-tax gains = $53/share. $FFH.TO $FRFHF