https://t.co/g2dK82BlK3 IMHO the best terminal rn @TrojanOnSolana Earn gold rewards through quests, rank ups and exchange those gold for jackpot entries! Super fun and rewarding 💰

Maybe a $TROJAN airdrop in future? Who knows 🤷♂️

An explanation for @saylor keeping the $STRC dividend unchanged is that they want to see whether the combination of semi-monthly payments and a rebuilt USD reserve fixes the discount before raising the rate.

The problem with STRC trading below par may not be the dividend rate itself. At 11.5% and a market price around $95, investors are already getting a very attractive current yield. The bigger issue may be confidence in the credit, liquidity, and balance sheet support behind the instrument.

By moving to semi-monthly payments, Strategy is trying to reduce dividend-cycle volatility, improve liquidity, and make STRC feel more like a real credit instrument. By rebuilding the USD reserve, they can strengthen the market’s confidence that the dividend is well covered and that the balance sheet is being managed conservatively.

So before increasing the dividend from 11.5% to 12% or higher, it makes sense to test whether better structure plus stronger reserves can move STRC back toward par.

Strategy also does not want to train the market to believe that every time STRC trades weak, the company will automatically raise the dividend. If traders believe “$95 means a guaranteed rate hike,” they can pressure the stock and force Strategy’s cost of capital higher.

Holding the rate steady sends a different message: the dividend framework matters, but it is not a mechanical formula. The board still has discretion. The company is going to manage STRC like a credit instrument, not like a panicked stock support program.

Keep the dividend steady. Increase payment frequency. Rebuild the USD reserve. Strengthen the balance sheet. Let the market decide whether the discount closes.

If that does not work, then a rate increase remains available. But it does not make sense to use that tool before seeing whether the structural changes and stronger credit support can solve the problem first.

Only ~5% of SpaceX stock is floating right now

~95% $SPCX is still locked

Most don’t realize bearish pressure often comes later, when insiders finally get liquidity

Unlock schedule below ⬇️

$SPCX’s IPO is mirroring $TSLA’s IPO pretty closely.

Everyone remembers what Tesla became. Few remember what happened right after the IPO.

$TSLA priced at $17.

It closed its first day at $23.89, up 40%.

The next morning it hit $30.42.

A week later?

$16.11.

A 47% drop from the high and below the IPO price.

Then came the part everyone remembers. Tesla went on to become one of the greatest investments in history.

But here’s the difference…

Tesla IPO’d at a valuation of roughly $1.7 billion.

$SPCX IPO’d at roughly $1.8 trillion.

That’s over 1,000x larger.

Great company doesn’t always mean great investment at any price.

Don’t let FOMO make your decisions.

Bitcoin ⬆️ 1.77%

MSTR ⬆️ 7.84%

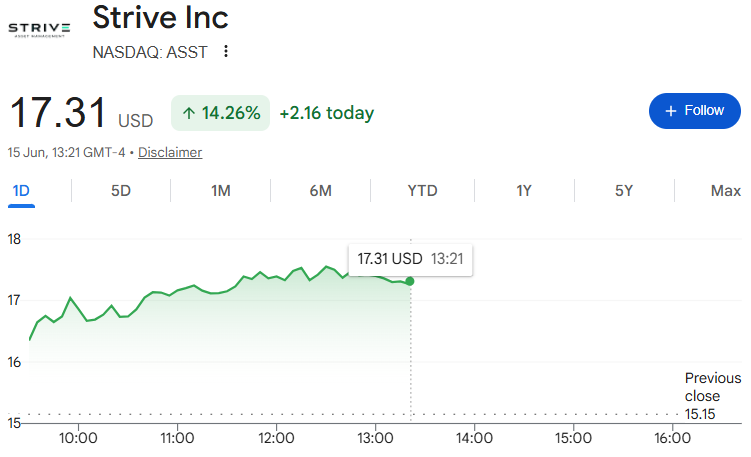

ASST ⬆️ 14.26%

Amplified Bitcoin works both ways. Bitcoin is sat at just under $67,000.

Now imagine what these stocks are going to do when Bitcoin trades at $200k - $400k

You. Are. Not. Bullish. Enough.

🚨 BREAKING:

BILLIONAIRE RON BARON SAID LIVE ON CNBC:

"SPACEX IS GOING TO BE WORTH $10T, $20T, AND $30T, AND I COULD BE VERY LOW."

THIS MAN BOUGHT THE 2008 CRASH AND CONTROLS OVER $53 BILLION IN ASSETS

HE DEFINITELY KNOWS SOMETHING!!

🚨 THIS IS HOW $SPCX ACTUALLY PLAYS OUT FROM HERE

Day 1 opens with a pump - retail floods in, peak FOMO, headlines everywhere

Insiders sell into every green candle

That's not cynicism - that's how 93% of major IPOs have behaved historically

Then comes the part nobody talks about on launch day:

Months of slow bleed while retail holds and prays

Momentum fades, attention moves on and another narrative takes over

Most day-one buyers end up underwater - sometimes for years

Meta IPO'd at $38 in 2012, dropped 53% in 100 days

The people who waited 6 months bought at $17 from the people who bought the hype

Same pattern now

$1.77T valuation at listing with 95% insider ownership is not an entry point

It's an exit point - just not yours

Two ways to play this:

1. Buy today and fund the insider unlock schedule

2. Wait until nobody cares, valuation reflects reality, and you buy from the people who bought from them

Same asset, six months apart - completely different trade

I'll be watching the 6-month window

Follow + notifs on, I will keep you updated

Grant Cardone reveals NOBODY would buy $10,000,000 worth of Gold at market price

“I know a guy who is trying to sell 10,000 pieces of silver and he can’t get a real offer. He’s getting a 30% discount below the market. People see it spiking like this and they’re like, ‘OMG.’ But go try to sell $10M worth of gold and see what happens. You’ll only get offers 20-30% below the market, and you won’t get the money tomorrow or in five minutes. It needs to get authenticated, checked, and validated”

“Bitcoin is a real thing. You can trade it in five minutes, and that’s real. Bitcoin, to me, is not only money, it’s also technology, unlike gold or silver”

AMD CEO Lisa Su just killed Nvidia’s $4,000 AI box with a $1,499 lunchbox.

She walked on stage, held it in one hand, and ran a 235 billion parameter model live. No data center. No cloud. No rented GPU.

The chip inside is something nobody saw coming. AMD’s Ryzen AI Max+ 395 is the first x86 silicon where CPU and GPU share the same 128GB of memory. That single trick lets a desktop run models that used to need a server rack.

Out of those 128GB, Linux hands the GPU 110GB to play with. For context, an RTX 5090 gives you 32GB. A 4090 gives you 24. This box gives you more than three times either of them, in a chassis the size of a thick paperback.

The benchmark that broke the room: this chip beat an Nvidia RTX 5080 by more than 3x on DeepSeek R1 inference. A $1,499 lunchbox outrunning a $1,000 discrete graphics card on a real AI workload. Nvidia spent a decade convincing the world you needed their hardware for serious AI. AMD just put that on a desk for half the price.

Here is what nobody is telling you. A heavy AI user right now pays $200 for Claude Code Max, $200 for ChatGPT Pro, $20 for Cursor, $20 for Gemini. That is $5,280 a year leaving your account. The box pays itself off in 9 months and then runs free for the rest of its life.

Install Ollama. Pull Qwen3 235B. Point Claude Code at localhost. Same interface you already use, except now nothing leaves your machine, nothing costs per request, and no company throttles your usage at 3am when you finally have time to build.

This is the moment every AI subscription becomes optional. Lawyers stop fearing OpenAI leaks. Developers stop watching the token meter. Founders stop renting H100s for prototypes that never ship because the bill scared them.

The first thousand people to figure this out will own the next two years of private AI consulting.

Save this, and read the full breakdown article below you are watching the next shift hit before everyone else does.

THE BITCOIN 12 MONTH RSI HAS ONLY PRINTED 4 MAJOR RED CLUSTERS SINCE 2010.

Just 4 times in 16 years.

Each one a generational buying opportunity.

Every single time this signal appeared...

What followed redefined what people thought was possible with money.

And right now in 2026 the 5th cluster is forming.

The chart doesn't lie.

It has only spoken 4 times in over a decade.

And every time it spoke it was right.

The 5th time is happening right now.

Most people are too scared to listen.

The ones who listened the first 4 times.

Never had to worry about money again.

#Bitcoin Generational Bottom?

Something caught my attention while applying standard Fibonacci retracements on Bitcoin’s logarithmic chart.

In each of the last three cycles, Bitcoin bottomed inside the exact same retracement zone:

78.6% – 88.6% Fib Retracement

If the pattern repeats, a potential generational buying opportunity could emerge around $39K.

Not my base case. But markets don’t care about our opinions.

Will history repeat itself?

@GMartin_0

Your math checks. One refinement actually makes your case stronger, claims should be net of cash, which raises net backing and moves the breakeven further in your favor

The construction you derived is CEBE mNAV, market cap over the BTC common equity actually owns after senior claims. Live column for 10 companies on the tracker

Kratter is wrong.

MSTR issuing ATM to buy BTC is accretive not dillutive at current multiples

----------------------------------------

Let's use today's numbers.

Before ATM:

BTC = $54B

Debt + preferred = $22B

Net BTC backing equity = $32B

Equity market cap = $43B

So shareholders are valuing $32B of net BTC at $43B, a 34% premium.

Now Strategy issues $4.3B of stock (10% dilution) and buys $4.3B of BTC.

After ATM:

BTC = $58.3B

Debt + preferred = $22B

Net BTC backing equity = $36.3B

But shareholders only gave up 10% of the company.

10% of the pre-ATM net BTC was worth $3.2B.

They received $4.3B of new BTC in exchange.

Net gain to shareholders:

$4.3B - $3.2B = $1.1B

In other words, when equity trades at a premium to net BTC, issuing stock and buying BTC is accretive, not dilutive.

The breakeven is not gross mNAV = 1.0.

The breakeven is when equity trades at net asset value after adjusting for debt and preferred.

Being an MSTR shareholder feels a lot like being a venture capitalist.

Not because the company is a startup.

But because of where you sit in the capital structure.

The preferred shareholders get paid first.

The bondholders get paid first.

The lenders get paid first.

Common shareholders are last.

You’re the shock absorber.

You’re the one who takes the volatility.

You’re the one who watches 30%, 40%, and 50% drawdowns.

You’re the one everybody laughs at when things get ugly.

But there’s a reason venture capitalists accept that risk.

Because the common equity holder is also the one with the greatest upside.

The preferred shares have a ceiling.

The debt has a ceiling.

The lenders have a ceiling.

Common equity does not.

As a regular investor, I don’t get access to SpaceX private rounds.

I don’t get access to Anthropic.

I don’t get access to the next billion-dollar venture deal before everyone else.

But through MSTR, I get exposure to a high-risk, high-volatility equity where the upside is theoretically uncapped.

That’s the trade.

You can’t demand venture-capital upside while demanding treasury-bill risk.

The reward exists because the risk exists.

If you’re not comfortable being the last one in line during difficult times, you won’t be around long enough to benefit from being first in line when value is created.

That’s why most people won’t hold MSTR.

And that’s precisely why the opportunity exists. ₿

Elon just created 4,400 millionaires in a single day.

400 of them are now worth over $100 million.

These aren't VCs. They're SpaceX employees, and the list includes welders, technicians, and cafeteria staff, because for two decades the company paid every level of the workforce in stock instead of higher salaries.

Juan Hernandez immigrated from Mexico and took a $28 an hour contractor welding job in 2015. He says he didn't even know what SpaceX was. The company gave him a $10,000 equity grant and let him buy more shares through payroll deductions. That stake is now worth $880,000.

Trevor Hise's parents wanted him to take a stable job at General Electric. He picked SpaceX instead, stayed 12 years, and accumulated over 100,000 shares. At the $135 listing price that's $13.5 million. He's 37 and semiretired. His words: "The magnitude of this has been ridiculous."

The most telling detail came before the listing. Over 100 employees quietly banded together and negotiated a group wealth management deal covering up to $5 billion, because none of them had ever needed a wealth manager before.

Software IPOs have minted millionaires for 30 years. This is the first one where the money went to the factory floor.

DO NOT FALL FOR IT

Today SpaceX goes public at $1.75 trillion

In the last 20 years the overwhelming majority of hyped IPO's were a DISASTER in first year

SpaceX is 10x hyped and 20x a big IPO's valuation

Meta: −30% in the first year

Uber: −25% in the first year

Rivian: −60% in the first year

Coinbase: −55% in the 1st year (since day 1)

It is not designed for retail to win

You buy at the top, early investors are up 100x to 1000x

Bankers will win, investors will win, early employees will win

AT YOUR EXPENSE

SpaceX is a great company, and you'll easily buy it at a discount in the next 365 days

Just be patient

We are pleased to announce that Metaplanet has entered into an agreement to acquire 100% of Siiibo Securities, a licensed Type I securities firm and a pioneer of Japan's online corporate bond market. Following closing, expected in July, the company will be renamed Metaplanet Securities. This is Metaplanet's first major acquisition and the first concrete step in Project Nova, our long-term strategy to build a Bitcoin-centric financial ecosystem in Japan.

The significance is hard to overstate. Japanese households hold roughly $7.4 trillion in cash, deposits and low-yield products, and as Japan shifts from deflation to inflation, that capital has begun searching for yield. By bringing Siiibo's Type I registration and online securities platform into the group, we will develop and distribute Bitcoin-related yield products directly to Japanese investors, supported by the 40,177 BTC on our balance sheet, the largest corporate Bitcoin treasury in Asia.

We have great respect for Kazuki Komura and the team at Siiibo Securities and what they have built. Together, as Metaplanet Securities, we will bring new yield opportunities to Japan.