Corrected:

Earlier we visited Sitka Gold, who have discovered over 5 mln ounces of gold, since I first visited this project in 2022

Their current 50k meters drill program might add a few more million ounces this year

Several major producers (I won’t mention names here) joined us on this site visit and showed great interest.

Next to their geologists, they also send business development/evaluation specialists

$MOLY Today we announced that the Government of Canada concluded its final due diligence and awarded our company a $7 million non-repayable contribution to evaluate the potential recoveries of by-product magnesium and rare earth elements. Canada is now the first G7 government to invest in mining in Greenland. More updates on our other equity capex financing efforts to follow😎

#Greenland #Criticalminerals #molybdenum #magnesium #REEs

https://t.co/7YqN6z3KMk

Gold weeklies: It's minor problematic that the last downswing was greater than the previous downswing. This makes it less likely that GC will put in a V bottom as well. 4077 is the 120 minute EMA, and that might be the play for now.

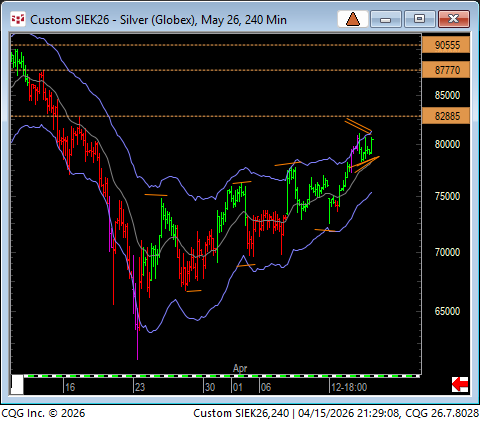

Cash Crude Oil

If we look at the monthly closing price chart we see a massive multi year channel

This would be a monster if completed above the 2022 high projecting price toward $200

The daily chart is coiling in a sym triangle

A busy first few months of the year for NGEx and more to come as we continue to put results out from our Phase 4 program, advance preparations to go underground, and work to move Los Helados forwards. Hear more from President & CEO, Wojtek Wodzicki...

JUSTIN HUHN (@uraniuminsider ) JUST LAID OUT THE CORE CASE ON SPROTT RADIO

• Supply cliff is real (per Huhn)

Cigar Lake ~2035. McArthur River ~2041. NextGen Arrow, the industry's "savior" deposit, ~2031 to 2032 for meaningful production (~230M lbs LOM). France’s fleet extension alone 250M lbs.

• Term market is where the story lives

Long term price $91.50 per lb (UxC and TradeTech). Cameco pushing market reference contracts ($85 floors and $160 ceilings). Utilities balking but no alternative supplier or substitute fuel.

• Strait of Hormuz risk is real but narrow

Husab (13 to 15M lbs per year) imports sulfur for acid leaching. Rossing and Kayelekera similar exposure. Kazakhstan largely domestic acid. Near term disruption, not structural.

• Demand side accelerating

China 33 reactors under construction, targeting 150 to 200 GW by 2035 (~56 GW today). France extending reactor lifetimes. Japan accelerating restarts. SMRs not modeled until ~2032, Huhn calls that conservative.

• U.S. back in the game (per discussion)

Westinghouse AP1000 deals discussed as large scale and strategic. Japan backing BWRX 300 builds in the U.S. NRC posture shifting.

Supply models do not balance for ~5 to 7 years. Risks skew to the upside.

$URNM $CCJ $URA $NXE $LEU $URNJ

@GavMcCracken@prb2o1o@Petro_Tal There's a spread with respect whether companies decide to offer a div. I don't know if there is a categorically correct answer.

@prb2o1o@GavMcCracken@Petro_Tal Sometimes when companies are stable they offer a div and are then included in etfs and other funds. Equinox gold is now offering a token div for that reason. Once they gain more liquidity sometimes multiples expand. Equity is then used elswhere.

@GavMcCracken@Petro_Tal Reasonable but the share price may have experienced significant volatility. Lots of o&g investors like the div. Buyback vs not is definitely a central point of discussion in energy. Buybacks at high share price may imply value destruction.

THE EX-CHINA RARE EARTHS ETF FINALLY EXISTS. HERE'S WHAT'S IN IT.

The first pure-play ETF focused exclusively on rare earths companies

outside China. Per Sprott, the only one of its kind in the Morningstar

Natural Resources Sector Equity universe as of launch.

TICKER: $REXC | Nasdaq | Inception: April 14, 2026

BENCHMARK: Nasdaq Sprott Rare Earths Ex-China Index (NSREXC)

HOLDINGS: 34 companies | 0.65% expense ratio

AUM AT LAUNCH: $2.04 million

TOP HOLDINGS (index weight):

· Lynas Rare Earths ($LYC) 22.85%

· MP Materials ($MP) 19.11%

· USA Rare Earth ($USAR) 5.85%

· Iluka Resources ($ILU) 5.24%

· Energy Fuels ($UUUU) 3.09%

SIZE SKEW: 43.86% small-cap under $2B. This is not a large-cap story.

DOMICILE MIX: Australia, U.S., Canada, UK, Chile, Guernsey

WHY IT EXISTS:

China controls roughly 70% of rare earth mining and 90% of refining.

Beijing's export controls in 2023 and 2025 turned that dependency into

a national security problem for every developed nation.

$REXC routes around that exposure entirely.

$REXC $MP $UUUU $LYC $USAR