How do you know stablecoins have strong pmf?

When Bitcoin maxi @jack had to add them to @CashApp even if he hates the idea 🤭

"I don't like that we're going to support stablecoins but our customers want to use them," he said.

Read more about how Cash App's 59M users can now use stables:

https://t.co/wc0FZSepii

Issue #4 of the Converge newsletter is out:

Big stories this week:

⇒ @DTCC sets July for live tokenized trades and October for full launch — Russell 1000, ETFs, and Treasuries, with Goldman, JPMorgan, BlackRock, Circle, @OndoFinance and 45+ firms in the working group

⇒ @OndoFinance, Kinexys, @Mastercard & @Ripple complete the first cross-border, cross-bank tokenized Treasury redemption — outside banking hours, settled in under 5 seconds

⇒ @WesternUnion launches USDPT on Solana — the world's largest remittance network goes on-chain

⇒ @Amazon builds AI agent payments with @Coinbase and @Stripe, putting stablecoins at the center of agentic commerce

Also worth watching:

⇒ @krakenfx parent acquires Hong Kong payments firm Reap for $600M + files for OCC federal trust charter

⇒ @Securitize gets FINRA custody approval + launches regulated trading venue with @jump_trading and @JupiterExchange

⇒ @BitwiseInvest takes over Superstate's $267M Crypto Carry Fund ⇒ Morgan Stanley E*Trade launches retail crypto for 8.6M customers

⇒ 19 European banks form Qivalis to build a MiCAR-compliant euro stablecoin on @FireblocksHQ

Check out the first issue of @DefiantNews's Converge newsletter, a weekly briefing on the highest-signal RWA, tokenization and stablecoin news & in-depth analysis.

Subscribe: https://t.co/bPtEQrOysz

Follow: @ConvergeDefiant

And that's just the newsletter. Converge website is loading :)

The debate around @circle and the $285 million Drift exploit has focused on whether the issuer failed to take steps to freeze the stolen USDC. I argue this framing misses the fact that Circle took active steps, under its sole control, to issue new USDC to the malicious party through its CCTP bridge.

Full analysis:

https://t.co/BLV71BrFrm

What does tokenization look like when it reaches the heart of U.S. market infrastructure?

Chris Storaker sat down with Tom Sullivan, Managing Director at @The_DTCC Digital Assets, to talk about:

- Why SEC clarity changed everything

- What DTCC is actually tokenizing

- Why collateral is emerging as the key use case

- How traditional finance and blockchain rails are starting to merge

This is one of the clearest conversations we’ve had on how tokenization scales from experiment to real market infrastructure.

🎙️ Watch the full interview below

We just launched Circle Nanopayments on testnet, and I want to explain the core problem this solves.

Let’s say you want to charge $0.01 for an API call, especially for agentic use cases.

That seems completely reasonable.

But the gas fee to process that payment costs $0.005. You just lost half your revenue to infrastructure.

Now imagine you want to charge $0.001 per request. The gas fee is still $0.005.

You are now losing money on every single transaction.

The payment literally costs more than the service itself. This is why pay-per-use models have not worked at scale. The infrastructure economics prevent it from working.

The most natural way to price digital services is by usage.

- Pay per API call.

- Pay per computation.

- Pay per data query.

These models are what power agentic commerce, where developers and AI agents need a financial rail built for high-frequency, high-volume payments.

Nanopayments solves this through batched settlement.

Instead of paying gas for every transaction, Circle’s Gateway aggregates thousands of payments and settles them together in a single onchain transaction.

The gas cost is distributed across all of those payments.

Here is the result:

- 1,000 payments that would normally cost $10 in gas fees now cost $0.01 total.

- That brings the cost down to $0.00001 per payment instead of $0.01.

Gas is no longer the limiting factor.

The way it works is straightforward.

You deposit USDC into a Gateway Wallet contract once. That is the only time you pay gas.

After that, every payment is just a cryptographic signature. You sign a message authorizing the transfer, but nothing is immediately broadcast to the blockchain.

The signature is verified instantly, you receive access to the service, and Gateway batches your payment with thousands of others for settlement later.

From a developer perspective, you make a request, the server responds with payment details, you sign the authorization, and you immediately receive the resource.

The entire interaction happens in milliseconds. There is no need to wait for block confirmations, and there are no individual gas payments for each request.

What this enables is true usage-based pricing.

- You can charge $0.001 per API call and maintain margin.

- You can implement pay-per-token pricing for AI inference.

- You can charge per second for streaming services.

Pricing models that were economically impractical because of gas costs now become viable.

This is particularly important for AI agents that need to autonomously pay for services.

An agent cannot operate if every $0.01 payment carries $0.005 in overhead.

When payments cost $0.00001 in overhead, the economics make sense.

Agents can pay for compute, for data, and for API access, enabling an autonomous agent economy.

We are live on testnet today.

Developers can start building with gas-free USDC transfers down to $0.000001.

This is what makes usage-based pricing viable.

https://t.co/H1QRs6omSC

Reach out to me if you need help building with this.

Nice headline today: Visa and Bridge are rolling out stablecoin-linked cards to 100+ countries.

My takeaways:

1. Cards are becoming crypto's gateway to real-world payments.

Anyone can hold stablecoins, and now they can spend them without going through the clunky QR codes and apps of the past. Just swipe a card.

2. While the UX is staying the same, the rails are being overhauled.

The actual news in this announcement is that Visa is using Bridge and Lead Bank to settle card transactions onchain (on Solana).

--

Now we'll have to see what adoption is like: how many more stablecoin-linked cards will be issued, and will people actually use them.

Days like today make you wonder why finance isn’t open on weekends

I’m sitting next to a macro guy discussing Iran strikes. While he’s speculating what markets will do on Monday I pull up Hyperliquid’s oil perp

+5% @ $86

Brain melted. Yeah - 24/7/365 tokenized commodity trading is going to explode

Holding stablecoin inventory is no longer capital-prohibitive for BDs.

@SECGov signaled that broker-dealers can apply a 2% haircut (vs. potentially 100%) to positions in qualifying USD stablecoins (under the Net Capital Rule).

Implications:

- Economically viable to hold stablecoin liquidity

- Lowers barriers to offer crypto services beyond ETFs

- Opens path to act as regulated USD liquidity bridges into crypto rails

- Crypto-native firms will face greater competition from legacy incumbents

As stablecoins make it into payment and securities settlement flows, this is a massive infrastructure opportunity for well-capitalized TradFi players.

https://t.co/UAlmruJUnN

Crypto fintechs are moving up the stack, slowly disintermediating legacy banks by pursuing their own bank charters.

Implications:

- crypto native firms will potentially get more direct access to Fed payments infra, which means

- stablecoin payments are getting more efficient

- reduced reliance on sponsor banks - banking as a service will have to evolve

to consider:

- is crypto finally moving away from regulatory arbitrage? will the edge be precisely in how it can ingrain itself in regulated rails?

Bridge has received OCC conditional approval to organize a federally chartered national trust bank. This will enable us to operate stablecoin products and services under direct federal oversight, including:

- Custody

- Orchestration

- Issuance

- Reserves management

Stablecoins are becoming core financial infrastructure. Institutions need regulatory clarity, operational resilience, and scalable systems to build with confidence. A national trust bank establishes that foundation.

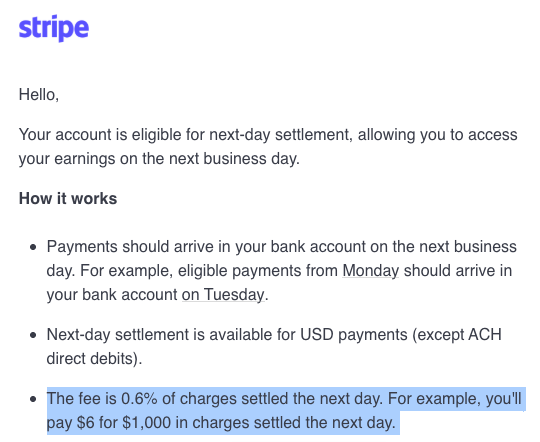

Visa USDC 7-day settlement is more interesting for acquirers than issuers.

Here's why:

• Merchants are willing to pay to get their money faster (PSPs like @stripe charge merchants ~0.6% for next-day settlement)

• For acquirers, it's easy to off-ramp 24/7 back to fiat via @circle

• For card issuers, this means lower pre-funding needs, but it comes attached with exposure to an asset that most treasurers don't know how to rate yet.

• Also re issuers, most issuing bank ops remain in traditional banking hours, so migrating card pre-funding to 7-day might be more of a burden than a meaningful operational gain.

For issuing banks to get on board, stablecoins need recognition as cash equivalents or similar balance sheet arrangements, or for tokenization to go far enough so that treasury teams are forced to bother with them.

--

https://t.co/yBtgQgoPzd

As these patterns mature, portfolio managers and treasurers will be forced to revisit their mandates and think more creatively about what “money” actually is in a programmable financial system.

We’re still early.

4/4

Tokenizing a fund is easy. Finding real traction is not.

@jpmorgan just launched MONY, a tokenized money market fund on Ethereum. The fund joins BlackRock’s BUIDL, Franklin Templeton’s BENJI, WisdomTree’s WTGXX, Fidelity’s FDIT, and others.

Sounds great but…

1/4

The unlock is in how crypto-native institutions are already using these funds today, showing how DeFi’s composable nature turns cash-like instruments into productive building blocks:

a) Interest-bearing collateral that remains economically active: Tokenized T-bill funds like BUIDL or BENJI being used as collateral in lending protocols or institutional DeFi venues, allowing holders to earn yield while securing credit.

b) Liquidity and reserve assets that can be dynamically redeployed: DAO treasuries or on-chain funds holding tokenized MMFs as a cash reserve that can be instantly moved between yield strategies, lending markets, or settlement venues without exiting to TradFi.

c) Composable balance-sheet primitives: The same capital can be pledged, referenced, and settled across multiple venues—used simultaneously for yield, collateral, and settlement—without breaking liquidity or triggering operational friction.

3/4

Spot on: RWAs won’t break out through issuance alone.

They break out when they work inside DeFi — permissioned where needed, composable by design.

Canonical tokenization is a big step toward

In our latest podcast, we spoke with @rleshner of @SuperstateInc - the takeaway is, DeFi needs RWAs and RWAs need DeFi:

"Bringing non-crypto-native assets on-chain is the only way DeFi becomes a massive financial system.”

But also, "tokenized securities only take off when they become useful building blocks in DeFi."

"The market is tiny — $300 million. We literally haven’t started.”

Watch the full interview with one of the founders who started DeFi and is now at the foundations of RWAs: