"Nobody buys a farm based on whether they think it’s going to rain next year. They buy because they think it’s a good investment over 10 or 20 years. It's the same with stocks. Think of stocks as a part ownership of a business. It's not that complicated." - Warren Buffett

Most people were never taught how to build real wealth.

They were taught to save pennies, chase titles, and feel guilty for spending.

Wealth isn't built by playing defense.

It's built with strategy.

Here are 8 principles to build lasting wealth - and enjoy it ↓

TL;DR - 8 Wealth Principles:

- Cash loses to inflation - invest it

- Buy back time, not things

- Earn more, not just spend less

- Build income you own

- Debt narrows options - stay clean

- Think in 5-year windows

- Discipline beats hot takes

- Build it. Use it.

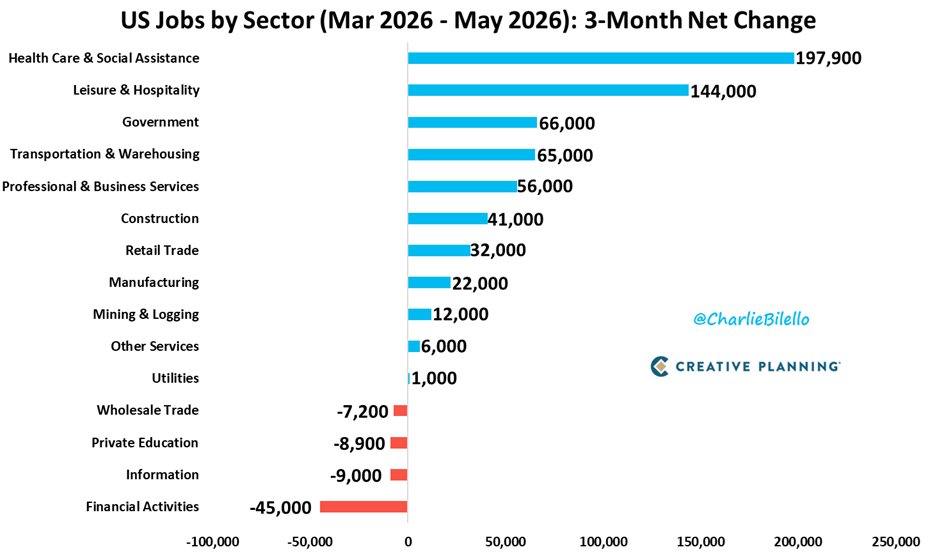

60% of the job gains in the US over the last 3 months came from just two sectors:

1) Health Care & Social Assistance: +198k jobs

2) Leisure & Hospitality: +144k jobs

One of the strangest things about retirement planning is the rule everyone follows was never meant to be a rule.

You meet retirees in their 60s afraid to take the trip, convinced they have to live on 4% of their savings forever.

Then you meet the man who wrote the 4% rule.

He calls it a worst case backtest. He's spent 30 years saying the real safe rate is closer to 7% (which can be wrong as well). He just wrote a book asking retirees to spend more.

The author isn't using his own rule. Neither should you.

Real retirement planning is a year by year cash flow plan. It starts with the variables a percentage will never see.

How long the money has to last.

When Social Security turns on, and at what amount for each spouse.

Whether there's a pension. What other income shows up, and when.

The mix of taxable, tax deferred, and Roth dollars you've built.

The age gap between spouses.

The state you live in.

The healthcare costs sitting between retirement and Medicare.

The IRMAA brackets after you get there.

What the surviving spouse faces when they start filing single.

Then it lays out the year by year decisions.

Which accounts to pull from, in what order, in what year.

Where the Roth conversions fit.

How to fill the low bracket years before Social Security and RMDs hit.

When to harvest gains. When to take losses.

And it has an answer for a market correction or crash in the first 3 years of retirement. A static withdrawal turns that drop into permanent damage, selling more shares at lower prices from a portfolio that should have recovered.

A real plan knows what to scale back on, and for how long. It doesn't sell at the bottom because it doesn't have to.

A percentage doesn't know any of that.

S&P 500 earnings are now expected to increase by 25% this year. We've never seen earnings growth this high outside of post-recessionary rebounds. An unprecedented boom fueled by massive EPS gains in big tech.

Video: https://t.co/HdoFAnN6sC

Stephen Meyer has absolutely destroyed Naturalism.

Nothing explains the universe and the Life within it better than an eternal, Divine Creator.

Here are the 4 most powerful points from his recent conversation with Phil Halper 👇

Historic Crashes in the U.S. Stock Market

1907 Panic — Decline: -48%, Recovery Time: 10 years

1929 Great Depression — Decline: -89%, Recovery Time: 25 years

1973 Oil Crisis — Decline: -45%, Recovery Time: 9 years

1987 Black Monday — Decline: -36%, Recovery Time: 2 years

2000 Dot-com Bubble Burst — Decline: -78%, Recovery Time: 13 years

2008 Financial Crisis — Decline: -57%, Recovery Time: 5.5 years

2020 COVID-19 Shock — Decline: -34%, Recovery Time: 6 months

2022 Rate Hike Shock — Decline: -27%, Recovery Time: 18 months

2025 Tariff Shock — Decline: -23%, Recovery Time: 1.5 months

2026 Expected Rate Hike Shock — Single-day decline: 4.8%

The Nasdaq Composite fell 4.18% in a single day, marking the steepest drop since April 2025.

The Philadelphia Semiconductor Index plunged 9%, wiping out over $1 trillion in market value in one day.

$NVDA dropped 6.2%, $MU fell more than 13%, $AMD nearly 11%, and $AVGO lost nearly 19% over two days.

During my research, I noticed:

The recovery cycle after crashes seems to be shortening year by year.

This suggests that the current downturn may be an excellent buying opportunity.

Capital is being reshuffled, and those who dare to position themselves early could be turned into millionaires in the next market cycle.

NAR Chief Economist Lawrence Yun reacts to the latest jobs report, which shows the labor market strengthening, with 172,000 net new jobs in May. Upward revisions to previous months brought cumulative job gains to 565,000 over a three-month period — among the strongest in recent years.

One of the biggest misconceptions in high school sports is that coaching is primarily about practices, games, and wins.

The reality is that coaching has become one of the most challenging roles in education because coaches are expected to wear dozens of hats while being evaluated from every direction.

Every parent, player, administrator, and community member often has a different expectation of success.

One family wants college recruiting to be the priority.

Another wants playing time.

Another wants winning.

Another wants player development.

Another wants discipline.

Another simply wants their child to enjoy the experience.

The challenge is that those goals frequently conflict, and coaches are often expected to satisfy all of them simultaneously.

Most coaches are balancing far more than what happens between the lines. They manage team culture, player conflicts, parent concerns, academics, transportation, fundraising, budgets, equipment, scheduling, eligibility, social media issues, and the emotional needs of teenagers.

At the same time, every roster includes athletes with different abilities, goals, motivations, and commitment levels. Some dream of college athletics. Some are trying to make varsity. Some simply want to belong. Building one program that serves all of them is incredibly difficult.

Perhaps the greatest challenge is decision-making.

Who starts?

Who plays?

Who sits?

Who travels?

Who gets moved up?

Who gets cut?

Every decision creates opportunity for one athlete and disappointment for another. Even well-intentioned decisions can be viewed as favoritism or politics when seen through the lens of an individual family.

Recruiting adds another layer of complexity. Coaches are expected to help athletes pursue college opportunities while also managing the needs of an entire team. Supporting one athlete can sometimes raise questions from another family about their child’s opportunities.

Social media has amplified many of these challenges. One lineup decision, one difficult conversation, or one emotional moment can quickly become public discussion, often without the full context.

There are also pressures many people never see.

Pressure from administrators to represent the school well.

Pressure from parents to provide opportunities.

Pressure from athletes to help them achieve their goals.

Pressure from communities that often measure success by wins and losses.

Pressure to retain athletes in an era of increasing transfers and movement.

And all of this occurs while coaches are trying to develop young people, not just athletes.

What makes coaching difficult is not that people don’t care.

It’s that everyone cares deeply, but often about different things.

Parents focus on their child.

Players focus on their opportunities.

Administrators focus on the school.

Communities focus on results.

Coaches must somehow balance all of those interests while making decisions they believe are best for the team.

As a former college coach, athletic director, and high school administrator, I’ve learned that most coaches are not trying to hold athletes back, play favorites, or make life difficult for families. Most are simply navigating competing priorities, limited resources, and difficult decisions while trying to do what’s best for kids.

Because at its core, coaching has never really been about managing games.

It’s about managing people.

And that’s what makes it both incredibly challenging and incredibly important

Kevin O'Leary reveals the trust fund structure he set up for his kids the day after he became rich

"When the learning company got sold for about $4.2 billion and 10 of us were founders, we woke up and said we're rich. I went to the lawyers and said I want to set up a trust that pays for my kids until they finish college and then they get nothing"

"The lawyer said what the hell's that. I said it's a way I can provide for them to set them up in life but not entitle them. I was taking a cue from my mother's strategy"

His mother's strategy:

"When I graduated, my mother said I've got great news, I'm coming to the graduation, but I also have some other news, no more checks. I said what do you mean. She said the dead bird under the nest never learns how to fly. No more checks. You're going to have to figure this out on your own"

"I had a tough couple of years. I couldn't even pay the rent. But it worked out and I got motivated"

We tend to read our hardest seasons as evidence that something has gone wrong. The job loss, the diagnosis, the prayer that hasn't been answered the way we hoped — surely these are detours from God's good plan.

But Scripture tells a different story. The very things we'd never have chosen are often the very things God uses to grow us into who we were always meant to be. Trials aren't the interruption of grace. Sometimes they're the delivery vehicle for it.

What growth has come through a trial you'd never have chosen?

Jim Abbott's amazing no-hitter has to be up there with one of the most underrated athletic achievements of all time. I mean, even within the baseball community, it's not talked about a lot at all.

And this was against what would become one of the most dominant offensive line ups in the mid to late 90s. Lofton, Baerga, Belle, Ramirez Thome, Alomar jr.

The Story of Everything was only supposed to be in theaters for ONE week…

But audiences kept showing up, so it’s now extended through May 17 🎟️

What caused the universe to exist in the first place?

See the film audiences can’t stop talking about 🎬

$100,000 invested in 2000 in a basic S&P 500 index fund.

By 2010, after two of the worst crashes in modern history, you had roughly $90,000.

A lost decade. Flat or slightly negative for 10 years.

But the investor who stayed and didn't touch it? By 2024 that $100,000 had grown to over $600,000.

Patience is sometimes the entire strategy.