$META wedge update 📈

Monthly FVB support held again.

Wedge is breaking out.

We are NOT in a full bull cycle yet.

Close over $700 would likely flip the weekly FVB

Strong breakout setting up for the next 6 - 12 months

Does this feel fair to ignore? A company combining AI mineral exploration, millions of geological records, and a copper-focused project in British Columbia while the market is focused only on today’s red candles.

$ARM $IESC #Yash

Let me tell you what most people are missing… copper weakness today doesn’t change the long-term supply problem. NRED gives exposure to copper, AI mining, and future discoveries.

#HoodiesOn#ARGxEGI#omegle $SRPT $RKLB VOD

THIS CHANGES THE SETUP... NRED has Wilmac at 16,078 hectares, but the part that caught me is how copper is moving beneath the headline market.

#momson#ometv#monkeyapp#TejRan NVDA TSLA AMZN META JPM UNH TSM

Yo metals crowd, China just gave us a small signal with a big meaning.

Copper scrap moved higher across several grades: CNY 400/ton for the main wire and tubing categories, CNY 200/ton for 85% recovery insulated wire, and CNY 100/ton for heater cores.

Meanwhile, many aluminum and steel grades stayed flat.

That contrast matters to me. Copper is the metal getting repriced inside the recycling market, which usually happens because the physical chain wants more of it.

That is the backdrop where $NRED makes sense: Wilmac, 16,078 hectares in BC, and MetalCore AI working to identify better copper-gold-platinum targets.

Source: https://t.co/xcZHSzA7rP

NFA

$META $AAPL $MU $XRP $ETH $NOK $DELL

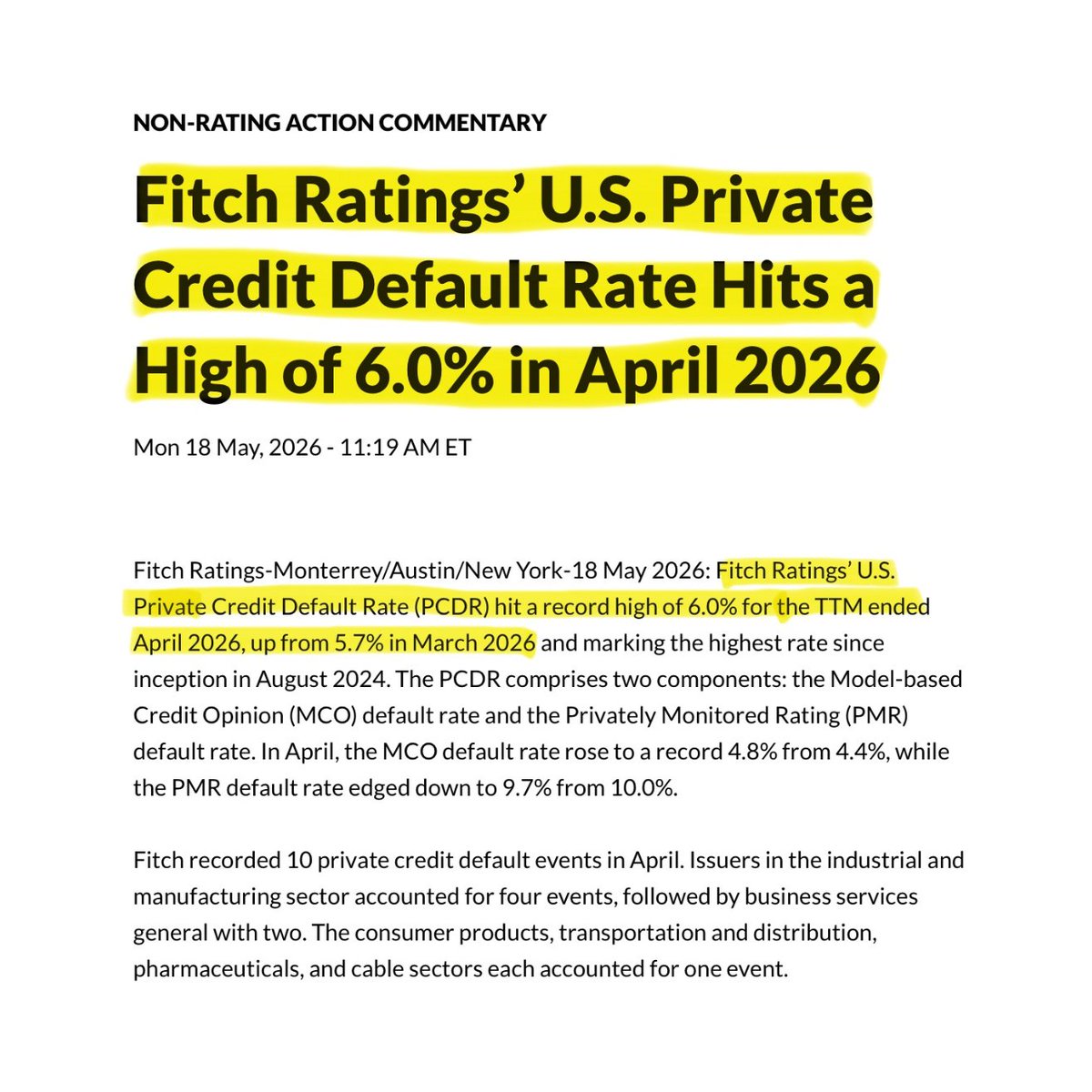

🚨 PRIVATE CREDIT MAY BE THE TRIGGER FOR THE NEXT FINANCIAL CRISIS.

Private credit defaults just hit their highest level ever recorded. Fitch's U.S. Private Credit Default Rate hit 6.0% through April 2026.

That's the highest since this data started being tracked in 2024.

Just three months earlier, in January, it was 5.8%, which was already a record at the time. For all of 2025, defaults came in at 9.2%, beating the old record of 8.1% set in 2024.

And the real number is worse than what's reported.

Some borrowers are avoiding an official default by paying their interest with more debt instead of cash. This is called a PIK loan.

The lender still counts it as income, even though no actual cash came in. This practice has more than doubled since 2022, from 5% to 11% of all private credit loans.

Companies using this method have pushed their debt up to 76% of their total assets, up from 40% three years ago. It's a way of delaying a default, not avoiding one.

Two of the biggest lenders, Ares Capital and Blue Owl, both said around 15% of their income last year came from these non-cash payments. The clearest real example of the risk is Medallia.

Thoma Bravo bought the software company for $6.4 billion in 2021. Its revenue later stalled because of AI competition, and lenders had to take control of the company. $5.1 billion in shareholder value was wiped out, and the loans were marked down to 60 cents on the dollar.

Blackstone, Apollo, and FS KKR all took losses on this deal.

Software companies are a big part of the risk here, making up somewhere between 19% and 35% of private credit loans, depending on the estimate. Morgan Stanley expects 11% of these loans to come due by the end of 2027, with another 20% due the year after.

That's when companies will need to refinance old debt, and many may not be able to on the same terms.

At the same time, investors are trying to pull their money out of these funds. In the first quarter of 2026, they requested $13.9 to $20 billion in withdrawals. Only about $7.4 billion, roughly half, was actually paid out.

Some investors selling their positions on the secondary market are accepting 30% to 65% less than the fund's stated value, just to get their cash back sooner.

The part that gets the least attention is who actually holds this risk. U.S. life insurance companies hold $849 billion in private credit. If defaults keep rising, insurers are the ones who absorb it, not banks.

That risk moves quietly through retirement and insurance policies, long before it shows up as a major headline.

Warren Buffett has said the risk is more serious than that, pointing to how connected banks already are to this market. Either way, the default rate is already at a record, and the loans most at risk from AI disruption haven't come due yet.

$CRCL received final OCC approval to launch Circle National Trust as a federally regulated trust bank.

The bank will custody digital assets for Circle and its affiliates and could later manage USDC reserves and serve select institutions.

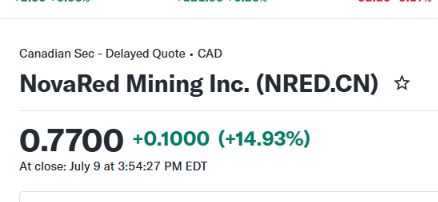

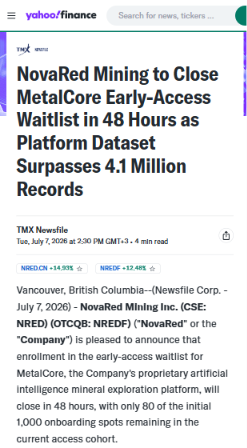

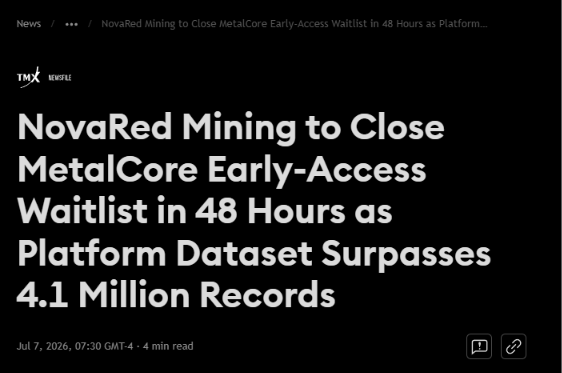

I’ll be honest with you… red days expose weak stories. NRED still has the same thesis: copper demand, AI data advantage, and 39,726 acres of exploration upside.

$PDD $GRAB #omegle#omegle#ometv#momson

I’ll be honest with you - when a tiny mining name has 92% of its first AI platform cohort filled before the window even closes, I pay attention. NRED has 48 hours left and only 80 MetalCore spots open.

$CDE $UUUU

HOLY SH*T... SKHY demand reportedly running 7x and NRED is tied to the copper side of the AI chain.

Let me tell you what most people are missing here.

#omegle#momson#teenagee#HoodiesOn AAPL MU VTAK NCRA IOTR IE EA CLSK

AI runs on GPUs, memory, power, and copper.

SK Hynix is preparing its U.S. Nasdaq debut under ticker SKHY, with 177.9M ADS representing 17.79M common shares. Demand for the offering is reportedly running at 7x the available shares, and the company is aiming to raise around $28B.

Why does this matter for $NRED / $NREDF?

Because the AI buildout is much bigger than chips.

High-bandwidth memory helps AI processors move critical data faster. Data centers need that memory, but they also need massive power infrastructure. Power infrastructure needs grids. Grids need copper.

That is the bridge.

SK Hynix shows the scale of AI hardware demand.

NovaRed sits on the raw-material side of the same chain: copper-gold exploration, Wilmac in British Columbia, North American critical minerals, and MetalCore AI-driven targeting.

AI needs memory.

AI infrastructure needs copper.

$SPCX $ORCL $SPY $QQQ $CLSK $WMT $ETH

BREAKING: Nvidia, Meta, Alphabet, and Microsoft lost $191 billion today while chip and memory stocks added $245 billion.

Micron +6.6%, $70B added

Broadcom +3.18%, $57B added

AMD +5.81%, $49B added

Intel +5.3%, $28B added

Western Digital +7.50%, $15B added

SanDisk +5.63%, $14.5B added

Seagate +6%, $11B added

Nasdaq 100 +1.30%, $500B added

S&P 500 +0.30%, $205B added

Meanwhile:

Nvidia -1.07%, $51B wiped out

Alphabet -1.35%, $58B wiped out

Meta -2.82%, $44B wiped out

Microsoft -1.34%, $38B wiped out

Micron's $250B U.S. investment plan through 2035 and Apple's new supply deal with Broadcom are driving the entire sector higher.

JUST GIVE IT TO US...

$SPCX just need the break and retest of 148-150... Then we will see the 135-140 push, worth mentioning $SPY $QQQ are bouncing but SpaceX is just stuck here at lows.

CLEAR WEAKNESS, dont chase but look/wait for the reaction👇

The headline looked boring. The details were not boring.

NRED mixing mineral exploration with AI data is the kind of shift I like watching early.

#HoodiesOn#Tabaahi#Yash NCRA IOTR NOK LINK DELL HIMS MU

Blood on the street is where the best entries usually hide.

I’m holding $NRED because the copper story is bigger than one red day, and AI-driven exploration gives this name a different angle.

Buy the dip. HODL. hold!

$INTC $NVDA $ORCL $AAPL $SPY $QQQ $BABA

IRAN War continues...

$WTI looking to get back into 80.50-81 here, First major level I'd be watching. The SPR is also CRITICALLY lows according to most reports.

MAJOR WATCH

Jeff Bezos Blue Origin is reportedly raising outside capital for the first time seeking $10B at a $130B pre-money valuation.

This is very bullish for $RKLB which still trades around a $48B market cap as one of the few pure-play space infrastructure names.

$NQ $ES $QQQ

Wow day today.

More than 2% clean gain points from Nasdaq

Market makers gave retail clean move entries. Days like this will need to be utilised more than anything.

BREAKING: Broadcom is up 4% after Apple announced a $30 billion chip deal with the company.

The contract runs until 2031 and covers custom silicon components and next generation wireless connectivity chips used across every Apple product.

Broadcom will invest $1.5 billion to expand its manufacturing facility in Fort Collins, Colorado, where it will produce the radio frequency and wireless chips that connect iPhones to Wi-Fi, Bluetooth, and cellular networks.

This is Apple's largest US manufacturing commitment to date and part of its broader pledge to invest $600 billion in the US economy over four years.

Last month Apple signed a preliminary agreement to potentially buy $9 billion worth of chips from Intel.

Combined with today's Broadcom deal, Apple is signaling a major push toward US-made chips across its entire supply chain.

Broadcom's AI chip revenue hit $10.8 billion last quarter, up 143% from a year earlier. The company is targeting over $100 billion in AI semiconductor revenue for the full fiscal year.

The announcement sent shockwaves through the entire chip sector. The Nasdaq 100 bounced 1.60% from its day low. SanDisk surged 14% from its day low. Micron recovered 6% from its day low after a brutal two week decline.

Not saying this is a gem yet, but it definitely made me stop scrolling. NRED just crossed 4.1M records on MetalCore, up from 2.7M+, with 920 users already registered. Actual milestones are what get my attention.

$DRAM $UUUU

Not saying this is a gem yet, but it definitely made me stop scrolling. NRED is building something different with 4.1M+ geological records, including 1.5M geochemistry records and 800K+ deposit records. AI + mining is a combo I’m paying attention to.

$NOK $ONDS $DXYZ