@LuisAntonV Very bullish. Since they de-risked with the LAR acquisition.

12 million dollar grant/ loan to pay for part of the upgrade to LAR facility can't be overlooked.

$DRX.TO Beat on analist expectations.

Beat on revenue

Beat on margins

Bear on earnings

Down 12% or so in last 3 days. Probably due to people scared of this results being weak.

Let's see the conference call as they have a quite healthy cash balance and we could have a buyback.

@Stocks_Stones is one of the best micro-cap investors I know, highly suggest listening in to this to hear more about his process and top picks.

Couple @Atrium_Research names mentioned on there too $DRX.TO $LOVE.TO

I recently bought $DRX.TO - ADF Group, a Canadian fabricator of complex structural steel. They have 2 fabrication facilities in Quebec and 1 in Montana.

The stock recently sold off on near-term margin noise tied to steel tariffs and their LAR acquisition, creating what I think is a really good entry point

Why It's exciting:

1. Trades under 4x depressed EBITDA with a clean net cash balance sheet

2. Backlog has more than doubled in a year from $300m to $650M+, with strong bidding activity continuing.

3. Beneficiary of the "Build Canada" Thematic

4. A recent acquisition I believe will look like a no-brainer in hindsight

ADF is one of the best-positioned names to play the 'Build Canada' theme. They stand to benefit from a wave of infrastructure spend: airports, Ontario nuclear, hydro expansion in Quebec, BC, and Newfoundland, and energy/industrial buildout in the west. A "Buy Canadian" mandate further improves their competitive position and will spur industria/constructionl projects

Historically, they were 90% US, 10% Canada. However, with last year's tariffs, the company has aggressively pivoted its backlog which now sits at 60% Canadian and 40% US with a good chunk of the work segregated between the two countries. I expect Canada to make-up a bigger percentage of the mix overtime.

The most exciting part of the story is the LAR Group acquisition. Historically, ADF Group did primarily industrial & commercial projects. Think airports, warehouses, bridges and some industrial plants. LAR was a distressed, over-levered steel fabricator for the hydro sector. A specific contract blew them up and ADF stepped in as the white knight through a reverse vesting order approved by the government. It allowed them to acquire LAR's assets while having all liabilities extinguished, BUT keeping all certifications intact.

ADF is now certified to operate in both the hydro AND nuclear markets two of the most infrastructure-intensive sectors in Canada's near-term pipeline, in addition to potentially bidding for some of the big 'nation-building' projects the Canadian government has proposed.

The near-term overhang: LAR is working through a tail of low-margin legacy projects, which weighed on Q4 results. LAR currently runs ~10% gross margins vs. ADF's mid-20s. Management doesn't expect margins to deteriorate further from here, but the meaningful inflection only comes in H2 2026 and into 2027, as ADF deploys ~$35M to automate LAR's facilities. LAR is understood to be the preferred vendor for virtually all Hydro-Québec projects and so I expect more work to come their way. And let's not forget the government of Quebec approved the CCAA proceeding at record speed. Clearly Hydro-Quebec was pretty desperate to have ADF acquire LAR group as there aren't many companies capable of doing that type of work.

The second near-term overhang is the recent US steel tariff changes which puts a 10% tariff on the total value of steel transformed outside of US, but that uses US Steel. For some jobs, it made economical sense to ship US steel to Terrebonne and then ship it. It will impact their Q1/Q2 results, which caused last week's sell-off.

The market is focused on near-term headwinds but It's missing the forest for the trees.

Canada is entering one of the largest infrastructure build cycles in its history and ADF is one of a handful of Canadian companies capable of fabricating the complex steel structures these projects demand:

=> Hydro-Québec: $35–45B capex plan over the next decade

=> BC Hydro: $36B in regional investments over the next decade

=> Ontario & Atlantic provinces ramping hydro capacity

=> Ontario nuclear: plant refurbishments, SMRs, and Bruce Power expansion

And none of that includes the 15 'nation-building' projects the federal government has fast-tracked or the hundred of projects that will emerge from Canada's defense spend goal of 5% of GDP.

Despite the headwinds, the company expects to have stable gross margin, with a much bigger revenue number. There is a clear path here for the company to achieve 15% EBITDA margin on potentially over $500m of revenue which would get me to a target price of $17 at 6x EBITDA over the next 2-3 years.

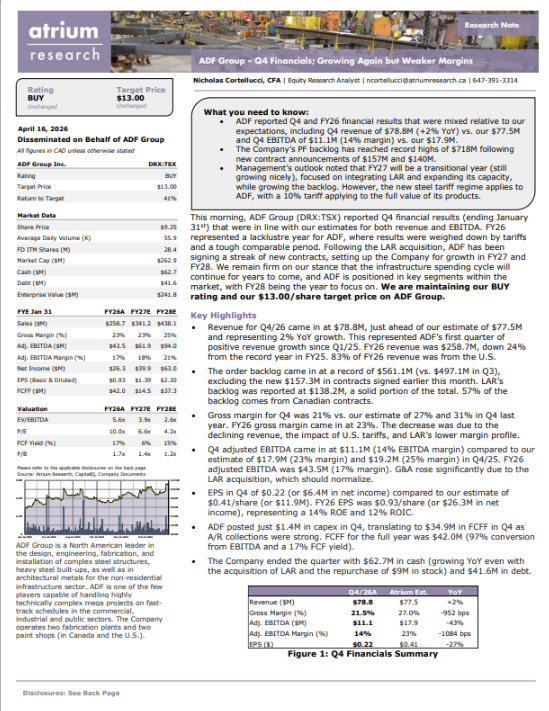

Our team has published a research note on ADF Group inc. ADF reported Q4 and FY26 financial results that were mixed relative to our expectations, including Q4 revenue of $78.8M (+2% YoY) vs. our $77.5M and Q4 EBITDA of $11.1M (14% margin) vs. our $17.9M. $DRX.TO

🔍 Read the full report below!

📰 Disclosure: Disseminated on Behalf of ADF Group

$SOMA.V small position in portfolio. Each passing week with gold over $4500 is going to do wonders to the FINS for soma. What's everyone else's favorite gold miners.

@ZiemzFinancial Tarriffs IMO are short term noise. I ask myself is this permanent?

My answer is always "no.

So depending on your investing timeline it may effect $DRX.TO revenue growth in short-mid term.

Overall management has proven to me they can handle tough macro. Coming out on top.

Great news for $DRX.TO yesterday, with a 157m in new contracts announcements yesterday.

Despite the tough macro with steel tarriffs. ADF continues to execute. Up 40% in last 6 months. With the LAR acquisition completed. Looking forward to 2026

Earnings 6 days away!

@Phoenix_FFM@LuisAntonV@Michhhhh43 Exactly the uncertainty delays contracts as companies are not willing to commit when pricing can change. So as soon as we have a permanent rule set for the industry . I imagine Us revenues will increase.

$DRX.TO expected to have 25% return by end of year according to Keystone Financial. They can't officially release name. No a keystone financial subscriber but am able to read between lines as I'm well researched on ADF Group.

@Phoenix_FFM@Michhhhh43 As far as I'm aware the steel sectoral tarriffs are still in place. But market is forward looking "allegedly". People/ news are saying that steel tarriffs will be struck down or negotiated lower, as tariffs are more disliked. Just my opinion. Very strong momentum for $DRX.TO

When $DRX.TO is now most stable position in your portfolio. Holding very strong on a red day. Seems we have finally gotten a strong investor base. Still bullish with recent institutional purposes.

@Michhhhh43 I agree I think closer to 50% return is in the cards with a few good quarters and a contract announcement to bolster backlog . Possible catalysts include any reduction in steel tariffs from the US. $DRX.TO

$DRX.TO finally receiving the gold stamp of approval from Keystone Financial. Very bullish for me as they were one of biggest bears. Nice to see momentum. 2026 should be a good year.

$drx.to quietly navigating this tough macro environment and still producing good net income. Overall solid performance. Company significantly de-risked with LAR acquisition.

I feel like this news is being heavily overlooked with other Microcaps reporting earnings. $DRX.TO will hopefully be able to capitalize on Canada. LAR acquisition may end up being an extremely lucrative move.

Strong headwinds after yesterday's announcement from Carney. Take the time to listen to yesterday's interview. Tarriffs to assist the CAD steel industry take effect January 31st. $DRX.TO https://t.co/DdVsrpyObA