I can confirm this as a trader with 8 years of experience

I’m long $SNDK $MU $INTC $NBIS $LITE $ALAB $AAOI $GLW from June lows in my trading account, a top-tier list in terms of business quality imo, and the decision making was simply this:

opened tradingview

placed the price change tool from ATHs to lows

see -20% to -30%

instant long

It is still AI or nothing. Only money tells the truth.

A little bit of background, a Z‑score tells you how extreme the flow is compared to before.

In other words, >+2 = people keep buying

>+3 = people buy like there's no tomorrow, and vice versa

The US is still the biggest winner. We're gonna win so much you may even get tired of winning.

So, the emerging markets are just TSMC and Samsung and SK Hynix.

Funds are dumping financials + consumer goods to make room for tech.

It’s productivity vs. rate‑sensitivity.

Sell banks and consumer names (rate peak + soft consumption). Buy AI.

Clear rotation signal.

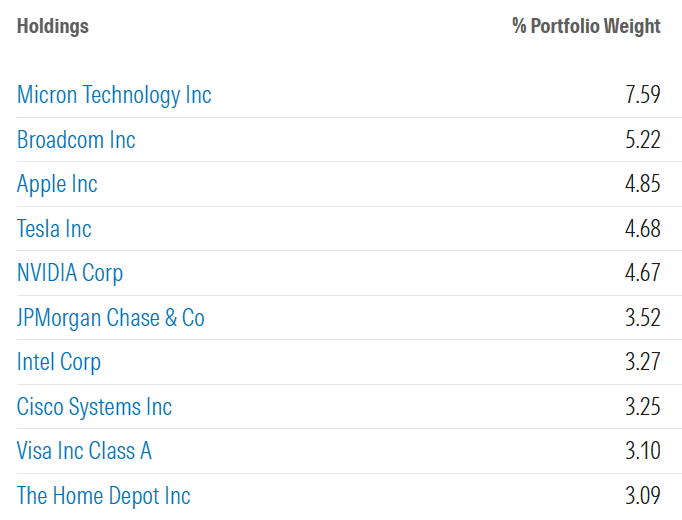

The Vatican Bank has a US equity index that tracks stocks that are "consistent with Catholic teachings"

Top 10 positions:

1. $MU 7.59%

2. $AVGO 5.22%

3. $AAPL 4.85%

4. $TSLA 4.68%

5. $NVDA 4.67%

6. $JPM 3.52%

7. $INTC 3.27%

8. $CSCO 3.25%

9. $V 3.10%

10. $HD 3.09%

Hilariously ironic index composition.

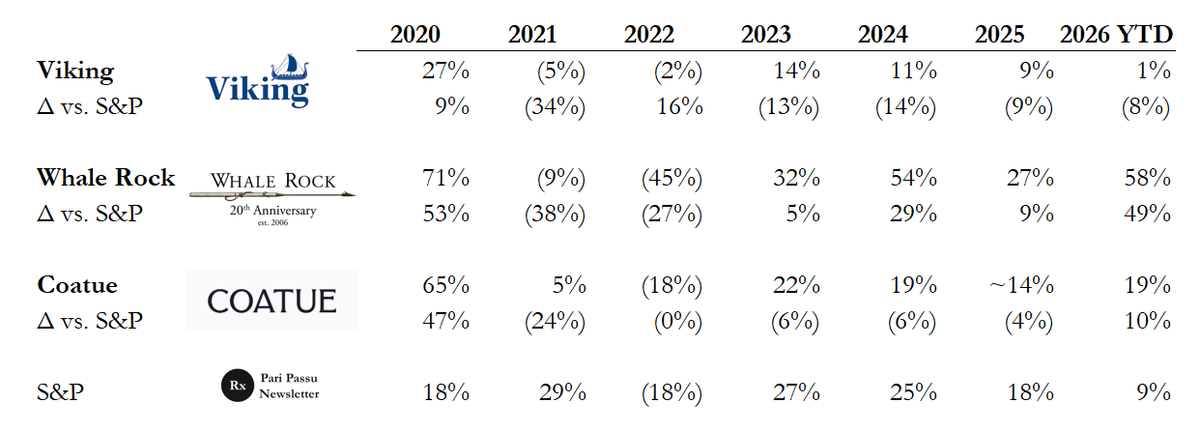

I have massive respect for Viking

One of the few hedge funds that actually runs a disciplined portfolio

Everyone in a bull market forgets what happens when the tide turns, see 2022 below

Serious question, if you are an LP, which of the below do you prefer?

1) Viking: actually provides lower vol

2) Whale Rock: smart levered beta

3) Coatue: somewhere in between

China is deliberately choking the global supply of Indium Phosphide (InP), the material that makes every laser in every AI data center work.

Reuters confirmed: US officials have visited China multiple times to resolve this. China is still blocking export approvals on purpose. They want to maintain the bottleneck.

Chinese producers like Yunnan Germanium (https://t.co/wyCjVX0HNv) and Guangdong Xiandao are scaling capacity fast (Yunnan investing $28M to reach 450K wafers/year, shipments up 74% in 2025). But even if export approvals are granted, overseas shipments will be "limited."

Switching InP suppliers requires lengthy qualification cycles. You can't just find a new source overnight. 12-18 months...

This will help explain the recent price action in the below names.

WINNERS:

$SIVE.ST CW lasers ARE InP devices. Policy-duration shortage extends their 14-quarter laser supply constraint indefinitely. Every month China maintains this, SIVE's pricing power widens.

$LITE Substrates come from Sumitomo + JX Advanced Metals in Japan. Entirely outside the China export gate. Their competitor's supply gets squeezed while theirs is control-immune. This is the cleanest relative advantage.

Win Semi (https://t.co/la0Q2W86G1) Only pure-play III-V foundry on earth. InP wafer fab capacity is scarce globally. Tighter substrates = their existing capacity commands higher pricing.

$AEHR Sole-source wafer-level burn-in testing for InP and SiPh devices. When every wafer is more valuable because the input material is scarce, the cost of shipping a bad one goes up. Testing intensity rises with scarcity.

AIXA (https://t.co/B1hBTJxtCC) Makes the MOCVD equipment needed for InP epitaxy. Every country trying to build domestic InP capacity needs their tools. More fragmentation = more equipment orders.

$SOI.PA Photonics-SOI monopoly. InP scarcity makes the entire optical layer more expensive, increasing the value of every component in the stack including Smart Cut SOI wafers.

LOSERS:

$COHR Reuters specifically names Coherent as "mainly supplied by AXT." AXT manufactures IN China, inside the export gate. Even if approvals come, shipments will be limited. COHR carries a substrate risk that LITE does not. And switching requires lengthy qualification cycles.

$AAOI Demand is not the issue; laser/EML/InP component supply is. If AAOI cannot secure enough laser chips, capacity ramp can slow.

$AXTI AXT is a US-listed InP substrate maker that manufactures in China. Their entire equity value is an export-approval question. If approvals flow, massive upside. If they don't, the business model breaks for Western customers.

We are watching real-time supply chain warfare over AI supremacy. The companies that own the physical bottlenecks in this chain benefit every time the world fragments.

US gov restricting Fable and China announcing the 290 Billion AI Buildout is running according to Leopold's timeline almost to a T. Guy called the entire thing out years ago.

$MU $DRAM Wanna know when supply catches up?

→ HBM eats 30% of all DRAM wafers next year. Possibly 40% by 2028.

→ That leaves 60% for everything else, Mobile, PC, Server, Automotive.

→ New fabs are only a fraction of future demand.

Never

AAII do not represent the average "Main Street" retail trader. Instead, they are a highly specific sub-population. Largely mid-to-late 60s, highly educated males.

Meanwhile, asset managers and nearly fully long Nasdaq.

Hyperscalers are hitting demand limits domestically so they are flooding international markets. Last week AMZN issued largest ever Canadian bond offering, GOOGL's JPY deal was the biggest on record.

tbh that sector is mostly for copers/copium flow who missed memory supercycle, semis supercycle, gpu supercycle, compute supercycle, etc

in other words, its useful to use it to track on mtf cross-sectorially what the ppl last to the party is doing. usually a leading factor/one of the leading indicators on 8th-9th inning environments such as ours.

obviously this is under bayesian conditioning that we are in 8th-9th innings re: ai capex supercycle current wave, so its gd to enter this framework while being situationally aware of the base denominator event driven & its respective invals

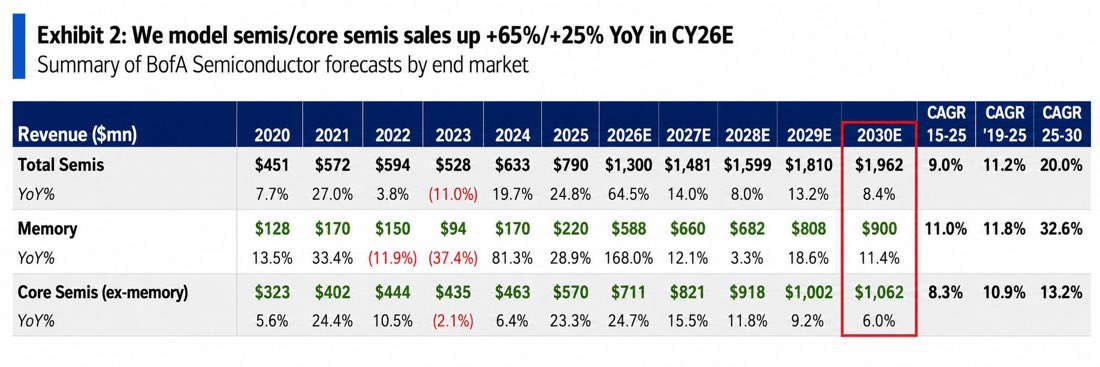

I think this is the most interesting chart from the B of A $INTC report

AI CPUs are almost as large as HBM by 2030. (This is huge, I will try to explain my view at the bottom of this post)

What almost everyone sees

AI accelerators = $1.1T

HBM = $168B

CPUs = $140B

What everyone may miss is

GPUs create a second CPU boom

Just look at the split:

AI Cluster / Head Node CPUs = $70B

AI Agentic Standalone Node CPUs = $70B

Every GPU cluster needs CPUs.

Agentic AI creates an entirely new CPU market the size of today's cloud CPU market multiple times over.

That's a huge bet.

This actually also has implications for $AMD

If BofA is right:

Intel wins of course

AMD wins

ARM server CPU vendors also win

Because the pie becomes much larger.

Roughly $170B by 2030.

For the part AI CPUs are almost as large as HBM by 2030, this is ultra huge

The market often treats HBM as the second largest AI winner after GPUs.

However, it may not be the case, CPUs could become nearly as economically important as HBM.

So If that happens, investors may have underestimated $INTC relative to memory.

Early AI cycle = GPU GPU GPU but we are not in the early cycle anymore

Next (or now) AI cycle = GPU + HBM + CPU + Packaging Networking + Power

Dot-com & Volatility ($VIX)

“The most extreme "spot up, vol up" regime on record occurred during the latter stages of the 1990s bull market. Demand for upside exposure started building as early as 1996, and volatility gradually shifted into a structurally higher regime.

While the final top was marked by a sharp volatility spike, the underlying repricing of risk had begun years earlier. It ultimately took close to a decade for volatility to fully normalize.”- The Market Ear

Source: LSEG