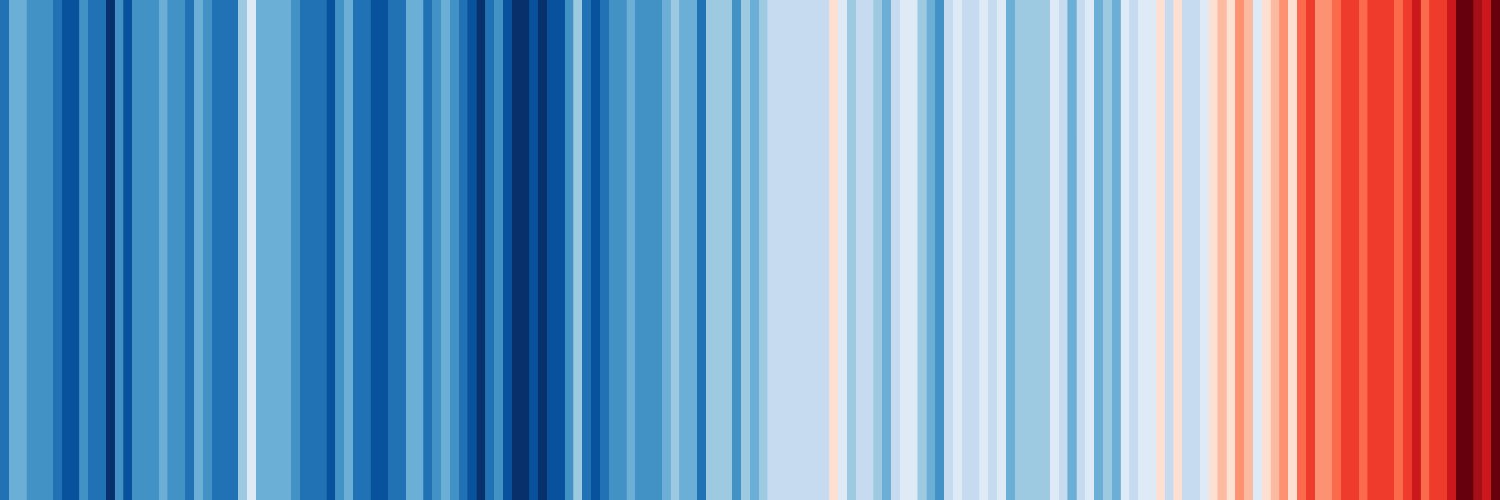

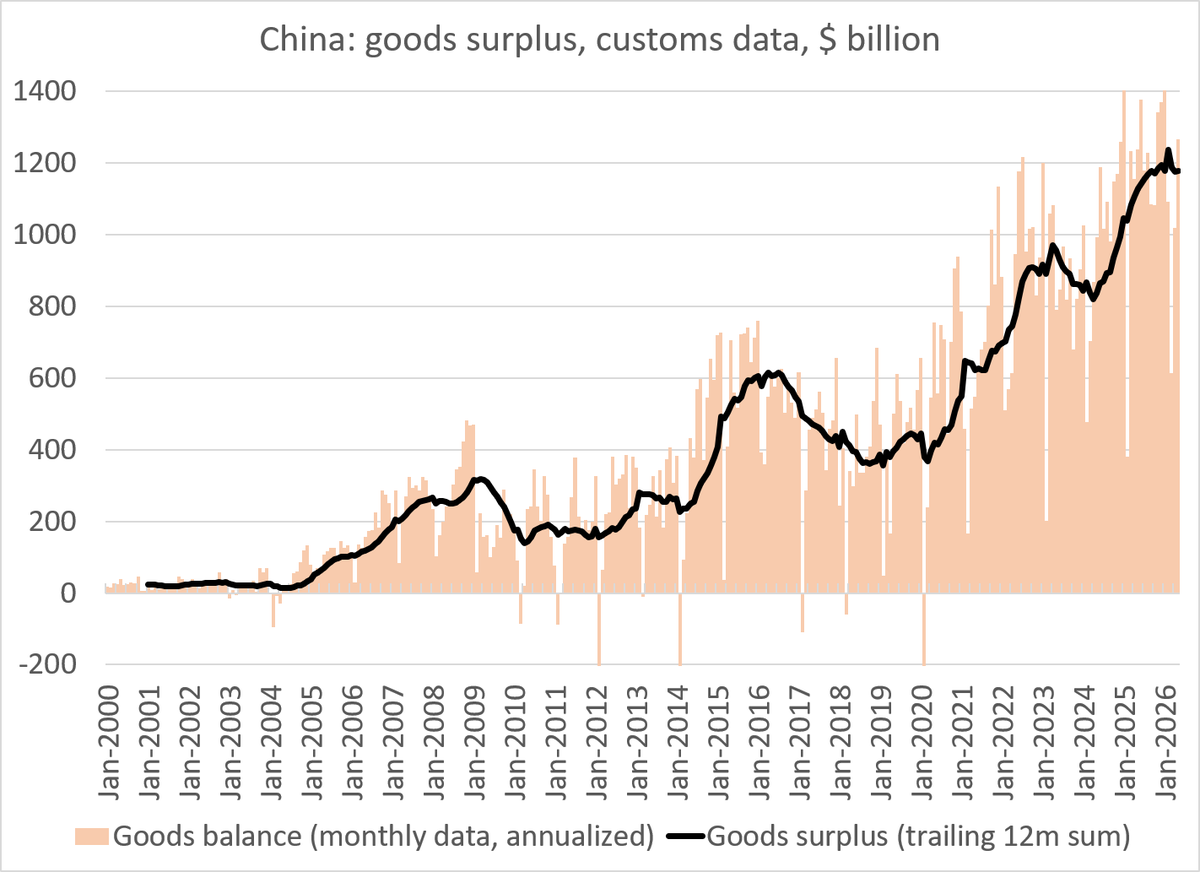

China's constant ~ $1.2 trillion trade surplus over the last 12ms of data is a classic case of a dog that hasn't barked. China imports chips and crude. The price of both have soared. China's surplus should be down not flat ...

1/x

@GabLattanzio Je n’ai rien contre proposition mais compte tenu du poids de la région IDF dans le PIB français je pense qu’une large part de la subvention publique du ticket d’opéra est payée par des gens qui peuvent en bénéficier…

La désinformation propagée par @hugoclement, grâce à @FranceTV est subtile... Elle n'est est pas moins ravageuse.

J'ai regardé ce soir son émission "Sur le Front", sur @france5 : un modèle de manipulation "par omission". Du grand art, je dois dire. On décrypte ?

C'est parti. 🧵

The Economist argues here that China should set a higher GDP growth target because the current target (4.5-5.0%) is too low and will make the economy’s current problems, including surging debt, worse. “The proof,” it says, “lies in China’s prices. They have been falling, by some measures, for three years. This persistent deflation is a worry in itself—it increases the burden of debt, limits the room for monetary easing and mutes price signals, given the reluctance even in China to cut wages in money terms. It is also a sign of a deeper problem. It suggests that output is falling short of what the country could produce if its capital and labour were more fully employed.”

But this is the wrong way to look at the Chinese economy. Chinese deflationary pressures are not an unexpected aberration but rather a consequence of its current growth model.

Falling prices suggest not that there is a shortfall in output but rather that output is growing faster than what domestic – and, increasingly, foreign – demand can absorb. In a system in which excessively high GDP growth targets are met mainly by increasing investment in infrastructure and manufacturing (and, not too long ago, in the property sector), it seems a little perverse to argue that boosting output in a system already suffering from excess capacity in property, infrastructure and manufacturing will cause prices to rise.

If anything, increasing investment in an already investment-heavy economy will tend to worsen the very imbalances that have produced falling prices in the first place. When production capacity expands more rapidly than the purchasing power of households and businesses, prices must adjust downward to clear inventory that banks are increasingly reluctant to finance. In China’s case, the imbalance is reinforced by the structure of the economy, which systematically channels resources toward investment and production rather than toward household income and consumption.

The article also argues that a higher GDP growth target will make it easier to manage the country’s debt burden. But this assumes that there is no connection between GDP growth and the debt burden.

In fact, the opposite is true. The overwhelming majority of lending in the Chinese financial system is used to fund investment, with a very small share going to fund consumption. If investment were healthy, it should be impossible in such a financial system for the debt-to-GDP ratio to rise – except occasionally in the very short term – because the investment itself would generate faster increases in economic value than in debt-servicing costs.

But over the past fifteen years China has suffered from among the fastest increases in the debt-to-GDP ratio in history. This is strong evidence that a rising share of debt is funding non-productive manufacturing capacity, infrastructure and property. More generally, there is a pretty strong correlation between the investment contribution to Chinese growth and the rise in the country’s debt-to-GDP ratio.

To put it another way, China can only set GDP growth targets much above a sustainable GDP growth level – perhaps around 2–3 percent – by accelerating credit creation. In that case, a higher GDP growth target would require even faster growth in debt, and would raise the debt burden further rather than reduce it.

The article does hedge against the likelihood of increasing non-productive investment by arguing that a higher GDP growth target could be achieved by directing resources to households to boost consumption. While this sounds attractive on paper, and while China has spoken for nearly a decade about the need to rebalance with an acceleration in consumption growth, there is a reason why this has proved so difficult. There is also a reason why no country in China’s position has ever managed to rebalance without a slowdown – or even a contraction – in growth.

In rapidly growing economies where high investment is powered by even higher savings, low consumption is not an accident or an oversight. It is fundamental to the way the economy is structured. Businesses and governments receive a disproportionately large share of GDP, while households receive a disproportionately small share. These imbalances are embedded in the mechanisms that drive growth.

If China is to boost the consumption share of GDP, it would require reversing the transfers implicit in the national distribution of income. This could be done by raising wages, raising interest rates, increasing the value of the currency, raising current social-safety-net payments (future promises will not affect current consumption except after many years of credibility building), and/or increasing other forms of household income. In each case, however, the policies that increase household income simultaneously reduce the resources available to subsidize investment and manufacturing.

What many analysts fail to grasp about Chinese manufacturing – just as they failed to understand Japanese manufacturing in the 1980s, is that while China’s very large manufacturing sector is globally competitive, it is also far less efficient than most analysts assumed. If it were genuinely efficient, it would be profitable without subsidies. Yet in many cases it is only marginally profitable despite large transfers that directly and indirectly subsidize its costs.

Among these transfers are an undervalued currency, abundant and cheap credit, artificially low interest rates on household savings, and government overspending on logistics, infrastructure and transportation networks that reduce costs for manufacturers. These policies boost manufacturing competitiveness, but they do so by transferring income from households to producers.

If the global competitiveness of China’s manufacturing sector depends on these direct and indirect transfers, reversing those transfers in order to raise household income would necessarily undermine that competitiveness. The process of rebalancing therefore requires a structural shift away from investment and manufacturing toward consumption and services.

Japan provides a useful example. Between 1991 – when Japan’s consumption share of GDP bottomed out – and 2008, Japan succeeded in increasing its consumption share by roughly 10 percentage points of GDP. But during that same period Japan not only lost roughly half its share of global GDP, it also experienced a decline of roughly one-third in the manufacturing share of its economy. This implies a drop in its share of global manufacturing of roughly two-thirds.

These were not coincidental; they were the nearly-inevitable consequences of rebalancing income toward households.

For China, the implication is straightforward. Increasing the consumption share of GDP necessarily implies slower overall growth and a smaller manufacturing share of the economy. The idea that China can simultaneously dedicate resources to increasing output while dedicating even more resources to increasing demand is hard to reconcile with either logic or historical experience.

My conclusion, therefore, is the opposite of the Economist’s. Chinese deflationary pressures, its huge trade surpluses, its surging debt burden, and its increasingly unviable investment in property, infrastructure and manufacturing are all direct consequences of a political obsession with too-high GDP growth targets. Maintaining these targets requires ever-increasing credit expansion and ever-greater investment in sectors that are already suffering from excess capacity.

It is not an accident that no country with Chinese-style imbalances has ever adjusted without a slowdown – or even a contraction – in GDP growth. Rebalancing toward consumption requires shifting income from producers to households, and this necessarily reduces the pace of investment-driven growth.

For this reason, raising China’s GDP growth target would almost certainly make the underlying problems worse rather than better. The real challenge for Chinese policymakers is not how to increase growth targets, but how to accept lower growth – and a smaller share of global manufacturing – while restructuring the economy and rebalancing the domestic drivers of growth.

https://t.co/xN7rrWhtM1

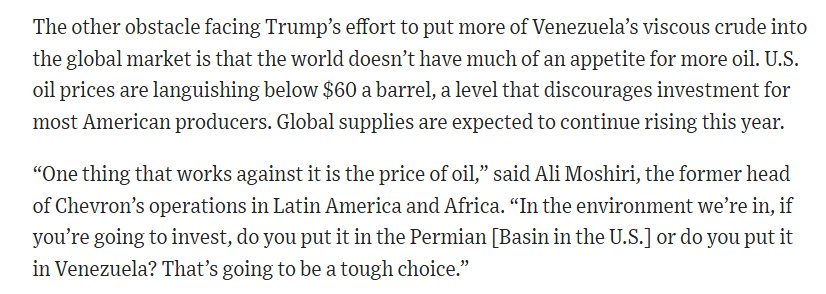

There is a lot of talk -- not the least from the US Administration -- about the windfall from Venezuela's oil. It is worth doing a bit of (boring) quantification.

Bottom line: it isn't going to pay for everything ...

1/

En réponse à la polémique autour du partenariat entre Starlink de Musk et Air France, @LelloucheNico a pris la plume pour expliquer le choix de la compagnie aérienne française et déplorer l'absence de solutions européennes équivalentes ainsi que la méconnaissance des politiques sur le sujet. A lire, c'est très intéressant.

https://t.co/qOy1U10bN2

Merci à @lalibre pour cet entretien – le seul que j’ai jamais demandé à conduire.

Au-delà de l’affaire Euroclear et des risques systémiques (pour la BE, mais aussi la santé éco. de l’UE), il était nécessaire de revenir plusieurs des attendus des déclarations de @Bart_DeWever :

Pourquoi les chiffres de PIB par habitant ou de PIB par heures travaillées semblent si différent selon la source ou la personne qui les cite ?

Une petite explication

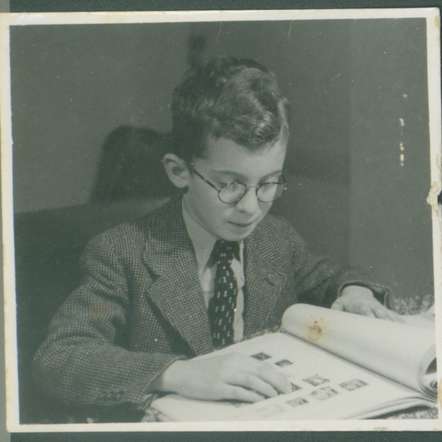

17 December 1931 | Dutch Jewish boy, Emile Joost Jacobs, was born at the Hague.

He was deported to #Auschwitz from #Westerbork in October 1942. He was murdered in a gas chamber after the arrival selection.

---

Video about the first two gas chambers created near Auschwitz II-Birkenau: https://t.co/KArryHBbea

The most effective sanctions against Russia’s shadow fleet right now are Ukrainian SBU drones.

In the past two weeks, they hit three oil tankers in the Black Sea. But The Atlantic writes this escalation also signals Ukrainian desperation ahead of talks. 1/

NSF is launching one of the most ambitious experiments in federal science funding in 75 years.

The program is called Tech Labs, and the goal is to invest ~$1 billion to seed new institutions of science and technology for the 21st century.

Instead of funding projects, the NSF will fund teams. I’m in the @WSJ today with a piece on why this matters (gift link): https://t.co/xteQ3NgWVC

Here’s the basic case:

1) Most federal science funding takes the form of small, incremental, project-based grants to individual scientists at universities.

2) The typical NSF grant is ~$250k/year to a professor with a couple of grad students and modest equipment over a few years. This is a perfectly reasonable way to fund some science, but it's not the only way.

3) A healthy portfolio needs more than one instrument. Project-based grants are like bonds: low-risk, steady, safe. But no one trying to maximize long-run returns would put 70% of their portfolio in bonds.

4) Yet that's basically what our civilian science funding portfolio looks like. Around 3/4ths of NSF and NIH grant funding is project-based.

5) Tech Labs is NSF's attempt to diversify that portfolio. The Tech Labs program is aiming for:

- $10-50 million/year awards per team

- 5+ year commitments

- Measuring impact through advancement up the Tech Readiness Level scale rather than papers published

- Up to ~$1 billion for the program

- Supporting research orgs outside traditional university structures

6) Scientific production looks very different than it did when the NSF launched 75 years ago. The lone genius at the chalkboard can only do so much. Frontier science + tech today is increasingly team-based, interdisciplinary, and infrastructure-intensive.

7) The team behind AlphaFold just won the Nobel Prize in Chemistry. It came from DeepMind, an AI lab with sustained institutional funding and full-time research teams. It would be near-impossible to fund this kind of work on a 3-year academic grant.

8) Same pattern at the @arcinstitute (8-year appointments, cross-cutting technical support teams) and @HHMIJanelia (massive infrastructure investments to map the complete fly brain). Ambitious science increasingly needs core institutional support, not a series of project grants stapled together.

9) Similarly, Focused Research Organizations (@Convergent_FROs) have showcased a new model supporting teams with concrete missions and predefined milestones to unlock new funding.

10) There’s a whole ecosystem of philanthropically-supported centers doing amazing research, like the Institute for Protein Design, the Allen Institute, the Flatiron Institute, the Whitehead Institute, the Wyss Institute, the Broad — the list goes on.

11) But philanthropy can’t reshape American science alone. The federal government spends close to $200 billion each year on research and development, an order of magnitude more than even the largest foundations.

12) If we want to change how science gets done at scale, federal funding has to evolve. And the NSF and NIH don’t have dedicated funding mechanisms to support or seed these sorts of organizations.

13) Earlier this year, I started working on a related framework called “X-Labs” that built on all this exciting institutional experimentation that’s been happening within the private and philanthropic sectors. It’s time for the federal government to step into the arena: https://t.co/0iVLobqQeA

14) Traditional university grants are still important for training the next generation of scientists and for certain kinds of curiosity-driven work. But after 75 years of putting nearly everything into one model, we should try something different.

15) And key program details are still being developed! You can reply to the Request for Information with suggestions or feedback on how to design this program here: https://t.co/R6MNo0ZfN1

16) Science is supposed to be about experimentation. Science funding should be too.

Ce #Budget2026 est gérontocratique, il sauvegarde coûte que coûte le pouvoir d'achat des retraités au détriment de tout le reste. En trahissant ainsi l'avenir, nous sommes tous perdants.

Tribune collective avec les mousquetaires 🤺 @Erwann_TISON@sc_cath@LevyAntoine@WeilEric

The operational situation for the ukrainian 🇺🇦 army is getting increasingy more difficult

After losing most of Pokrovsk, Ukraine is facing an accelerated advance towards Zaporizhzhia in the south.

Russia 🇷🇺 is pushing everywhere at a faster pace.

🧵THREAD🧵1/16 ⬇️

An update on the war following a recent trip. Ukrainian forces are holding, but the situation has worsened since July due to mounting offensive pressure. Here I cover some of the negative and positive trends, along with the salient dynamics at the front. Long thread. 1/

Je ne sais pas qui ça peut intéresser, mais voici un exemple récent de relations civilo-militaires en démocratie. Le Danemark est dans un processus de réarmement rapide, le mot d’ordre actuel étant comment générer du “kampkraft” (puissance de combat) 1/

Rien d'étonnant, cher @jmaphatie. Le tribunal fait du droit, pas de la politique, et dans cette affaire il est bien le seul.

Le tribunal ne banalise nullement ni ces propos ni l'injure. Il dit même expressément le contraire dans ce jugement que vous avez lu, je n'en doute pas.

[Thread] - Essayons de recenser ensemble les lois, non-lois et niches fiscales en faveur des retraités

Je l'alimenterai au fur et à mesure des découvertes