Everyone is chasing the "best AI model."

Meanwhile, the smartest builders are focused on something else:

AI Agent Architecture.

Because GPT-5, Claude, Gemini, or any future model is just one piece of the puzzle.

What actually makes an AI agent useful?

✓ Clear goals

✓ Strong system prompts

✓ Tool integrations

✓ Long-term memory

✓ Workflow orchestration

✓ Human feedback loops

✓ Continuous evaluation

The truth nobody tells beginners:

A well-designed agent with an average model will outperform a poorly designed agent with the most powerful model.

Models are becoming commodities.

Systems are becoming the advantage.

Learn to build the system, not just use the model. 🚀

🔖 Save this roadmap before your next AI project.

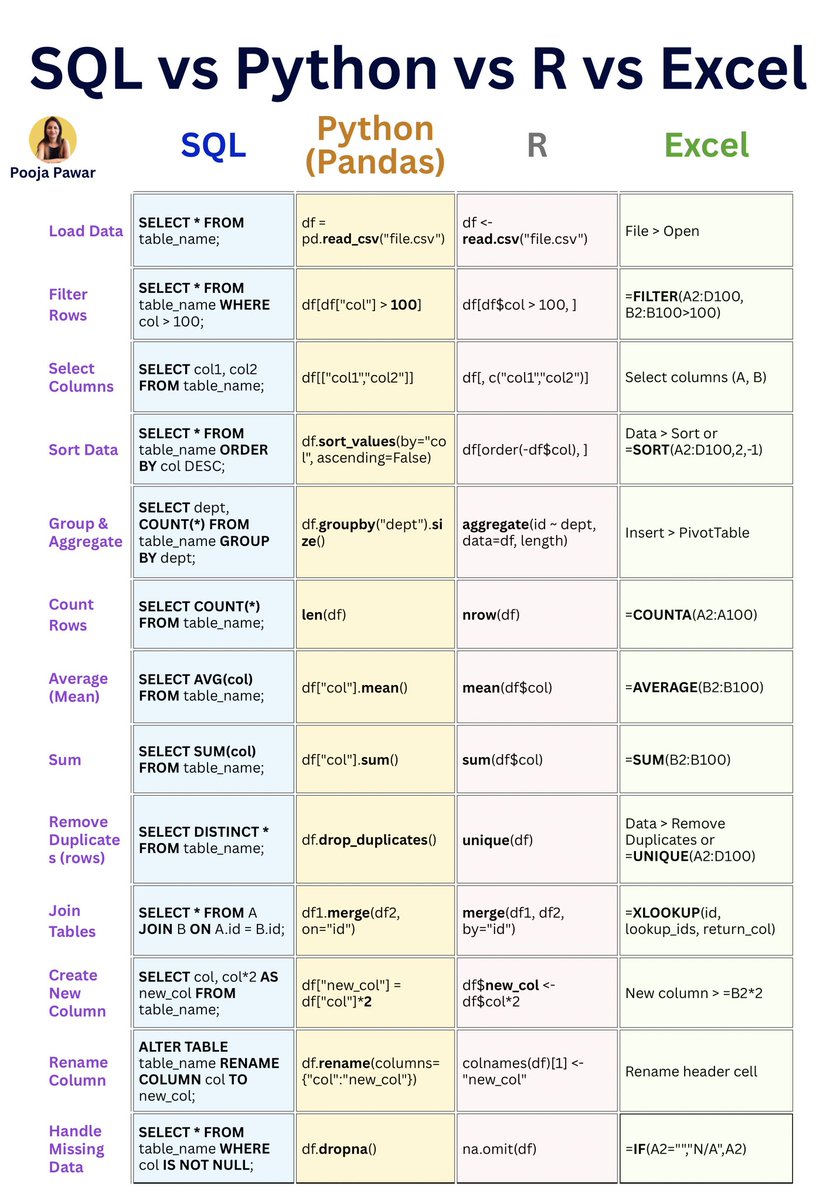

SQL, Python, R, and Excel all solve data problems, just differently. Knowing when to query, script, model, or spreadsheet is what makes a strong analyst. Tools change, fundamentals do not. #SQL#Python#RStats#Excel#DataAnalytics#DataSkills

AI in SRE is here! Google just open-sourced how they keep 5 billion people online.

This is Google SRE. The team that invented Site Reliability Engineering 20 years ago. Every major tech company copied their model. Now they just published exactly how they are rebuilding it with agentic AI.

Here is what their agents are doing inside Google right now:

→ When something breaks, AI agents pull observability data, run through playbooks and fix the issue autonomously before the on-call engineer even gets paged

→ AI agents monitor every live incident, write postmortems automatically and generate engineer handoff documents without a human touching anything

→ A system called AI Insights continuously reads every past Google incident ever recorded and feeds those lessons to agents so they get smarter after every single outage

→ Anomaly detection agents learn normal behavior patterns instead of using static thresholds and alert only when something actually looks wrong

→ Every agent has its own identity, its own permissions, its own reliability SLO and its own backup plan. Google treats AI agents exactly like human engineers.

They published the full architecture as a free white paper.

If Google is rebuilding a 20 year old discipline from scratch with agentic AI, every engineering team on earth is already behind and most do not know it yet.

Full playbook here:

https://t.co/qNDOaKORYA

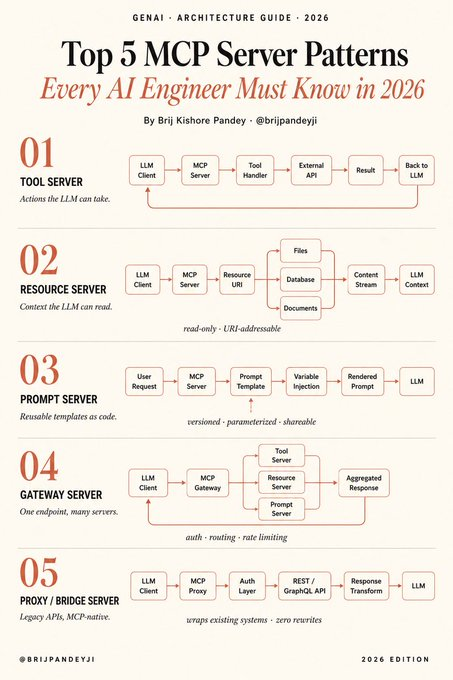

Everyone is talking about MCP.

Almost nobody is talking about the architecture patterns that make AI agents production-ready. ⚡

If you’re building serious AI systems in 2026, these 5 MCP server patterns matter more than prompts:

Tool Servers

AI takes actions through APIs, databases, workflows, browsers, automation tools.

Resource Servers

Inject structured context into agents:

docs, files, vector DBs, internal knowledge.

Prompt Servers

Turn prompts into reusable infrastructure:

versioned, parameterized, maintainable.

Gateway Servers

Central control layer for:

routing, auth, observability, rate limits, orchestration.

Proxy / Bridge Servers

Connect old enterprise systems with modern AI agents without rebuilding everything.

The real shift:

We’re moving from:

“AI chatbot apps”

to:

“AI operating systems.”

The next generation of AI engineers won’t just write prompts.

They’ll design modular agent infrastructure. 🚀

Bookmark this before MCP becomes standard everywhere.

Follow me

@ashiqur_ai

for more AI IDEA.

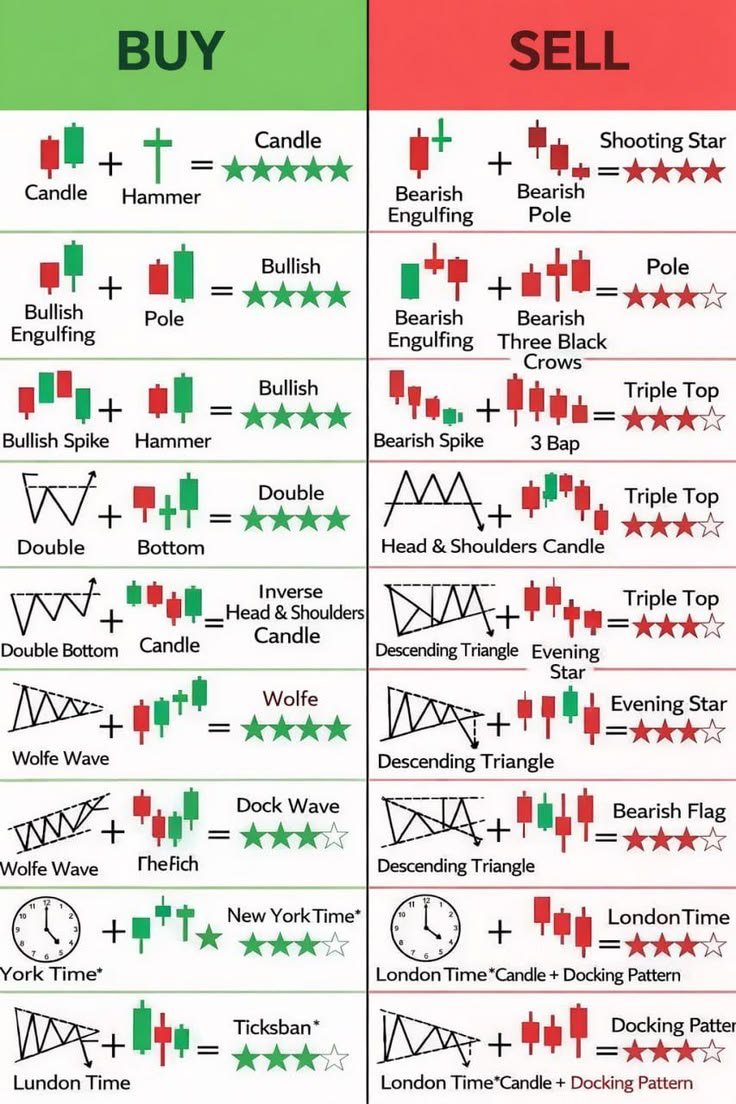

Candlestick Concepts

Bullish Candle ,Closes above its opening price.

Bearish Candle ,Closes below its opening price.

Pin Bar ,Candle with a long wick showing rejection.

Engulfing Candle , A candle that completely engulfs the previous candle.

Doji ,Candle showing market indecision.

Semiconductors are not a single industry.

They are an entire ecosystem. ⚡

🇮🇳 India's semiconductor market is estimated at ~$52 Billion today and is expected to cross ~$100–110 Billion by 2030.

The opportunity extends far beyond chip fabrication.

Key listed players across the value chain:

• 𝗕𝗘𝗟 → Defence Electronics & Radar Systems

• 𝗗𝗶𝘅𝗼𝗻 𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝗶𝗲𝘀 → EMS / Electronics Manufacturing

• 𝗖𝗚 𝗣𝗼𝘄𝗲𝗿 → OSAT / Semiconductor Packaging

• 𝗔𝗺𝗯𝗲𝗿 𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲𝘀 → Electronics Manufacturing

• 𝗧𝗲𝗷𝗮𝘀 𝗡𝗲𝘁𝘄𝗼𝗿𝗸𝘀 → Chip Design & Telecom Hardware

• 𝗞𝗮𝘆𝗻𝗲𝘀 𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝘆 → Embedded Systems + Electronics Manufacturing

• 𝗦𝘆𝗿𝗺𝗮 𝗦𝗚𝗦 → Industrial & Automotive Electronics

• 𝗔𝘃𝗮𝗹𝗼𝗻 𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝗶𝗲𝘀 → Export-Focused EMS

• 𝗠𝗼𝘀𝗖𝗵𝗶𝗽 𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝗶𝗲𝘀 → Semiconductor Design IP

• 𝗦𝗣𝗘𝗟 𝗦𝗲𝗺𝗶𝗰𝗼𝗻𝗱𝘂𝗰𝘁𝗼𝗿 → Chip Packaging & Testing

A semiconductor cycle does not create value in one company.

It creates value across design, manufacturing, packaging, testing, electronics assembly and end applications.

The biggest mistake is studying semiconductor stocks. The better approach is studying the semiconductor value chain.

Capital flows to ecosystems before it flows to individual winners. 📌

Which company from this ecosystem do you believe has the strongest long-term positioning ❓

Save this for future reference 🔖

Educational purpose only. Not investment advice. I may have positions in mentioned securities.

Backend Engineering Mastery Guide

If it is handling requests → APIs

If it is designing APIs → REST / GraphQL

If it is server-side development → Node.js / Java / Go

If it is database management → PostgreSQL / MySQL

If it is NoSQL data → MongoDB

If it is authentication → JWT / OAuth

If it is authorization → RBAC / Permissions

If it is caching → Redis

If it is background jobs → Queues & Workers

If it is messaging systems → Kafka / RabbitMQ

If it is file storage → S3

If it is scalability → Load Balancers

If it is performance → Query Optimization

If it is monitoring → Prometheus / Grafana

If it is logging → ELK Stack

If it is containerization → Docker

If it is orchestration → Kubernetes

If it is deployment → CI/CD Pipelines

If it is system reliability → Fault Tolerance + Resilience

If it is mastering backend engineering → build → scale → monitor → improve → repeat

Grab the Backend Engineering ebook: https://t.co/t9mqUuRbjx

🚨 NVIDIA is making the biggest power architecture pivot in data center history.

The shift to 800VDC for Rubin is NOT just a GPU upgrade.

It's a full supply chain reset — and most investors are watching the wrong ticker.

Here's the 4-layer opportunity map 🧵

Why 800VDC?

Rubin targets 200kW+ per rack.

At that density, 48V delivery creates catastrophic copper losses. You'd need busbars the size of an arm!

800VDC cuts current by ~16x at the same power level.

Thinner copper. Less heat. Smaller form factors. Higher efficiency.

This isn't a product cycle. It's an architecture RESET.

NVDA's 800VDC architecture for Rubin is the starting gun for a 4-layer power supply chain reset. Every hyperscaler building Rubin clusters must rebuild their power stack — from the grid to the GPU.

4 layers. Dozens of beneficiaries. Multi-year capex cycle locked in.

🔴 Layer 1 — SiC/GaN semiconductors

🔵 Layer 2 — Power management ICs

🟢 Layer 3 — Busbars & connectors

🟣 Layer 4 — Grid edge infrastructure

LAYER 1 🔴 — Wide Bandgap Semiconductors ($SiC / $GaN)

800V systems can't use silicon.

SiC/GaN are the ONLY materials that handle high-voltage switching at these frequencies.

Key names:

→ $NVTS — pure-play GaN/SiC fabless, highest beta

→ $ON — best-in-class EliteSiC platform

→ $STM — largest captive SiC fab in Europe

→ $WOLF — foundry economics, captures industry demand

LAYER 2 🔵 — Power Management, Gate Drivers & Protection

The GPU still runs at 0.8V–12V. Someone has to step down from 800V.

That's billions in VRM/PMIC content per Rubin cluster.

Key names:

→ $VICR — most direct 800VDC play. Factorized Power Architecture built for this

→ $MPWR — already in Blackwell. More content per Rubin socket

→ $ADI — isolated gate drivers, critical for 800V safety compliance

→ $TXN — volume play, every PSU uses their analog ICs

$VICR deserves its own separate tweet (I’ll write later).

Vicor's Factorized Power Architecture converts 800V bus → point-of-load in a single step with industry-leading efficiency.

They didn't pivot to 800VDC.

Already engaged with hyperscalers on Rubin deployments.

This is the most asymmetric bet in the entire supply chain map.

LAYER 3 🟢 — Busbars, Connectors & Power Modules

The physical copper architecture of the rack.

At 200kW per rack, connector ASP per system goes up massively.

Key names:

→ $APH — connector kingpin for AI infra, sticky design-wins

→ $TEL — certified 800V connectors = regulatory moat

→ $NVT — thermal + power distribution for high-density racks

→ $MEI — laminated busbars are core competency, deep value

LAYER 4 🟣 — Industrial Power Infrastructure

Grid edge → switchgear → transformers → DC distribution.

Long lead times. Large contracts. 10–20 year asset lives.

Key names:

→ $VRT — highest beta AI power play. Co-architected with NVDA on liquid-cooled racks

→ $ETN — PDUs + switchgear in nearly every hyperscaler globally. 800V-ready now

→ $GEV — transformer/switchgear backlog is multi-year. Grid electrification compounder

→ $SIEGY — medium-voltage DC infrastructure at scale

$VRT is the clearest pure-play on the 800VDC wave.

Vertiv's power + thermal systems are co-designed with NVIDIA for liquid-cooled, high-density deployments.

They're not chasing the market. They're co-architecting it with Jensen.

When Rubin ships at scale, VRT's order book goes vertical.

My 800VDC watchlist by conviction tier:

HIGH BETA (growth leverage):

$VICR · $VRT · $NVTS

QUALITY COMPOUNDERS (durable revenue):

$ETN · $APH · $MPWR

DEEP VALUE (overlooked):

$MEI · $AOSL

Watch procurement acceleration in H2 2026 as hyperscalers lock supply ahead of Rubin delivery.