@RickRieder Interestingly this is part of the reason why mortgage rates have fallen more than 10Y yields. The option component in mortgages has become cheaper as bond vol has slumped.

@AndreasSteno@LanceRoberts@ISABELNET_SA Not so sure about that. Market cap may be inflated, GDP likely not as much. As % of actual earnings may make more sense.

Uncanny similarity of the S&P’s trajectory to the Fed‘s last hiking cycle in 2018. It also gained 50% over 3 years from the first hike (Dec '15 vs Mar '22), before selling off by 19% and bouncing back exactly as it does today. Remember, 2018 was Trump‘s first trade war with China

@profplum99 I disagree. The reason why you compare the earnings yield to the nominal bond yield is that these are the two actual investment alternatives you are facing. If the consensus is right, equities currently provide the lowest return on USD100 invested relative to TSYs since 2001.

@TaviCosta The difference to the rise in yields last year is the fact that it reflects an upgraded growth trajectory. High growth, long-duration is less affected as earnings rise with a steeper GDP path. High leverage, no earnings (or non-cyclical) is worst positioned (small cap, utilities)

For those arguing the current dispersion in equity markets is no reason to be worried.

The last two times tech valuations were as rich relative to the market as they are today, was November 2007 and December 2021.

Generally not the best moments to add equity exposure.

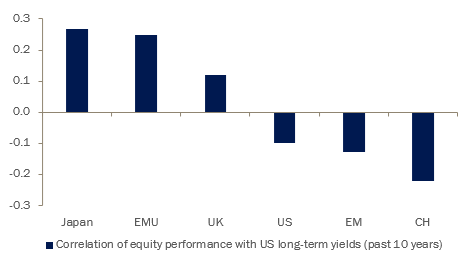

Thus, in order to know what Japanese equities are doing next, you first need to know what US yields are doing next.

If US yields were to drop from here, Japanese equities are unlikely to outperform further.

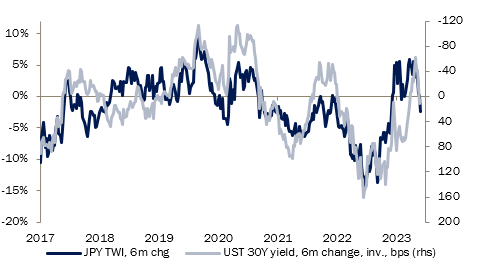

With all the excitement about Japanese equities lately, remember that they trade one-for-one with the Japanese Yen, most of the time.

In particular over the past few years, a weak Yen has boosted Japanese equity performance.

As Japanese yields are pegged by the BOJ's yield curve control, the Yen suffered more than any other currency from rising US yields - and boosted equity performance.

Euro area macro surprises took another beating after PMIs yesterday, dropping to the lowest since August.

Support for euro area outperformance is clearly waning further.