Looking for value, focused on O&G, Mining and Shipping.

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so

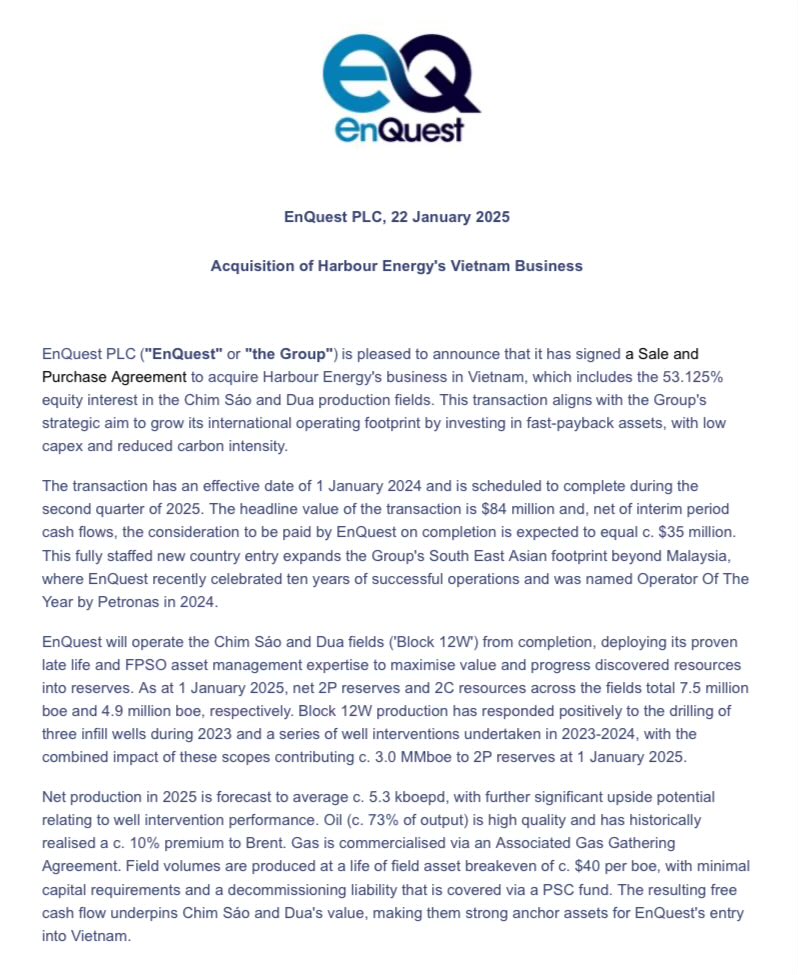

Nice move by EnQuest (never thought I would say that). Fair deal in APAC, that's where they should focus their business. Also positive for $HBR.L that they’re able to sell this in the end. #ENQ $ENQ.L

These people are buying gas produced by Norway from the same sands they could explore and develop.

I still cannot understand the European hypocrisy, being a huge consumer of hydrocarbons while demonizing their extraction.

I had an absolute blast joining @JacobShap & @Geo_papic on the Geopolitical Cousins pod to talk about the Hormuz oil supply hole.

Come for the barrel math, stay for the "which Twitter replies drive me to douse myself with gasoline and light a match" game. https://t.co/6XOHTxIhah

Back into an old investment of mine with a 3% portfolio weight. Panoro Energy Oslo listed.

I see a lot of people buying Kosmos Energy but PEN is very similar except better track record and a lot cheaper.

What’s (really) the price of oil right now?

How the physical and financial oil markets work, and why one can pick up a barrel of crude for $78 in Kansas or $286 in Sri Lanka.

🗞️🗞️ FREE-TO-READ (next 7 days): https://t.co/TT7PvaFaMY @Opinion

Hi guys.

The reason that Middle Eastern cash prices for near-term delivery barrels are extremely high is because they really need oil on the right side of the map.

WTI and Brent are on the left side of the map.

It takes time to get the oil across the map.

FREE @ShaleTier7!

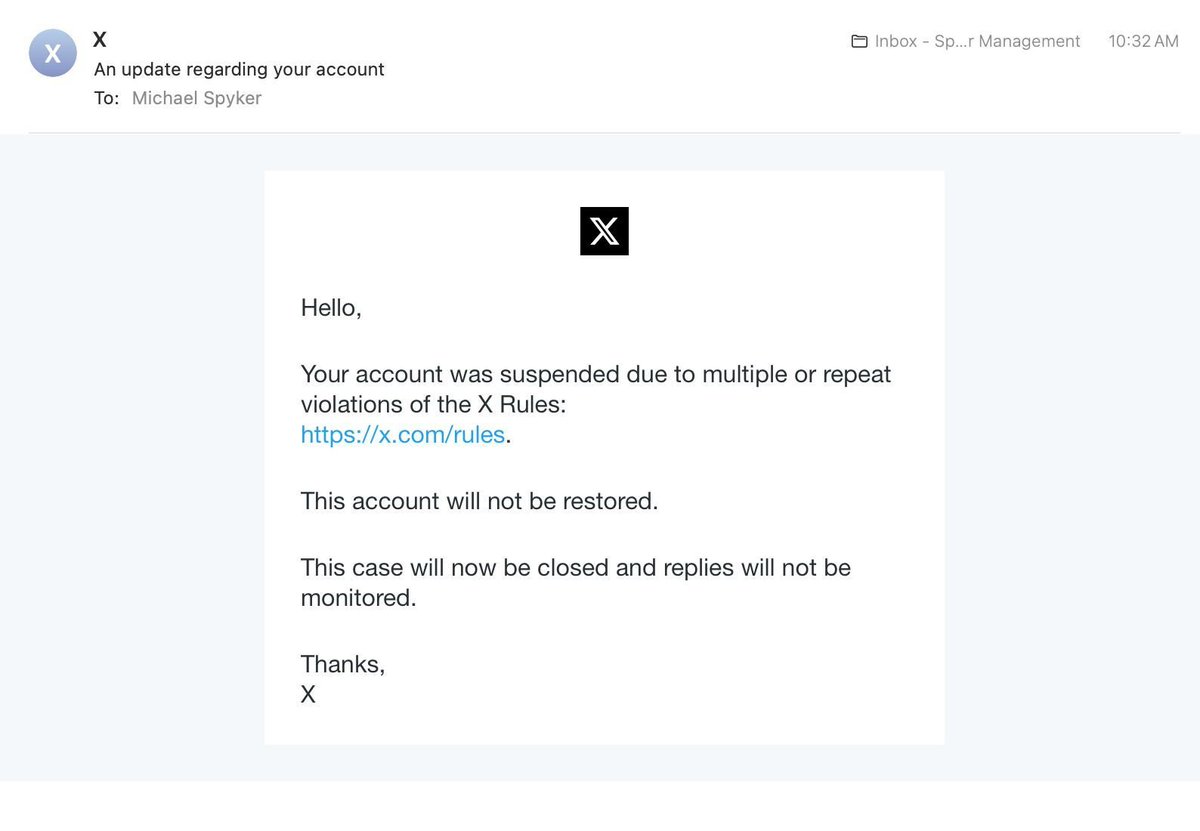

Chatting with Michael and he was just informed that his account suspension is now permanent and that his appeal has been closed

He was never shown an offending Tweet nor given any details of his offence beyond "inauthentic behaviors" (He's just like that!)

It's not about years of experience. It's about innate talent.

You never see someone that had a mediocre track record for 10 years, and then start to kill it.

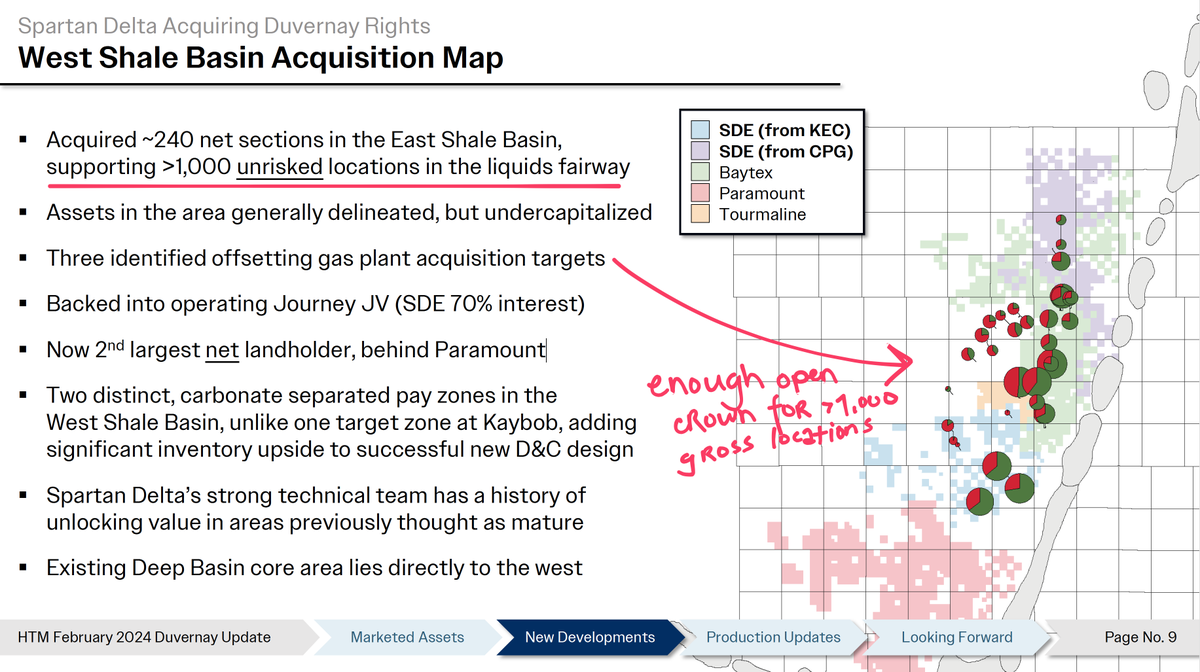

One thing I've thought about a lot is the timeline on Spartan Delta. Not for the usual "hurr durr Duvernay so good" reasons (though, that too), but for reasons as the whole saga is probably highly predictive of the next legs of alpha in upstream equities. I'll explain, bear with me.

It was Q3 of 2023 when Spartan Delta began mentioning the Duvernay. That's nearly 3 years ago. In Q4 of 2023 they began press releasing deals and crossed 100,000 net acres.

In Q4 of 2023 Spartan released their first West Shale Basin acquisition officially (before it had just been a "focus area" in their presentation deck). In Q1 of 2024 they acquired Tourmaline's asset that they got from Bonavista, and then shortly after began buying land at the crown land sale.

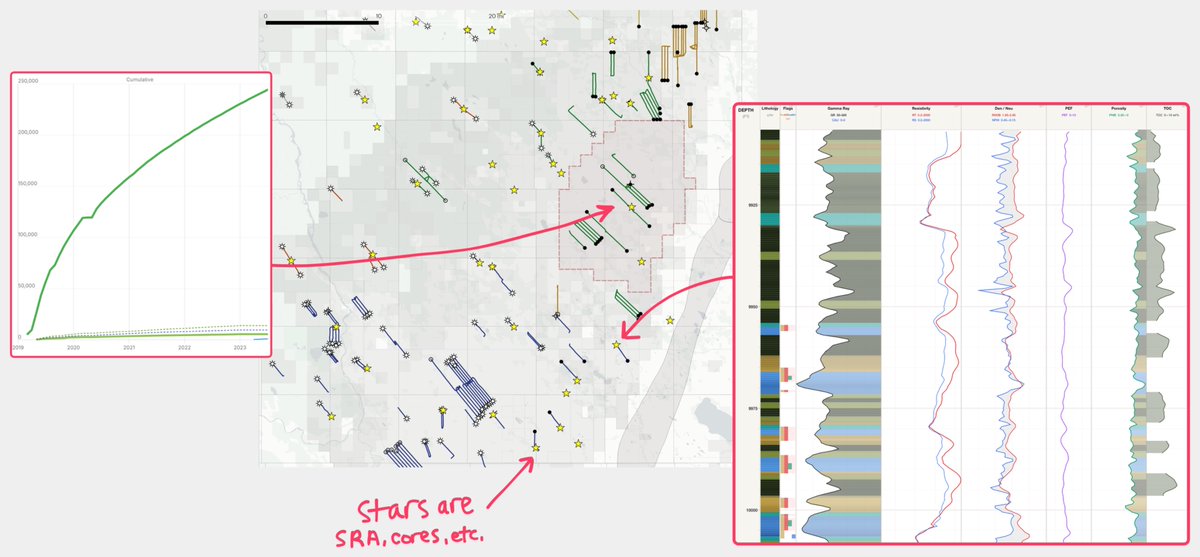

It's important to note that the visibility into the play is pretty robust. Tons of logs, core studies, very easy to map, and importantly very easy to understand the story behind the idea. By 2023, a Kiwetinohk well on the Journey JV had already produced ~250MBbls and had a booked EUR of >450MBbls, so not like we're wildcatting here.

So I would say for anyone paying attention, it was very clear what Spartan was going to do late-2023, and then really late-2024 people should have been on the offensive. By Q1 of 2025, Spartan had already proven that this asset was pretty much Tier 1 core of the core. The stock still didn't move. Really it wasn't until Q2 2025, a full 24 months after they started buying Duvernay, that the stock began pricing it in. And that's so freaking wrong. It should have been exceedingly clear what Spartan was doing. And this was as low-risk as it gets to me.

The Duvernay position they have today is worth $2-3Bn, and that was assembled with minor incremental equity. This should have been the biggest slam dunk of anyones career. But lots of people just didn't do anything about it. And mind you, this is Spartan Delta. This wasn't some random farmer with a thesis; these are some of the smartest guys in the basin. Nothing though... no credit whatsoever.

I think that's going to be the same for a lot of the large international/US ex-L48 shale assets that are being assembled right now. There's always been international exploration, but it's far harder to get an edge there. It's almost impossible to get seismic and when a new offshore field or whatever is discovered, generally it's less repeatable than unconventionals and comes with higher risk. Not always the case, but I think 'harder to get an edge' holds true. Not to mention to asymmetry is WAY more skewed.

But now we're exploring for unconventional; and it's easy to get an edge there. It's far easier to understand an unconventional 'story' vs. say a conventional deepwater story.

Unconventional story: we're gunna frac the Ghawar source rock bois and it cost $30mm to test

Deepwater story: Our blind geologies believes there's some lowstand tracts regression updip shelf-edge deltas prograding saturated clinoforms chunk sediment basin floor migration trap garbage look at this seismic you don't understand and it costs $300mm to test

These asymmetric bets are pretty much what it's all about right -- and there are 3-4 of them that have the potential to add absolutely unbelievable chunks of NAV to various issuer's model.

A lot of analysts are focused on the Permian y/y IP365 BO/ft values declining; like it really can't get any more grim than that. The Permian is going to stay flat and companies are going to harvest that free cashflow. If you're still talking about EOG's Delaware productivity declines when their wells still make ridiculous amounts of money (you know who), you're way behind the 8 ball in my view. Spartan never had a perfect balance sheet but they always had the liquidity to fund expansion from the Deep Basin asset. That's how the Permian behaves now to me. If you're buying Permian cause it's "cheap" in the public markets -- my brother I have some bad news.

So I suppose the story is, that there are going to be massive shale assets assembled outside of the Permian. Whether that's in Argentina or the Middle East, there's going to be some massive wins booked in the next 5 years. And if it was this lagged in Canada in the Duvernay, imagine how lagged and explosive it's going to be for larger assets.

So instead of jamming F5 on monthly production data to circlejerk over 0.02% lower BO/ft cumes -- time feels way better allocated instead getting comfortable with what some of these massive international unconventionals can do, and what to look for to confirm a thesis; is probably going to deliver serious alpha in the next 5 years.

And you really shouldn't let that alpha get scooped up by others. The amount of data to both appreciate what the "story" is -- along with the data needed to confirm a thesis is readily available.

For Argentina, data is public and easy to access much like the US. For the Middle East it's a bit harder but it's doable, especially if you have a budget. The Middle East satellite flyovers are pretty much always clear, and it's easy to get in touch with people actually operating the fields with a little work. With the right prompt, various LLMs can also put you together some tracking tools. A great source for geoscience data is academic papers; and with a little work it's easy to get familiar with the thesis that the operators are chasing for these international plays. Even Argentina -- tons of data, you can build section-level type curves it's that dense right now. Same can't be said for UAE or Algeria, but it's worth the work. Unconventionals are just easier to understand in terms of the thesis, like you're not dealing with structures or pinch outs or sea levels generally to get acquainted.

So all to say; there are a number of stories that are at the top of their funnel, and it's probably easier than ever, and more profitable than ever for potential equity owners -- to familiarize yourself with the play concepts, get a rough idea of what they can be worth, identify what is needed to confirm your thesis -- then keep track of these stories using both public and alt-data; then act on that funnel in the equity markets.

Probably make a bit more money that way than buying a heap of tired 'cheap' crap that's just levered oil beta with a management team!

Volans-1 results:

- Strong deliverability: 33Mmscfd of gas and ~5.3kkbls condensate on a 46/64 choke

- High liquid gas condensate: CGR of ~160 STB/Mmscf

- Low CO2 and H2S: 1-2% CO2 and ca. 3ppm H2S (highest value of 5ppm in 200 samples)

https://t.co/bkx4Gr6nqs

#Valeura Energy announces record cash position of US$306 million at 31 Dec, successful drilling at Jasmine field, and 2026 guidance in line with long-term value objectives.

$VLE $VLERF #Thailand#Türkiye#oil#gas

https://t.co/rIu4rx3muE

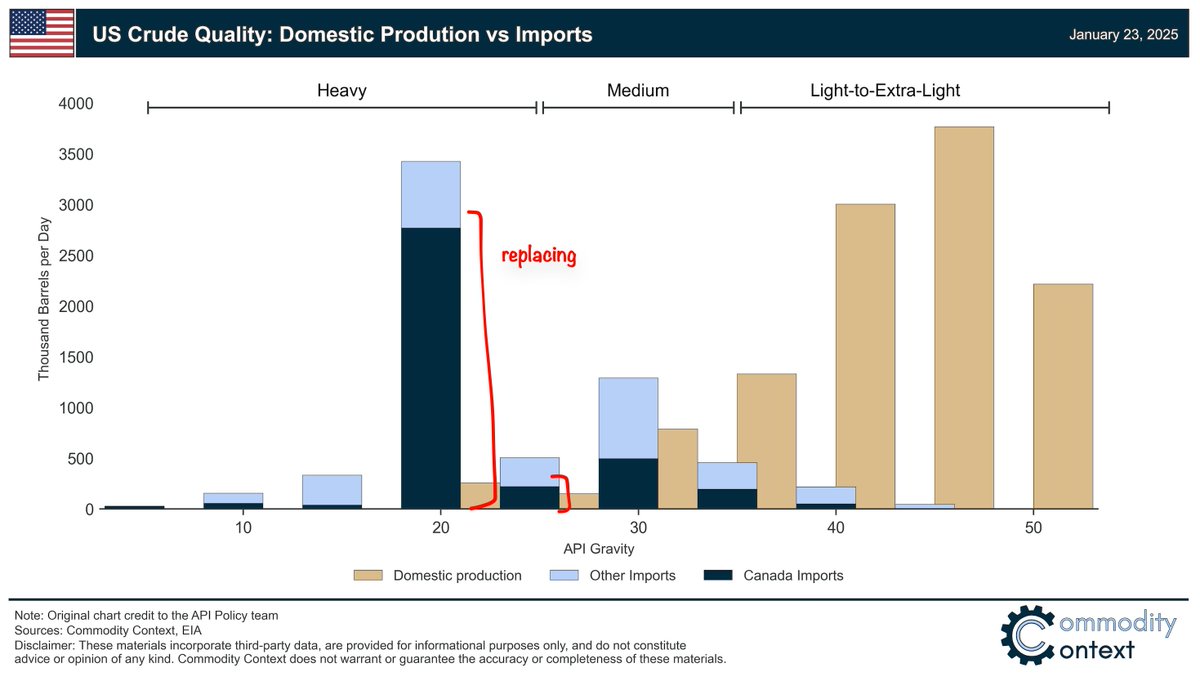

I have spent a lot of time talking shit at people with opinions on Venezuela's oil production potential, and how it's going to "RePLaCe CanADa". So here's my contribution -- how I see the cost of replacing Canadian crude with Venezuelan heavy.

I think it's a nearly $1 trillion bill to get that done. I'm not sure who has a spare $1 trillion in their jeans.

Venezuela's natural domestic consumption is ~1MMB/d, so to completely replace Canada and reach 3MMB/d of export capacity, the country needs to grow production to ~4MMB/d of production, a level they have never hit before. Exports never really exceeded more than ~1.2MMB/d.

They have one main export terminal (Puerto José) capable of ~1.2MMB/d and other smaller terminals gets them to realistically, 1.7MMB/d, so they need +1.3MMB/d in just export capacity and storage facilities, that's $5-10Bn. On the US side there needs to be minor import expansion, but not super major, around $1Bn.

Then, they have to get the oil flowing north. You'd be able to repurpose some Canadian pipelines (if we assume no USGC re-export), but right now Mid-Valley Pipeline is the only major remaining heavy trunk line that moves oil from the USGC region northward into the Midwest. So you need +3MMBbls/d of crude pipelines that move crude north which would run around $30-50Bn. Then you also need a condensate return line for another $10Bn.

Venezuelan crude has higher levels of metals and a higher TAN than Canadian exports, so you need to retool the refineries accepting the new sauce, that's another $50-90Bn on the tab.

Cause there's not enough VLCCs in the world to service this, you also need to build new tankers for the shuttle service. 30 new VLCCs will cost $4-8Bn.

Then onto the upstream. I'm going to say that if you're getting super majors to really invest in Venezuela, they're going to do tertiary recovery which is overwhelmingly the right play over 20+ years with current SAGD tech (SAGD wasn't commercial when Venezuela grew the first go-round). Using foamy oil to get to 4MMBbls/d and keep it there for 10-20+ years is impossible (we're replacing Canada so we need a 20+ year RLI).

Right now, Venezuela produces oil cold, and uses depleting reservoir pressure to bring that oil to surface. For a true Canada replacement, you need heat, which is going to be expensive! But we're not building new upgraders (replacing Canadian heavy), but even then upgrading capacity is only ~0.7MMB/d.

The problem is they don't have the power infrastructure to add the power needed for 3MMBbls/d of SAGD for steam generation, and even for primary recovery they don't have the electricity they need. So you need to build 10-15 GW of new power infra, at gas-fired capital cost including transmission and the new midstream infra to move gas (including LNG import terminals), that's another $40-75Bn just to get the power to the SAGD facilities. There are constant rolling blackouts in the country. You also need ~7-900MB/d of diluent looping on the Venezuela side, including DRUs for another ~$25Bn. Other local midstream refurb is at least $15Bn to replace ashphalted and corroded trunk lines. Any North American firm would also have to commit to cleaning up Lake Maracaibo which is a $10Bn commitment.

For the actual upstream facilities, I'm just going to use a pretty general number based on 125% of Canadian Greenfield costs, so ~$45K/Bbl/d, and lets just call it 2.8MMB/d that's another ~$125Bn for the actual production facilities and ~$220Bn in sustaining CAPEX while everything ramps, and inevitable 5yr issues will add another $10Bn.

There are also very little functional logistics infrastructure. The Tinaco-Anaco rail line was never completed, so you'd have to finish that. All copper has been inevitably stripped and looted, you'd have to rebuild all sorts of worker camps, airports/airstrips, rail spurs, trainload facilities. You'd need to re-dredge the Orinoco River ($15Bn), complete the Tinaco-Anaco line ($20Bn), build 1,000 miles of new heavy spec roads ($25Bn), and you'd need to refresh all of the civil infrastructure cause nobody from Houston is going to live in Venezuela as it stands. So you're going to shoulder that in wages, or Fort Mac copy-paste CAPEX for ~$40Bn. You are also, in the growth/construction and first 5 years going to spend $50-60Bn on paying employees/EPC/other contractors. You need at least 50,000 people in offices and fields to get this done. Of course, security too. Petrominerales spent ~$2.50/BOE on security, so +3MMB/d over 5 years is ~$10Bn on security.

So all-in we're at ~$700Bn in both direct upstream costs, and indirect costs. All-in, this is a $1 trillion project to grow exports ~3MMB/d. There is short-term growth to be had, but it's not sustainable growth. There is also huge long-term potential, but it's not the same as drilling a pad in the Permian and ripping a tie-in to Energy Transfer. It's a freaking massive commitment. The country is pretty much dilapidated, and until super majors (and other infra builders) begin committing to the full-cycle costs associated with realizing the country's potential, the upside is not as robust as many would want you to believe.

- Export terminal ($8Bn) and import refresh ($1Bn)

- Pipelines from USGC to Midwest ($40Bn) and then a condensate return line ($10Bn)

- Retooling refineries ($75Bn)

- New tankers for shuttle service ($6Bn)

- Lake Maracaibo clean up ($10Bn)

- New power infrastructure for the upstream growth at a post-AI inflated capital cost ($60Bn)

- New diluent looping ($25Bn)

- Actual upstream production facilities and <5yr sustaining capital and issue contingency ($355Bn)

- Full logistics and civil infrastructure overhaul (~$100Bn) and security ($10Bn).

US imports chart by @Rory_Johnston

What a first hole on a greenfield project 🙌 $CCCM.v

C3 Metals Intersects 269m at 0.30% Copper

"Based on size and strength of the alteration, mineralization, geophysical footprints, and the geology we are seeing in drilling, Khaleesi clearly demonstrates the potential for a large copper system analogous to some of the large nearby deposits"